The Valuation Mismatch and Liquidity Drain

The exodus from Indian equities is not merely a reaction to global AI fever but a calculated retreat from stretched domestic valuations. As the Nifty 50 and BSE Sensex grapple with high trailing P/E ratios compared to historical averages, international funds are finding more immediate yield in U.S. technology plays and fixed-income hedges. The rapid liquidity withdrawal indicates that institutional desks are prioritizing balance sheet protection over emerging market beta, effectively treating the Indian exchange as a funding source for high-conviction AI positions in Western markets.

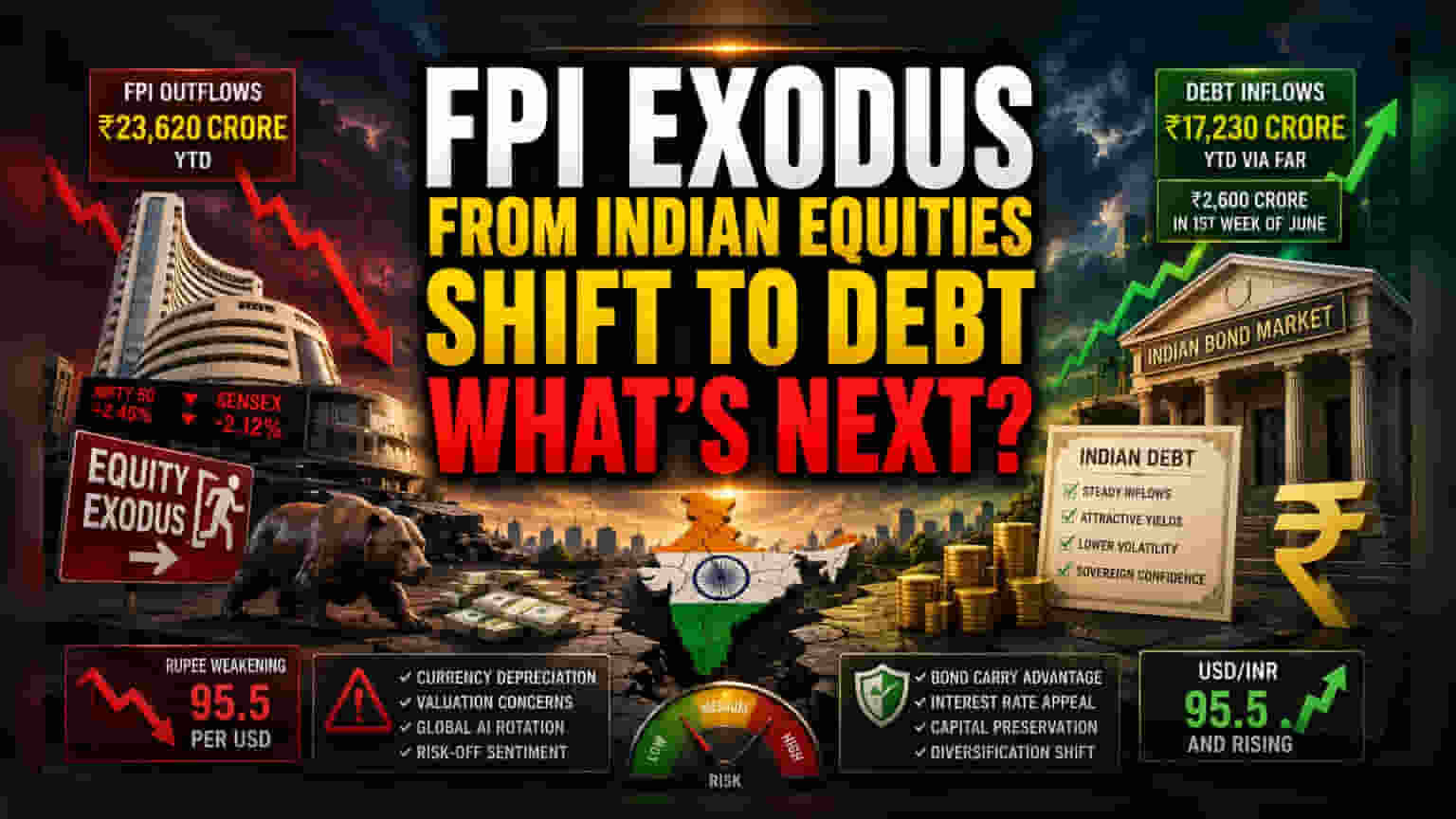

The Debt-Equity Divergence

While equity markets face relentless selling, the narrative of total abandonment misses the underlying shift into Indian debt. Year-to-date inflows into the Fully Accessible Route (FAR) segments have reached Rs 17,230 crore, with a notable Rs 2,600 crore entry in the first week of June alone. This suggests that while foreign capital is skittish toward equity volatility and currency depreciation, it remains tethered to India through the sovereign bond market. This dual behavior implies that investors are not exiting the country entirely but are re-balancing risk profiles to favor interest rate carry trades over domestic growth exposure.

The Forensic Bear Case: Currency and Carry Risk

The depreciation of the rupee toward 95.5 per dollar creates a structural headwind that no regulatory patch can easily overcome. For foreign investors, a weakening local currency erodes equity gains before they can even be repatriated. The Reserve Bank of India’s intervention, while intended to stabilize the exchange rate, has effectively created a ceiling on volatility that complicates hedge strategies for large-scale institutional players. Furthermore, the reliance on high-frequency trading algorithms in the Nasdaq means that any sustained correction in AI valuations will likely induce margin calls that force further selling in correlated emerging markets, potentially deepening the rout in Indian mid-caps that have yet to see their valuation premiums compressed.

Strategic Implications for Capital Flows

Looking ahead, the market is caught in a tug-of-war between speculative global capital and local institutional support. The sustainability of the current exodus depends heavily on the stabilization of the USD/INR pair. If the rupee continues its downward trajectory, the cost of hedging will render equity returns unattractive regardless of corporate performance. Investors are now watching the central bank’s next policy meeting for clues on whether the current tax exemptions and bond accessibility rules are sufficient to offset the mounting macro pressure, or if further aggressive monetary intervention will be required to stabilize the capital account.