Crisil Ratings projects a moderate 100 basis point decline in India Inc's operating margins this fiscal, easing fears of a steeper 200 basis point drop following the Strait of Hormuz's reopening. While energy costs have cooled, businesses still face a slow normalization of gas and urea supplies. Investors should watch for sector-specific pressures and potential macroeconomic headwinds.

What Happened

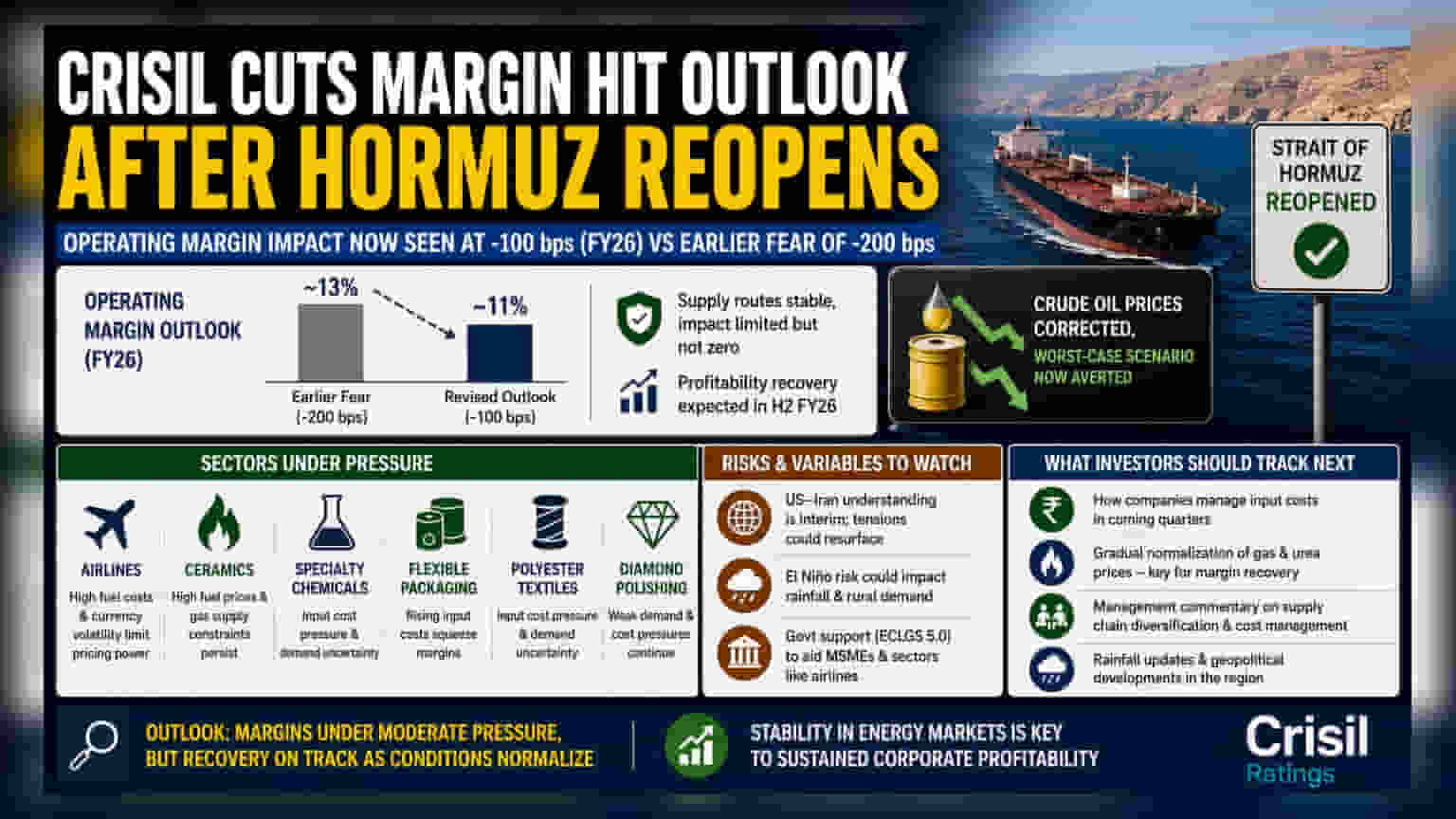

Crisil Ratings has revised its outlook on Indian corporate profitability following the reopening of the Strait of Hormuz. The agency now expects a 100 basis point decline in operating margins for Indian companies this fiscal year, bringing them to approximately 11%. This is a notable improvement from earlier market fears, which had projected a sharper 200 basis point impact due to potential conflict-driven supply disruptions. While crude oil prices have corrected following the easing of tensions, the agency notes that the availability of critical inputs like natural gas and urea will recover only gradually.

What This Means For Company Profits

Operating margins represent the profit a company retains from its revenue after paying for day-to-day operating expenses, such as raw materials, wages, and energy. When geopolitical tensions disrupt supply routes, companies often face higher fuel and transportation costs, which squeeze these margins. The latest projection suggests that while the overall impact on profitability is limited, it is not zero. For investors, this implies that while the worst-case scenario for earnings has likely been avoided, companies may still face some cost pressure compared to the previous year. Profitability recovery is expected to be more visible in the second half of the fiscal year.

Sectors Under The Spotlight

Not all industries are affected equally by these energy price dynamics. Crisil highlights that some sectors remain vulnerable despite the easing of tensions. Airlines are particularly sensitive, as they face the dual challenge of high fuel costs and currency fluctuations, which can limit their pricing power. Similarly, ceramics manufacturers continue to grapple with high fuel prices and potential gas supply constraints, which are essential for their production processes. Other segments, including specialty chemicals, flexible packaging, polyester textiles, and diamond polishing, are also expected to see margin pressure due to lingering input cost challenges and demand uncertainty.

Risks And Variables To Watch

While the situation regarding the Strait of Hormuz has stabilized, the outlook is not entirely without risks. Crisil has pointed out that the current understanding between the US and Iran is interim, meaning geopolitical tensions could flare up again. Furthermore, the Indian economy faces other domestic variables, such as the potential impact of El Niño, which could affect rainfall patterns and rural demand. If rural consumption slows, it could create a headwind for companies that depend on the domestic market for volume growth. Investors should also watch for government support initiatives, such as the Emergency Credit Line Guarantee Scheme (ECLGS) 5.0, which are aimed at providing credit access to MSMEs and helping specific sectors like airlines navigate these costs.

What Investors Should Track Next

The key monitorable for investors will be how companies manage their input costs over the coming quarters. The gradual normalization of gas and urea prices will be a critical indicator of whether companies can effectively protect their margins. Monitoring management commentary in upcoming quarterly results will be essential to see how businesses are diversifying their supply chains and managing the impact of fluctuating energy costs. Additionally, updates on rainfall data and any changes in the geopolitical stability of the region will continue to be important factors influencing the broader market sentiment.