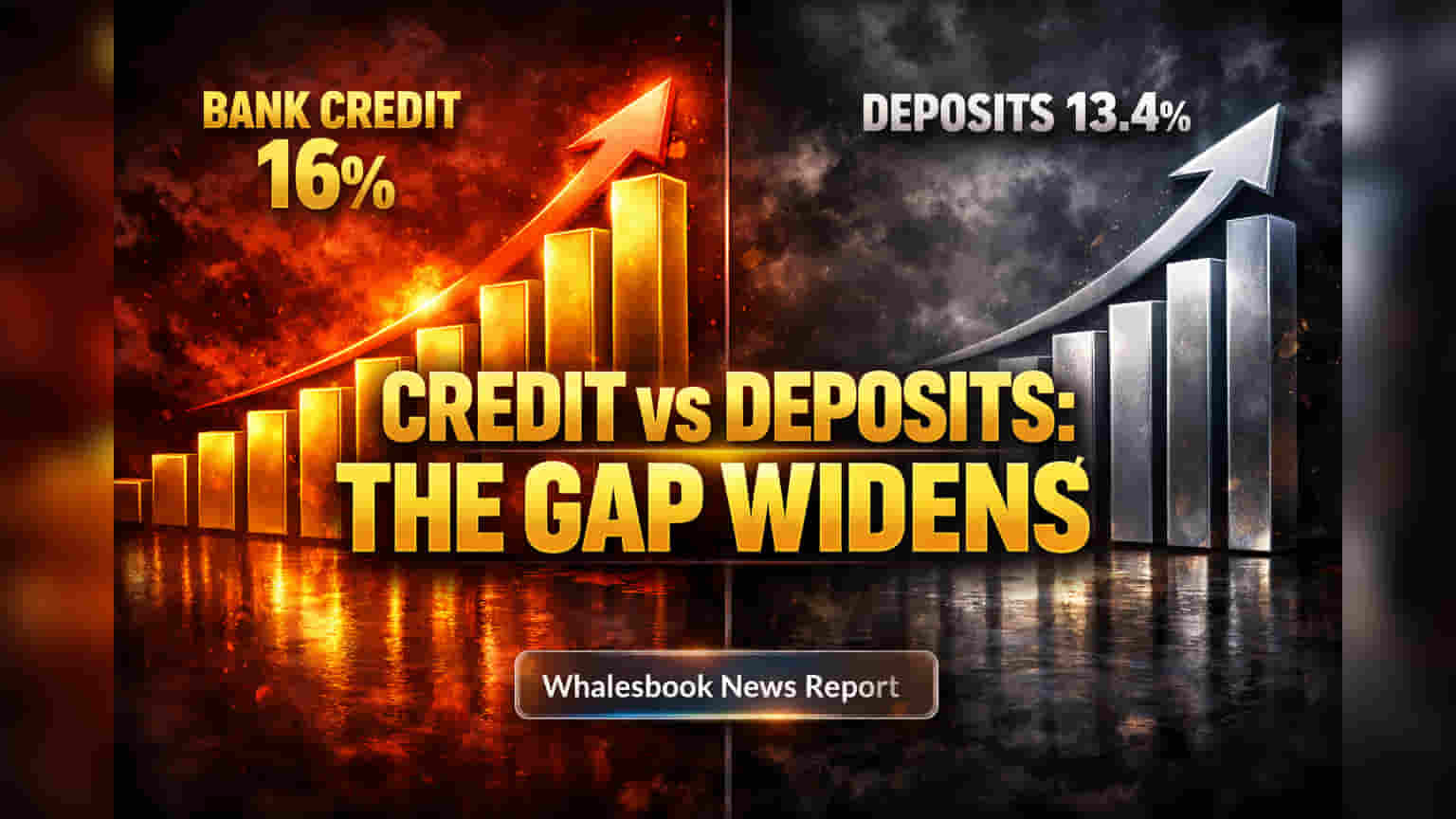

Credit Growth Surges Past Deposits, Widening the Gap

Data from the Reserve Bank of India shows a growing gap in the banking sector for the fiscal year ending March 31, 2026. Bank loans grew a strong 16% year-on-year, reaching ₹219 lakh crore. Deposits, however, grew at a slower 13.4%, totaling ₹267.8 lakh crore. This is the fastest loan growth seen since FY24. The large difference between lending and deposit growth has widened over the year, pushing the overall credit-deposit ratio to over 83% by mid-March 2026. This means banks are increasingly using costlier wholesale funding instead of cheaper, stable retail deposits to fund their loans.

Rising Funding Costs Pressure Bank Profits

This rapid loan growth, fueled by strong demand from businesses and individuals, is directly impacting bank profits. Analysts warn that loans growing faster than deposits is pressuring bank margins. Net interest margins (NIMs) may stay flat or fall for many banks as funding costs increase. This is due to greater competition for deposits and more reliance on Certificates of Deposit (CDs). The average cost for banks to get funds has risen because it's harder to gather deposits fast enough to meet loan demand. CDs now make up 2.6% of total deposits, the highest in ten years. This problem is made worse as people move savings to market-linked options, reducing the amount of cheaper funds from checking and savings accounts. While the RBI's February 2026 policy kept the key interest rate at 5.25%, this funding pressure is a constant challenge. Investments grew more slowly, up 4.7% to ₹71.4 lakh crore, as banks managed their balance sheets carefully amid funding difficulties.

Risks: Loan Surge, Global Economy, and Funding Challenges

While strong loan growth shows economic strength, it also carries risks. People are saving less in traditional bank accounts and more in market-linked options, reducing the supply of cheap bank funding. This pushes banks to use more expensive wholesale markets, potentially hurting profits and delaying margin improvements. Also, India's banks face a more unpredictable global economy. Global conflicts and oil price swings could increase inflation, forcing the RBI to change interest rates, even though it currently holds them steady. The RBI's limit on currency positions also reduces banks' profits from foreign exchange trading. Analysts say that although loan quality has improved in the past, the current imbalance between lending and deposits, plus rising funding costs, are major long-term risks. Cash availability has also decreased, with some reports of banks facing shortages. This gap between loans and deposits is wider than in the last 10 years, unlike during the pandemic when deposits grew faster than loans.

Outlook: Stable Growth Despite Pressures

Despite these pressures, India's banking sector outlook is largely stable, backed by a strong economy and steady demand for loans. Loan growth is expected to continue at 11-14.5% in FY27, driven by ongoing demand from individuals and small/medium businesses. Moody's has a stable outlook, expecting steady profits and higher returns on assets. Net interest margins are forecast to stabilize, with some areas potentially improving slowly as interest rate cuts likely end. Loan quality is expected to stay strong, with bad loan ratios forecast below 2.5%. Banks' capital reserves are at their highest in decades, offering an important safety net against unexpected issues. Future growth will depend on banks managing funding difficulties, using digital tools, and lending carefully under changing rules.