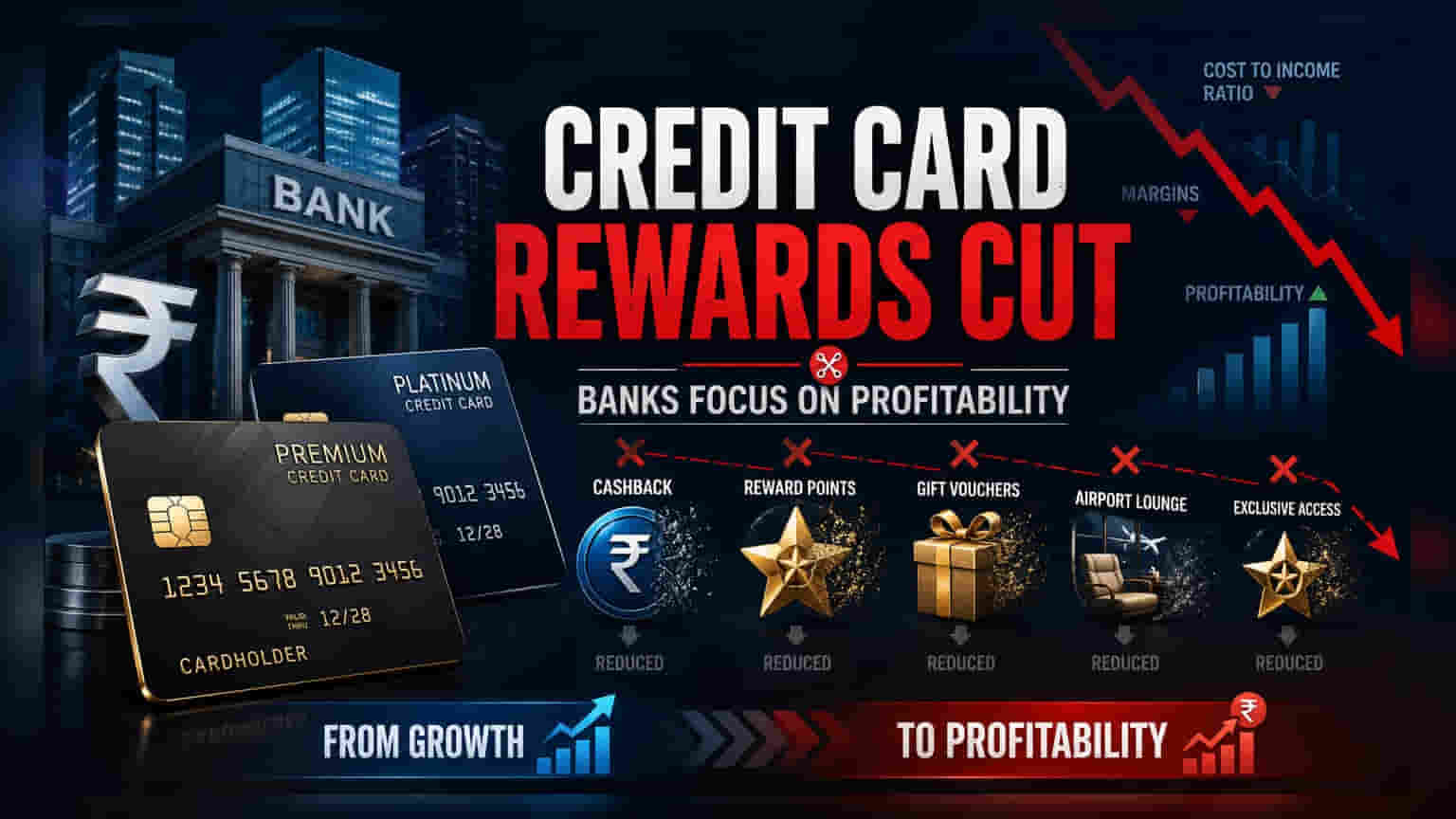

Indian banks are increasingly trimming credit card rewards to manage rising costs and defend profit margins. This shift reflects a maturing market where lenders prioritize profitability over aggressive customer acquisition. Investors tracking the banking sector should watch how these adjustments influence customer retention and the overall cost-to-income ratio in upcoming quarterly reports.

The Shift in Credit Card Rewards

In recent quarters, several Indian lenders have begun modifying their credit card reward programs, often reducing benefits or tightening eligibility criteria for premium cards. While these rewards were initially used as a primary tool to acquire customers and boost transaction volumes, the strategy is undergoing a subtle transformation. As the credit card market matures, banks are shifting their focus from pure market share growth to improving the profitability of their retail portfolios.

Why Banks Are Changing Strategies

Credit card businesses are lucrative but capital-intensive, involving high costs for customer acquisition, technology, and rewards. For banks, the goal is to balance these costs against the revenue generated from interest on revolving credit and merchant transaction fees. When economic conditions pressure margins, or when the cost of acquiring new customers rises, lenders often look at reward programs as a lever to improve operational efficiency. By devaluing rewards, banks can reduce their immediate cash outflows, which helps in maintaining healthy profit margins during competitive periods.

The Financial Impact on Lenders

For investors, the key area of impact is the cost-to-income ratio. A credit card business that relies heavily on expensive reward programs can see its margins shrink if transaction growth does not offset the reward payout costs. When a bank reduces these perks, it is essentially trying to lower the cost of doing business. However, there is a risk involved: if customers perceive the card as less valuable, they may switch to competitors, potentially increasing customer churn. The success of this strategy depends on whether the bank can retain high-spending customers despite the reduction in benefits.

The Competitive Landscape

Major players in the Indian credit card space, such as HDFC Bank, SBI Card, ICICI Bank, and Axis Bank, operate in a highly competitive environment. When one major issuer adjusts its reward structure, it often creates a ripple effect across the sector. Investors should note that while this move supports short-term profitability, it also signals that the phase of aggressive, reward-driven growth may be cooling down in favor of more sustainable, unit-economic-focused performance.

What Investors Should Monitor

Investors tracking financial stocks should pay close attention to management commentary regarding retail asset quality and cost-to-income ratios in upcoming earnings calls. If banks report a slowdown in new card additions or a rise in card attrition rates after reward cuts, it could indicate that the strategy is affecting customer loyalty. Conversely, a stable or improving margin profile despite these changes would suggest that the lenders are successfully balancing profitability with customer retention. Tracking the spread between interest income and operational costs will remain a key monitorable for the banking sector.