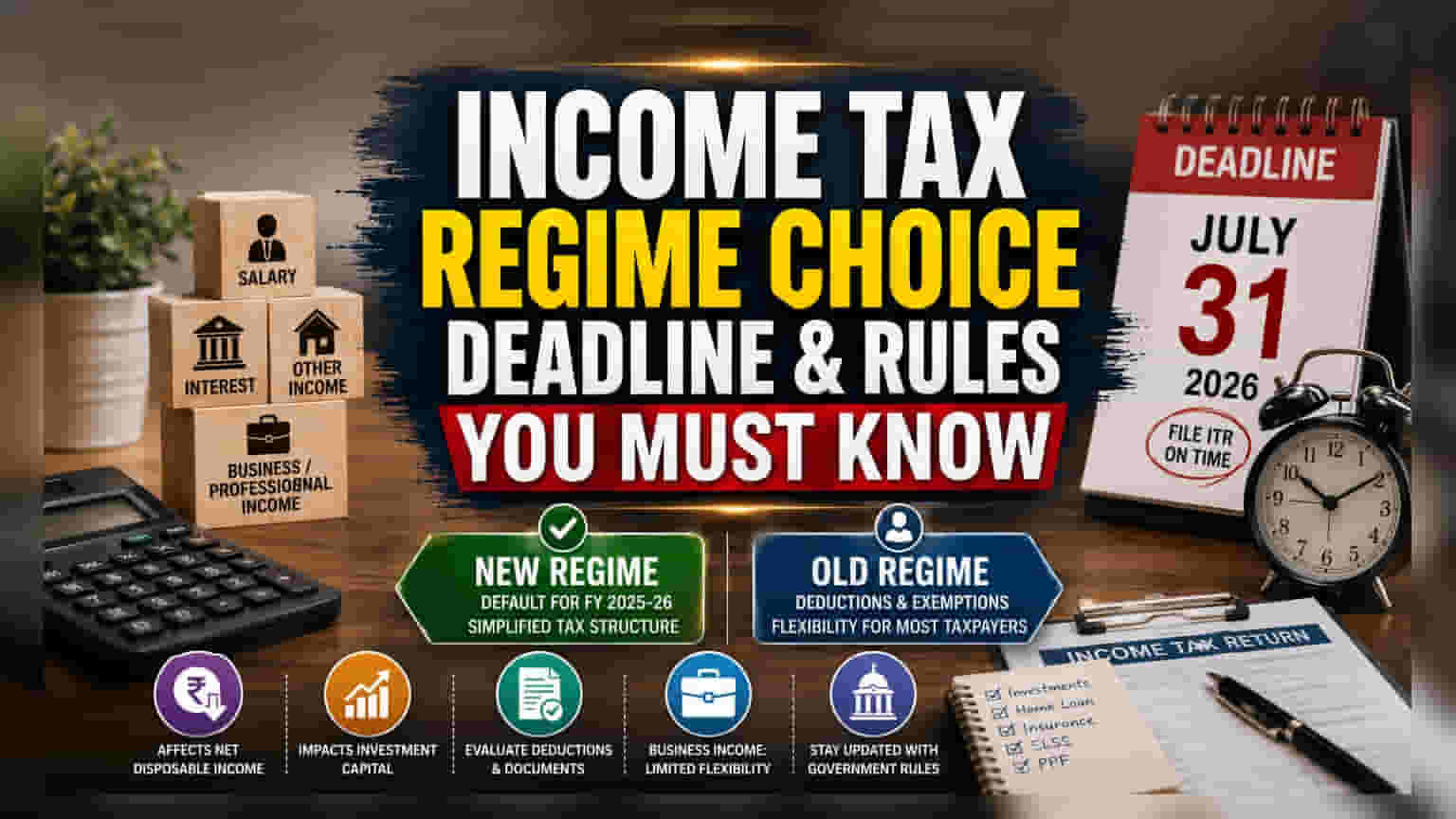

As taxpayers prepare for the July 31, 2026, filing deadline for FY 2025-26, understanding the nuances between the old and new tax regimes is essential. While the new regime is the default, salaried individuals retain annual flexibility, whereas those with business income face stricter constraints. This choice directly impacts net disposable income and tax efficiency.

What Happened

For the financial year 2025-26, the new income tax regime serves as the default system for taxpayers in India under Section 115BAC of the Income Tax Act. While the government has simplified the tax structure, taxpayers still retain the ability to opt for the old tax regime, which allows for various deductions and exemptions. However, the rules governing this choice differ significantly based on the source of an individual's income.

The Flexibility Gap

The ability to switch between tax regimes depends largely on the nature of a taxpayer's income. Individuals whose income is primarily from salary, interest, or other sources—excluding business or professional income—have the freedom to select either the old or new regime each financial year. This flexibility allows them to align their tax strategy with their current financial situation, such as taking advantage of specific deductions if they have significant tax-saving investments or expenses like home loan interest.

Conversely, taxpayers with business or professional income face a more rigid framework. Once a taxpayer with business income opts for the old tax regime, this decision is not as flexible. They are generally restricted from frequently switching back and forth. This rule is designed to ensure stability in the tax positions of businesses, as their financial planning often involves long-term considerations like depreciation calculations and the treatment of losses.

Why the Deadline is Crucial

The July 31, 2026, deadline is a vital monitorable for all taxpayers. Failing to file the income tax return by this date removes the opportunity to opt for the old regime. If the deadline is missed, the default new tax regime will apply automatically, regardless of whether the old regime would have been more tax-efficient for the individual. This underscores the importance of timely filing and proactive tax planning.

Investor Context and Monitorables

For investors, the choice of tax regime directly affects net disposable income—the money left after taxes that can be directed toward savings, investments, or expenses. A higher tax outgo under the default new regime could reduce the capital available for investment, while selecting the old regime might necessitate maintaining certain tax-saving investments to claim deductions.

Investors should monitor their specific income streams and evaluate their documentation for any tax-saving investments that qualify under the old regime. If an investor has business income, they should consider the long-term implications of their choice, as the restricted flexibility makes it a strategic decision rather than a simple annual calculation. It is also important to track any updates from the Central Board of Direct Taxes regarding filing procedures or potential changes to the tax structure, as government policy remains the final authority on these provisions.