Even if your income is below the tax exemption limit, you may still be legally required to file an Income Tax Return. Specific financial activities, such as large bank deposits, foreign travel, or high electricity bills, trigger a mandatory filing obligation. Failing to report these can lead to penalties and loss of financial benefits.

Many taxpayers believe that if their annual income stays below the basic exemption limit, they are automatically exempt from filing an Income Tax Return (ITR). However, Indian tax laws focus not only on the amount of income earned but also on specific financial behaviors and high-value transactions. In such cases, filing an ITR becomes mandatory regardless of the tax liability.

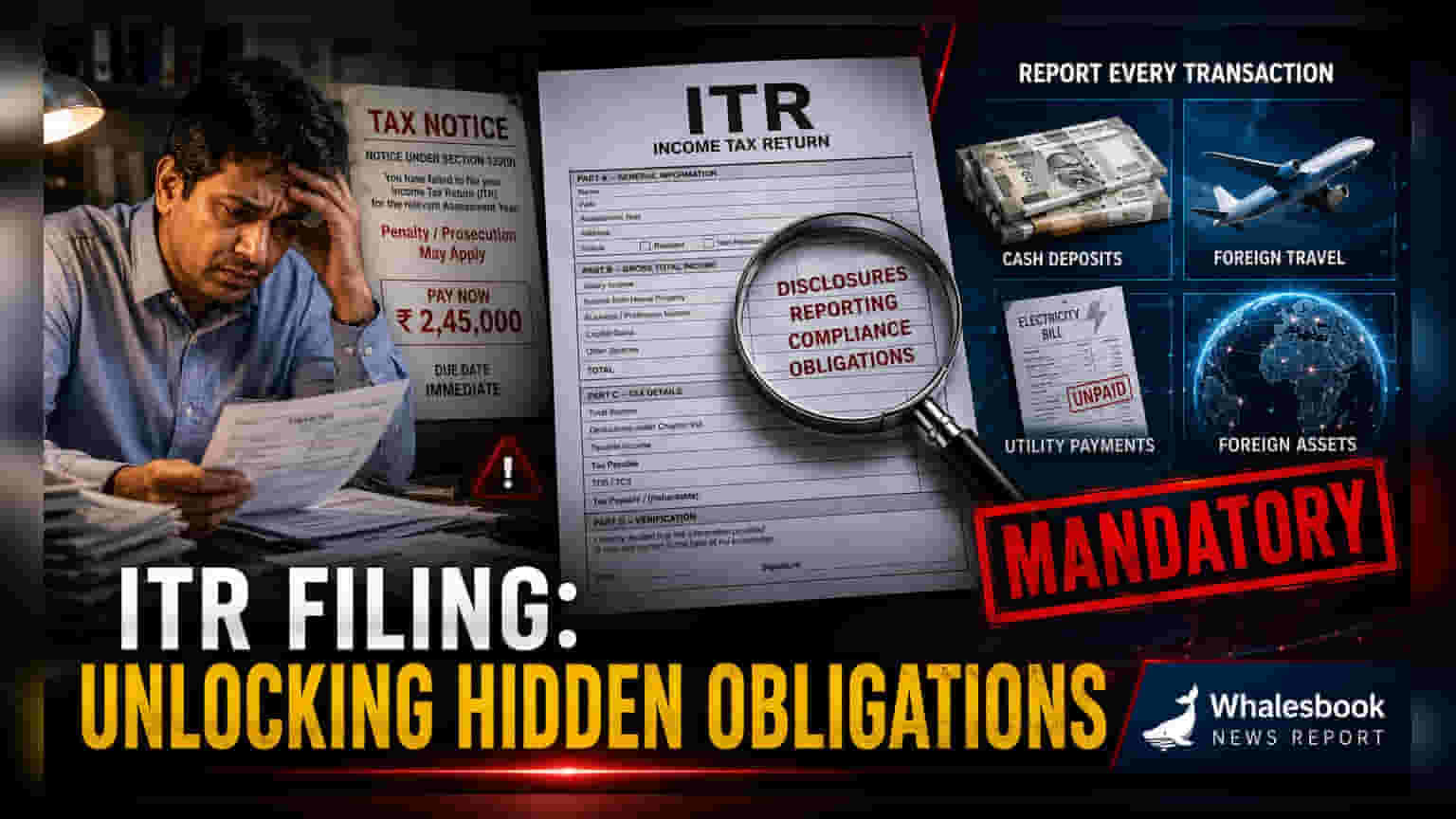

Banking and Financial Transaction Thresholds

Financial institutions are required to report high-value transactions to tax authorities. If an individual deposits a total of Rs 1 crore or more in one or more current accounts during a financial year, they must file an ITR. Similarly, an aggregate deposit of Rs 50 lakh or more in one or more savings bank accounts triggers the same requirement. These rules are designed to track significant cash flows and maintain financial transparency within the banking system.

Lifestyle and Discretionary Spending Indicators

Tax authorities use certain spending patterns as indicators of financial capacity. If you spend more than Rs 2 lakh on foreign travel for yourself or anyone else, you are required to file a return. Additionally, if your annual electricity bill exceeds Rs 1 lakh, it is considered an indicator of high discretionary spending, making ITR filing compulsory. These measures ensure that individuals with significant lifestyle expenses are within the tax reporting network, even if their declared income remains low.

TDS and International Asset Reporting

If you have been subject to Tax Deducted at Source (TDS) or Tax Collected at Source (TCS) totaling more than Rs 25,000 in a year, you must file a return. For senior citizens aged 60 and above, this threshold is set at Rs 50,000. Filing is necessary in these instances to process claims for any excess tax deducted. Furthermore, any resident Indian who holds assets abroad, such as foreign bank accounts, financial interests, or signing authority in foreign accounts, must file an ITR. This rule applies even if no income was generated from these foreign sources, as it aligns with international reporting requirements.

Business Compliance and Loss Reporting

For those involved in business, filing is mandatory if the total sales, turnover, or gross receipts exceed Rs 60 lakh in a financial year. If you have incurred losses from business or capital assets like shares and property, you must file your return by the designated due date. Failure to file on time prevents you from carrying these losses forward, meaning you cannot set them off against future profits to reduce your tax burden in later years.

Potential Risks of Non-Compliance

Ignoring these requirements can lead to more than just administrative trouble. Aside from a late filing fee of up to Rs 5,000, non-filers may face interest charges on any unpaid tax liability. Moreover, failing to file invites closer scrutiny from tax officials, which can lead to best-judgment assessments or the reopening of income files from previous years. Investors and taxpayers should ensure they review their financial records and bank statements to confirm compliance before the annual due date to avoid these potential complications.