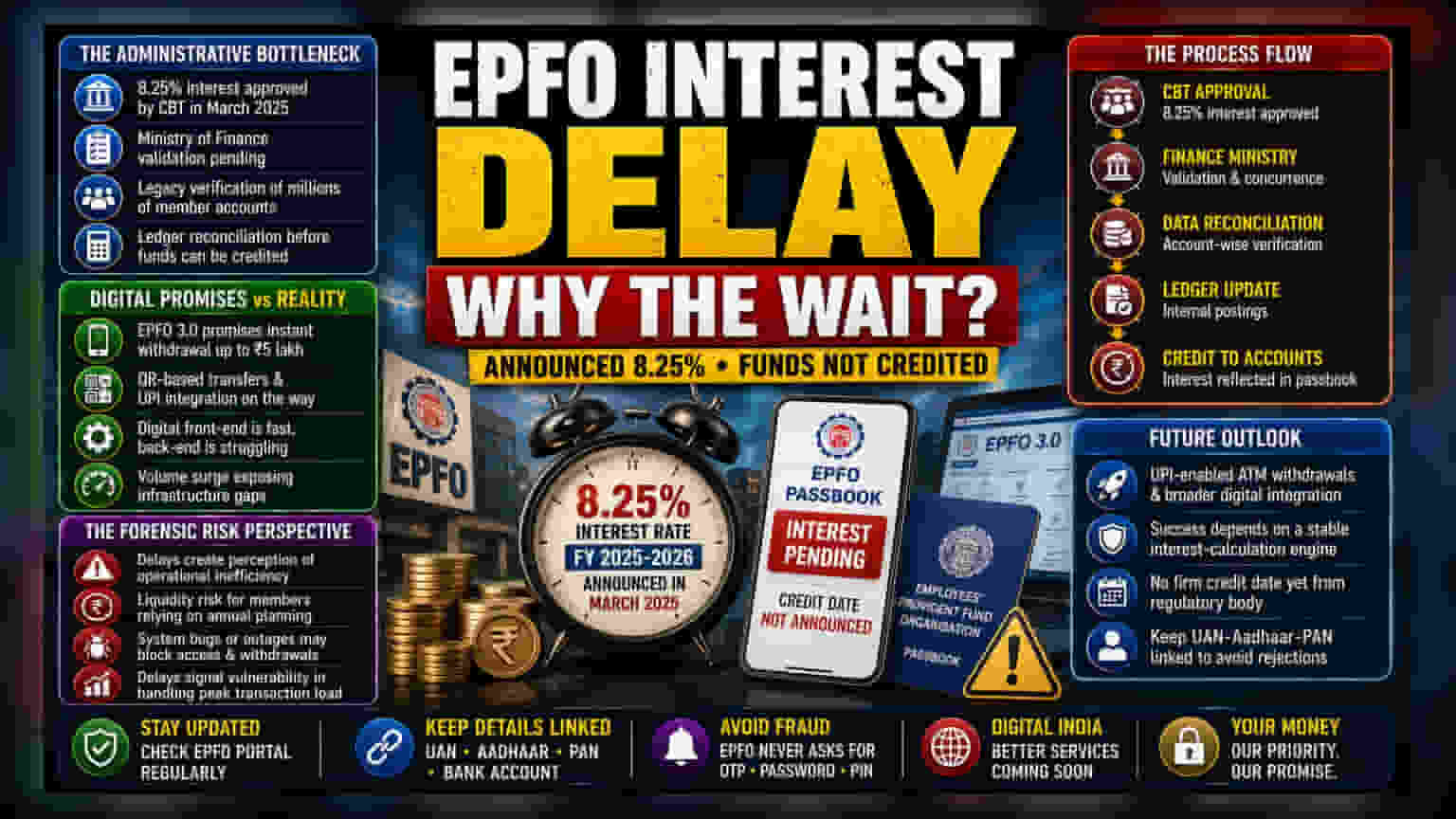

The Administrative Bottleneck

While the Central Board of Trustees signaled an 8.25% interest rate for the 2025-2026 fiscal year back in March, the capital remains absent from member passbooks. The discrepancy between the announcement and the actual cash flow stems from a rigid bureaucratic sequence involving Ministry of Finance validation and subsequent internal ledger reconciliation. Unlike private financial institutions that utilize automated real-time accounting, the EPFO relies on a legacy-heavy verification process that must reconcile millions of individual accounts against central government approvals before any interest can be legally distributed.

Digital Transformation vs. Operational Reality

The current delay stands in stark contrast to the aggressive marketing behind the EPFO 3.0 initiative. While management touts upcoming features like instant withdrawals of up to ₹5 lakh and QR-based transfers, the struggle to finalize standard interest payouts reveals a disconnect between front-end digital promises and back-end processing power. Market observers note that the agency often prioritizes systemic stability over speed, yet the extended wait time suggests that the underlying infrastructure may be struggling to keep pace with the massive volume of data generated by an expanding subscriber base.

The Forensic Risk Perspective

From an institutional standpoint, the inability to execute predictable interest payments creates a perception of operational inefficiency. For the average subscriber, the lack of a firm credit date introduces unnecessary liquidity risk, particularly for those relying on these funds for annual financial planning. Furthermore, if the EPFO 3.0 transition encounters additional software bugs or server outages, members may face prolonged difficulty accessing their balances or initiating the new, supposedly seamless withdrawal processes. Historical precedent suggests that these delays are rarely malicious but indicate a systemic vulnerability in the organization’s capability to handle sudden increases in transaction volume during peak update cycles.

Future Outlook

Guidance from the regulatory body remains non-committal, offering no concrete timeline for the funds to hit individual accounts. As the organization pivots toward UPI-enabled ATM withdrawals and broader digital integration, the success of these programs will hinge on stabilizing the foundational interest-calculation engine. Subscribers are currently advised to maintain their UAN-Aadhaar-PAN linking status, as any technical mismatch in the portal will likely lead to further individual account rejections once the bulk credit process finally begins.