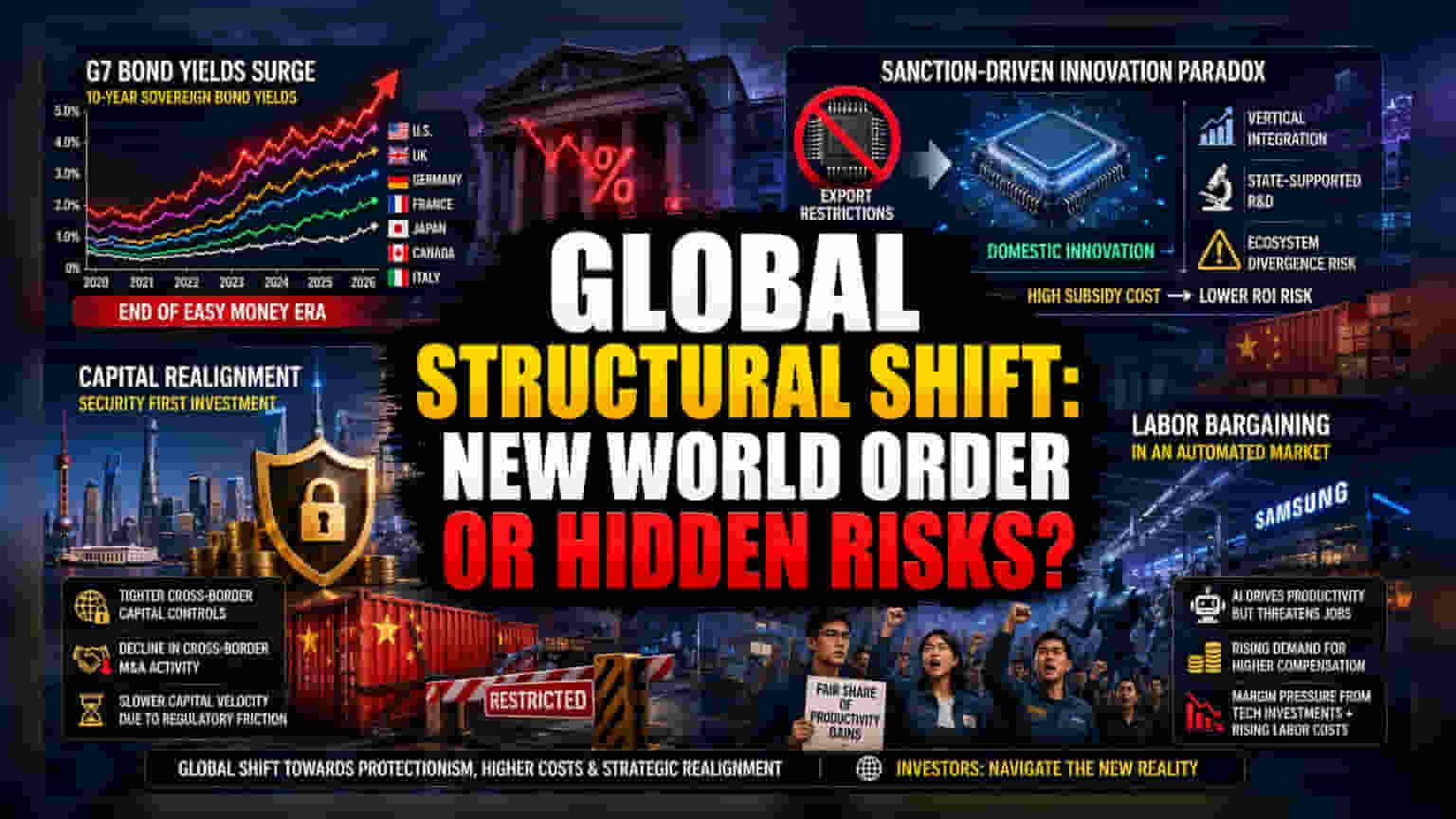

The Yield Environment and Structural Drag

The current escalation in long-term sovereign bond yields across the G7 represents more than just a reaction to inflationary pressures. It marks the formal termination of the post-2008 era of easy money. By effectively raising the hurdle rate for capital expenditure, these elevated yields are forcing a shift in corporate strategy from aggressive expansion to defensive optimization. This transition is not merely financial; it reflects a broader macro-structural shift where governments prioritize debt sustainability and domestic industrial resilience over the historical preference for globalized supply chain efficiency.

The Sanction-Driven Innovation Paradox

External containment policies are inadvertently creating a new form of industrial isolationism that prioritizes domestic sovereignty over market integration. The experience of firms operating under severe export restrictions demonstrates that state-sponsored R&D can temporarily circumvent technological blockades by focusing on vertical integration. However, this model carries a heavy premium. While these entities may achieve architectural breakthroughs in semiconductors or software, the loss of access to global ecosystem standards creates a long-term risk of divergence. The cost of maintaining this parallel tech infrastructure requires massive subsidies, which may ultimately depress return on invested capital for the broader regional market.

Capital Realignment and National Security

Beijing’s pivot toward a security-first investment mandate represents a contraction in global liquidity that will likely impact emerging markets and infrastructure projects worldwide. By tightening oversight on cross-border capital flows, the state is signaling that financial internationalization is secondary to domestic stability. This shift will likely lead to a decline in cross-border M&A activity, as potential targets face increased due diligence and regulatory friction. Institutional investors should anticipate a decrease in the velocity of capital as these new vetting procedures are fully integrated into deal-making workflows.

Labor Bargaining in an Automated Market

The integration of artificial intelligence has transitioned from a theoretical efficiency tool to a primary driver of industrial labor disputes. In advanced manufacturing economies, the threat of displacement is being met with demands for premium compensation. This trend suggests that corporations are losing the ability to dictate wage terms unilaterally. As firms like Samsung face pressure to increase bonuses, it reveals a structural bottleneck where the deployment of expensive AI technology must be financed simultaneously with rising labor costs. This squeeze on operating margins is likely to persist as unions pivot from job preservation to demanding a direct share of the productivity gains generated by automated systems.