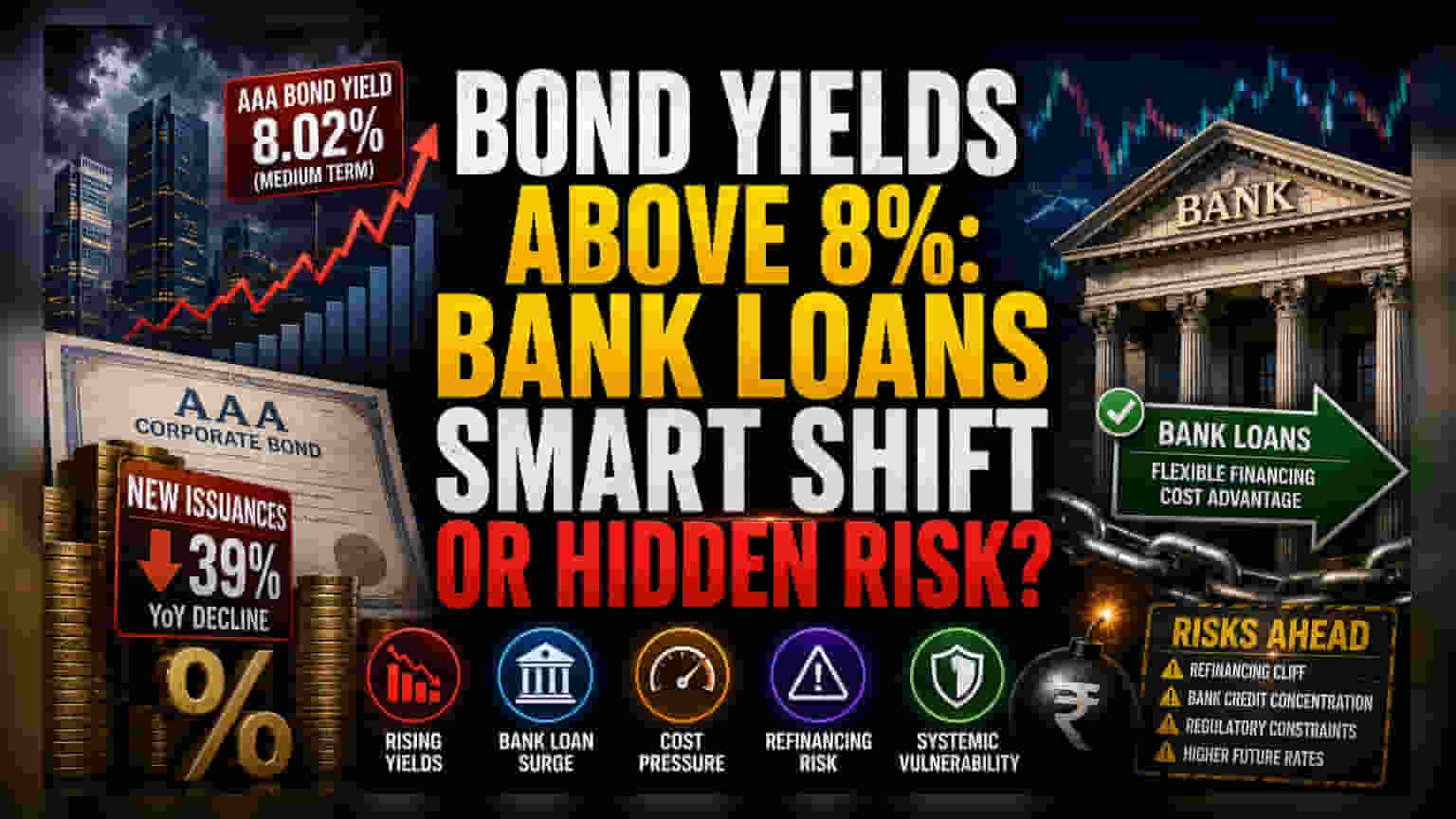

The Cost-of-Capital Inflection Point

Fixed-income markets are undergoing a structural repricing as AAA-rated bond yields for medium-term maturities climb above the 8% threshold. This movement signifies a critical departure from the low-interest-rate environment that supported corporate balance sheet expansion over the past three years. As the gap between market-determined yields and institutional bank lending rates widens, the traditional preference for bond-market financing is eroding, compelling issuers to prioritize bank credit facilities to avoid locking in historically expensive, long-term liabilities.

Analyzing the Institutional Pivot

Recent data indicates a marked decline in debt capital market activity, with new issuances dropping nearly 39% compared to the same period last year. This contraction is not merely a reaction to current central bank policy but a preemptive adjustment by treasurers fearing further liquidity drainage. While the Reserve Bank of India maintains a hawkish stance to curb inflationary pressures, the burden is falling disproportionately on capital markets. Unlike the corporate bond space, where pricing is immediate and sensitive to interest rate expectations, bank lending portfolios often exhibit a lag, providing a temporary, albeit shrinking, cost advantage for borrowers. This arbitrage opportunity is currently fueling a surge in bank credit uptake among major non-banking financial entities.

The Forensic Bear Case: Structural Vulnerabilities

This migration from bonds to bank loans introduces a secondary layer of systemic risk. By relying heavily on bank credit, corporations are concentrating their liability risk within the banking sector, which is already managing elevated credit growth. Furthermore, the reliance on short-term bank borrowings instead of longer-tenured bonds risks creating a refinancing cliff should the central bank maintain current restrictive policies for a duration longer than anticipated. Unlike the bond market, where institutional investors provide a degree of diversification, bank balance sheets may face sudden constraints if regulators impose stricter capital adequacy requirements or asset-liability mismatch mandates in response to this rapid credit expansion. Companies failing to secure long-term, fixed-rate debt now may find themselves vulnerable to margin compression if they are forced to roll over debt at even higher floating rates later in the fiscal year.

Macro-Economic Implications

Looking ahead, the outlook for debt capital markets remains constrained by the interplay of persistent inflation and central bank policy. Analysts anticipate that until volatility in the sovereign yield curve subsides, the primary market for corporate bonds will remain dormant, reserved only for issuers with immediate refinancing needs. The broader trend suggests a consolidation of power among top-tier commercial banks, which now hold significant leverage over corporate funding access, potentially altering the competitive dynamics of the Indian financial sector for the remainder of the fiscal year.