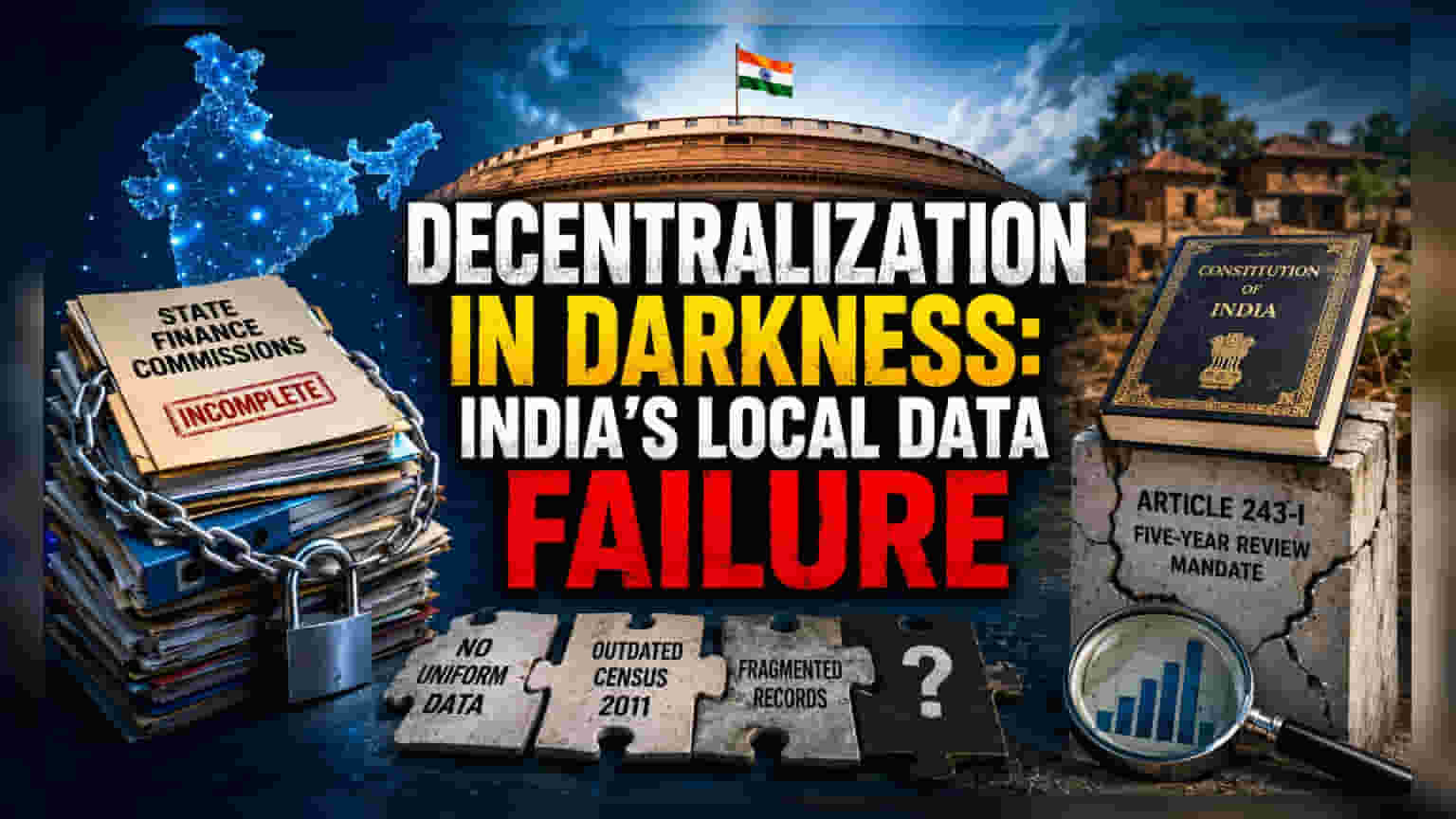

The Structural Data Blackout

The long-standing disconnect between constitutional mandate and administrative reality has reached a breaking point. A newly released report from the Ministry of Panchayati Raj confirms that India’s fiscal architecture is suffering from a structural data void at the grassroots level. While Article 243-I of the Constitution requires State Finance Commissions (SFCs) to review and recommend the financial devolution for Panchayati Raj Institutions every five years, these bodies have been forced to function without a reliable, integrated database. This absence of disaggregated financial, demographic, and asset-management data means that the foundational pillar of local self-governance is essentially relying on estimation rather than evidence-based analysis.

Impact on Fiscal Decentralization

Fiscal decentralization is intended to empower local bodies by aligning resources with functional needs. However, the current reality involves fragmented, siloed datasets that prevent a coherent national assessment. Because financial records across states utilize inconsistent accounting standards, they remain incomparable, effectively preventing a uniform understanding of rural service delivery costs. Chief Economic Adviser Dr. V. Anantha Nageswaran noted during the report's launch that without a systematic, independent assessment of what has been devolved versus what was promised, the system is essentially flying blind. This analytical thinness undermines the efficacy of constitutional transfers, as funds are disbursed without clear visibility into recipient requirements, thereby weakening the accountability mechanism that the 73rd Constitutional Amendment sought to establish.

The Operational Crisis

Beyond the headline data gaps, the report identifies a cascade of institutional failures that hamper the SFCs' effectiveness. These include severe capacity constraints at the local government level, frequent delays in the constitution of commissions, and a persistent reliance on outdated benchmarks, such as the 2011 Census figures. While digital platforms like eGramSwaraj and the Panchayat Advancement Index have been deployed, the committee highlighted that they remain insufficient for the high-level analytical demands of modern fiscal governance. Furthermore, the lack of uniform accounting heads makes it nearly impossible to reconcile central transfers with state-level grants, leaving a significant portion of local body funding unaccountable.

The Future Outlook

To mitigate these systemic risks, the committee has urged the adoption of a rigorous, standardized fiscal database across all states. A primary recommendation includes the implementation of a performance audit by the Comptroller and Auditor General of India (CAG) to track actual fund flows and create an evidence base that currently does not exist. The proposal to establish dedicated SFC Cells within state administrations aims to professionalize the data collection process, shifting the focus from ad-hoc estimations to structured, transparent financial planning. Whether these reforms can bridge the gap between constitutional intent and administrative performance will depend entirely on the urgency with which state governments align their accounting practices with these new national standards.