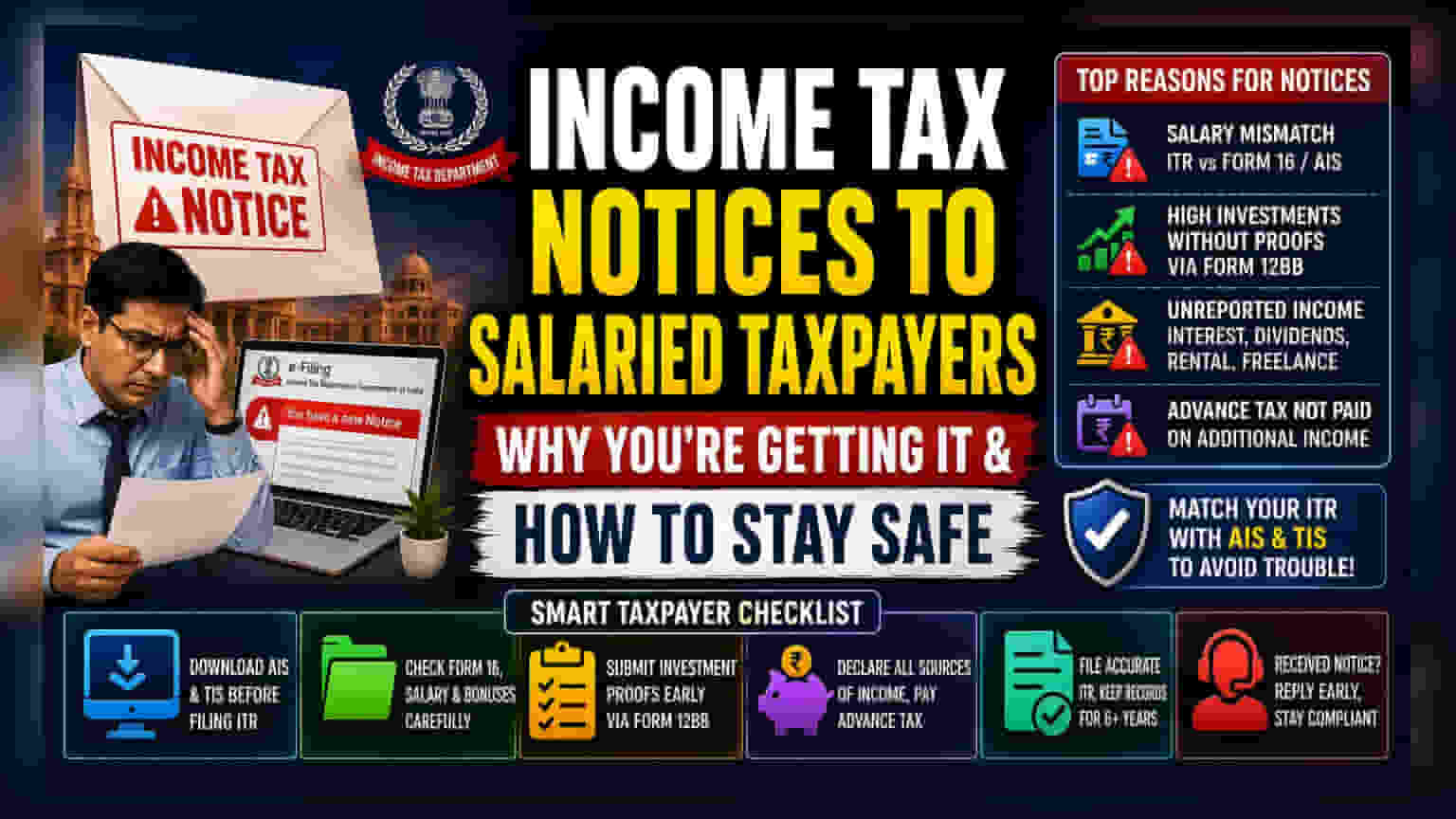

Many salaried taxpayers are receiving income tax notices due to errors in their tax filings. The Income Tax Department’s automated systems often flag discrepancies between reported income and data in the Annual Information Statement (AIS). Common triggers include salary mismatches, inflated investment claims, and missed advance tax on secondary income. Understanding how to cross-verify these details before filing and knowing how to rectify errors can help taxpayers avoid unnecessary penalties and unwanted scrutiny.

What Happened

The Income Tax Department has been issuing notices to a significant number of salaried taxpayers regarding discrepancies in their submitted income tax returns. These notices are primarily triggered by the department's automated verification systems, which match the data provided by individuals in their tax filings against records available in their centralized database, known as the Annual Information Statement (AIS).

Why This Matters For Investors

For the average taxpayer, receiving an income tax notice can be stressful and confusing. These notices are rarely arbitrary; they usually occur when the income, interest, or investments reported by the individual do not align with the third-party reports submitted to the government by employers, banks, or financial institutions. Understanding these triggers is essential to ensure that tax filings are accurate, reducing the likelihood of receiving a notice that requires a lengthy rectification process.

The Mismatch Problem

A primary cause for these alerts is a mismatch between the salary reported in the Income Tax Return (ITR) and the figures shown in Form 16 and the AIS. This often happens when individuals overlook components like bonuses, performance incentives, or income from previous employers if they changed jobs during the fiscal year. Because the department’s system is fully digitized, it automatically reconciles these figures. If the numbers do not match, the system flags the return for review.

Investment Claims and Form 12BB

Another common area of concern involves tax-saving investments. Some employees declare higher tax-saving investments at the beginning of the year to lower their monthly tax deduction (TDS). However, if they fail to actually make these investments or provide the necessary proofs to their employer via Form 12BB, the employer may not account for them correctly, or the department may question the deductions later. Submitting valid rent receipts, home loan interest certificates, and other investment proofs to the employer’s HR department on time is critical to avoiding later confusion.

Advance Tax on Additional Income

Many salaried individuals mistakenly believe that their employer deducts all necessary taxes. However, salary is often just one source of income. If an individual earns money from other sources—such as savings account interest, dividends from stocks, house rent, or freelance work—they are responsible for calculating and paying advance tax on this income. Failing to account for this additional income can lead to interest penalties under sections of the Income Tax Act that govern the timely payment of taxes.

How to Handle Tax Notices

If a taxpayer receives a notice, the first step is to log into the official income tax e-filing portal to understand the specific reason cited. The notice will usually point to a clear discrepancy. In many cases, the solution involves filing a revised return if a mistake was made in the initial filing. It is important to keep all documents, such as Form 16, bank statements, and investment proofs, organized for several years to respond to any queries the department might raise.

What Investors Should Track Next

Moving forward, the best strategy is proactive verification. Before finalizing an ITR, taxpayers should download and review their AIS and Taxpayer Information Summary (TIS) from the income tax portal. These documents provide a comprehensive view of the financial data the department has on file. By ensuring that the figures in the ITR match the entries in the AIS, taxpayers can significantly reduce the risk of receiving an automated tax notice.