1. THE SEAMLESS LINK

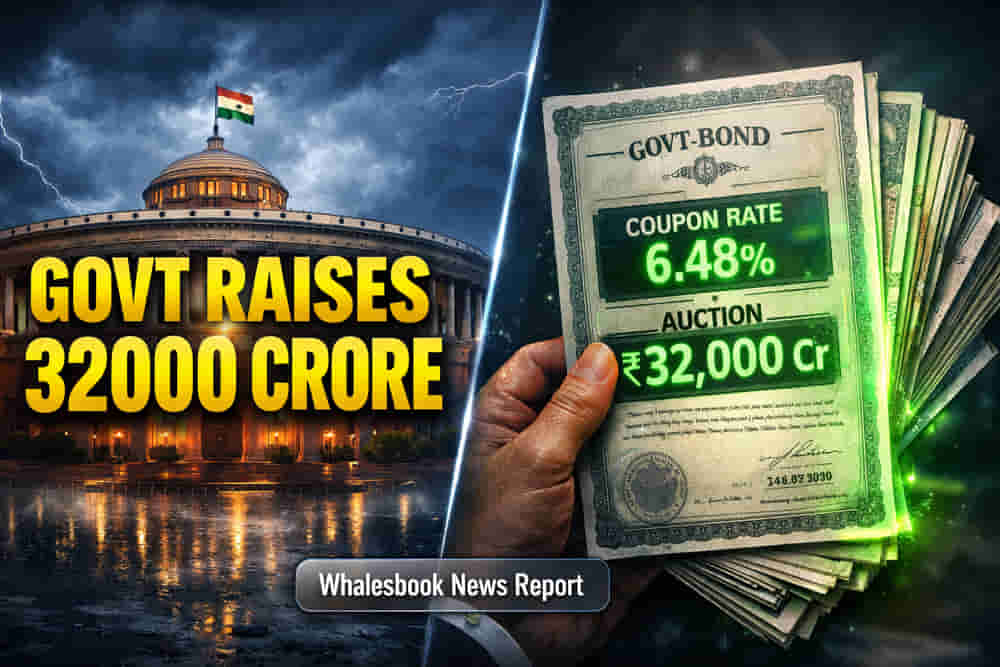

The scheduled re-issuance of the 6.48% Government Security maturing in 2035 signifies a critical juncture in the government's ongoing fiscal management. This auction is not an isolated event but an integral part of a broader strategy to meet substantial funding needs, a narrative supported by recent budget allocations and borrowing projections.

### The Government's Funding Imperative

The Government of India's commitment to its fiscal deficit targets, projected at 4.4% of GDP for FY2025-26, necessitates continuous market borrowing. The FY2025-26 budget outlined net market borrowings from dated securities at ₹11.54 lakh crore, with gross borrowings estimated at ₹14.82 lakh crore. This large-scale issuance program, including the 6.48% GS 2035 re-issue, is crucial for financing infrastructure projects and other government expenditures, underscoring the government's reliance on debt markets to bridge the fiscal gap. Total government liabilities are projected to reach approximately 56.1% of GDP by March 2026.

### Market Equilibrium and Yield Dynamics

The benchmark 6.48% GS 2035 bond yield has been hovering around 6.66% to 6.68% in mid-February 2026. This stability occurs against a backdrop of a neutral monetary policy stance by the Reserve Bank of India (RBI), which maintained the repo rate at 5.25% in February 2026, citing benign inflation and resilient growth. The RBI's proactive liquidity management through tools like Variable Rate Reverse Repos (VRRR) and Open Market Operations (OMOs) has ensured surplus liquidity in the banking system, averaging around ₹2.70 trillion in February 2026. This ample liquidity provides a cushion against excessive yield spikes, though persistent supply pressures from government auctions remain a key determinant of bond prices. Concerns regarding the depth and duration of the government's borrowing calendar could potentially push yields towards the 6.70%-6.75% range in the near term.

### The Underwriting Mechanism and PD Role

The auction process relies heavily on Primary Dealers (PDs), who act as underwriters and market makers. These entities commit to bidding for a portion of the issued securities, ensuring that the government meets its borrowing targets even if market demand is tepid. Bids for the competitive portion are submitted electronically through the RBI's e-Kuber system, with specific windows for Primary Dealers on auction day. The underwriting mechanism, including Minimum Underwriting Commitments (MUC) and Additional Competitive Underwriting (ACU) auctions, is designed to facilitate smooth debt issuance and maintain market stability.

### Risks and the Bear Case

Despite a generally stable outlook, several risks could influence the bond market. The sheer volume of government debt issuance planned for the fiscal year could exert sustained upward pressure on yields, potentially increasing the government's borrowing costs. While inflation remains subdued at approximately 2.1% for FY26, global geopolitical tensions and economic uncertainties pose potential headwinds. Furthermore, a continued increase in government debt relative to GDP, even with a roadmap for reduction, could raise long-term fiscal sustainability concerns among investors. The sheer size of borrowing might also lead to concerns about crowding out private sector access to credit, though the RBI's liquidity operations aim to mitigate this.

### Outlook and Investor Stance

The market anticipates continued investor appetite for longer-duration sovereign papers, a trend observed in previous auctions. The RBI's commitment to managing liquidity and its steady monetary policy are seen as stabilizing factors. However, market participants will closely scrutinize bid amounts, cut-off yields, and underwriting spreads from this and subsequent auctions to gauge investor sentiment and the trajectory of benchmark yields. The overall outlook suggests a balancing act, with continued government supply meeting cautious investor demand amid evolving macroeconomic conditions and global risks. Analysts predict that interest rates may remain stable for the next nine to twelve months.