Indian businesses are facing significant working capital pressure due to strict Input Tax Credit (ITC) validation rules. Because tax claims now depend on suppliers filing their returns on time, many companies are seeing their cash flow trapped, leading to operational stress.

What Happened

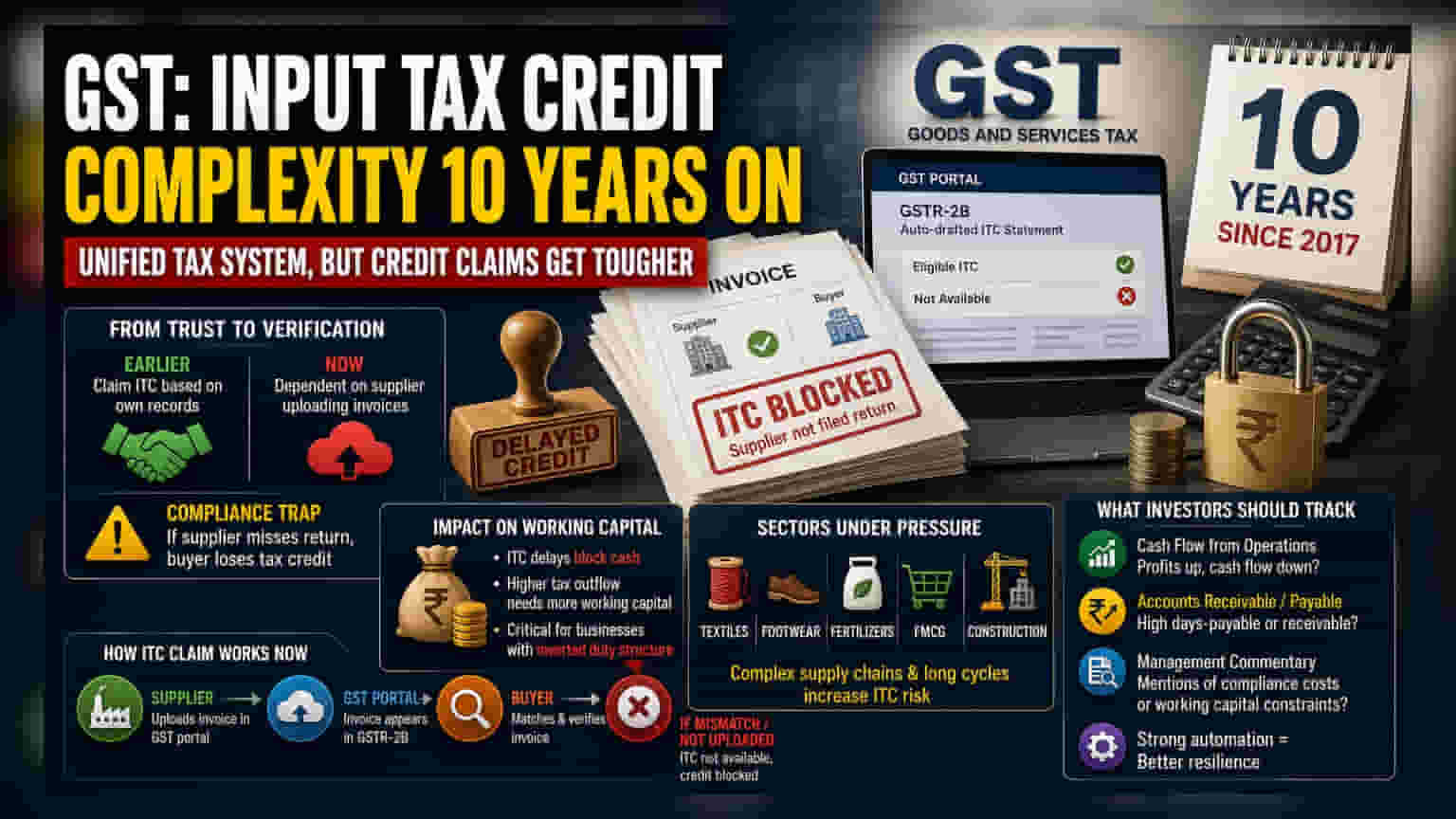

Nearly a decade since the launch of the Goods and Services Tax (GST) in 2017, the system has successfully unified India’s tax structure. However, the mechanism for claiming Input Tax Credit (ITC)—the tax a business pays on purchases and can adjust against the tax it collects on sales—has become significantly more complex. Businesses can no longer simply claim credit based on their own records. Instead, they must rely on their suppliers to upload invoices into the GST portal. If a supplier fails to file their return on time, the buyer is often unable to claim the credit, leading to cash flow delays.

The Compliance Trap

The current GST framework requires strict invoice matching between the buyer and the supplier. A key tool in this process is GSTR-2B, an auto-drafted statement that shows the taxes a business can claim as credit based on what suppliers have uploaded.

This has fundamentally changed how companies manage their finances. Previously, the system was more trust-based. Now, it is strictly verification-based. For a company, this means that even if they have paid their suppliers, they may be denied tax credit if the supplier has not correctly uploaded the invoice. This dependency creates a "compliance risk" where a company's financial health is partially tied to the discipline of its entire vendor network.

Impact On Working Capital

For investors, the most critical aspect of this change is the impact on working capital—the cash a company needs to run its daily operations. When ITC is delayed or denied, that money is effectively blocked. The company has to pay the full tax liability on its sales without the benefit of the credit it expected, which can force it to use more cash or borrow money to cover the gap.

This is particularly challenging for companies with long supply chains or those operating under an "inverted duty structure." In an inverted duty structure, the tax rate on raw materials is higher than the tax rate on the final product. These companies naturally accumulate excess tax credits that they claim as refunds. Any friction or delay in the credit validation process can significantly squeeze their cash reserves.

Sector Vulnerabilities

Certain sectors are feeling this pressure more acutely than others. Industries like textiles, footwear, fertilizers, and Fast-Moving Consumer Goods (FMCG) often deal with complex supply chains where credit reconciliation is difficult.

Additionally, construction firms often face unique challenges. They operate on long revenue cycles, meaning they incur significant upfront input costs and taxes long before they receive payment from clients. If their ITC is held up due to supplier non-compliance, it adds another layer of financial stress on top of their already capital-intensive business model.

What Investors Should Track

Investors looking at company performance should pay attention to how businesses manage their cash and supplier relationships. Key monitorables include:

- Cash Flow From Operations: If a company reports strong profits but weak cash flow, it may indicate that money is getting stuck in working capital or tax credit delays.

- Accounts Receivable and Payable: High days-payable and receivable can sometimes signal issues in the supply chain or difficulty in reconciling tax credits.

- Management Commentary: Look for mentions of "compliance costs" or "working capital constraints" in quarterly reports. Companies that have invested in strong automated systems to reconcile invoices with suppliers are generally better equipped to handle these complexities than those relying on manual processes.