Rate Cuts Reached Borrowers Unevenly

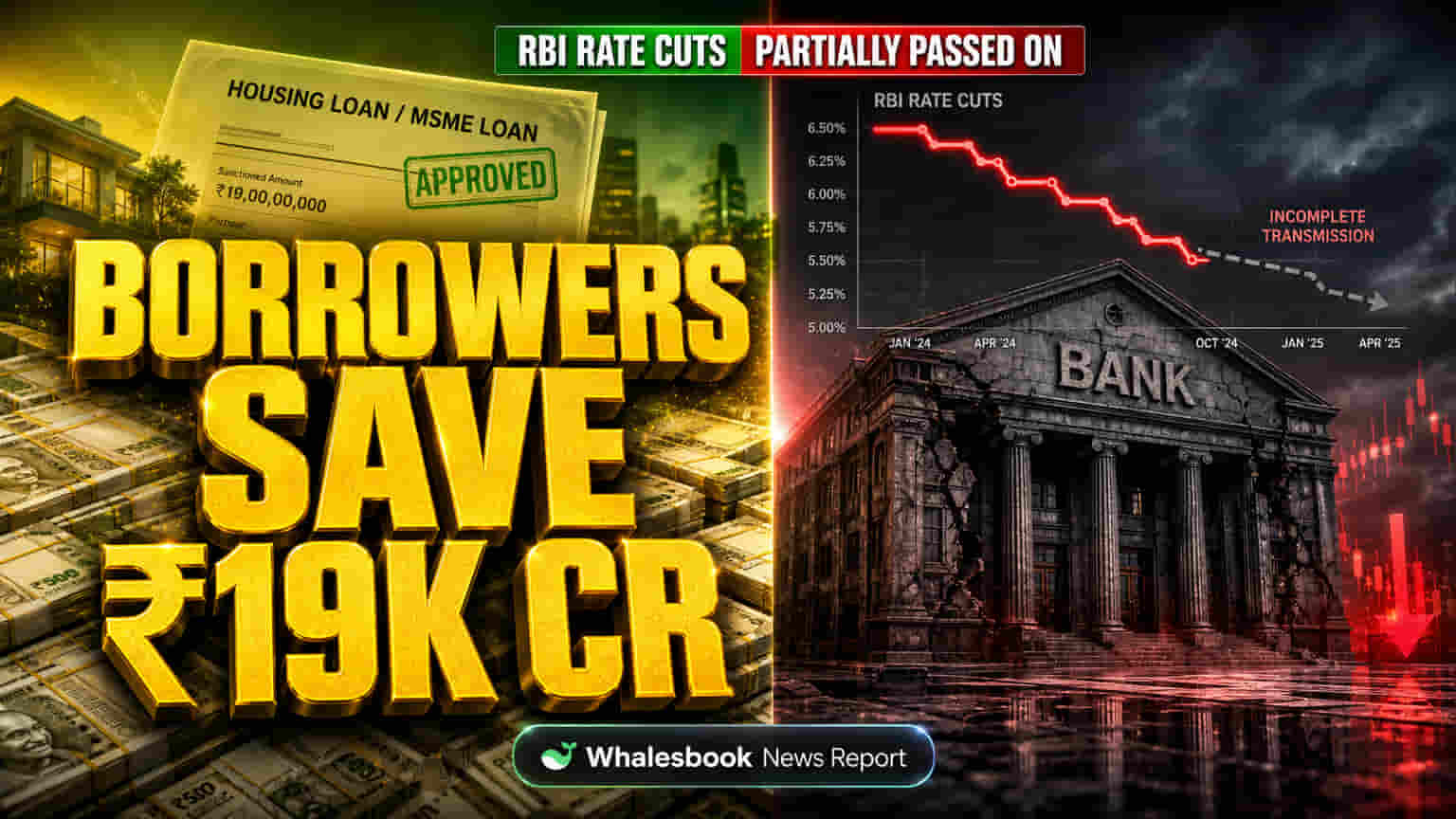

The Reserve Bank of India's (RBI) effort to lower borrowing costs by cutting the repo rate 125 basis points during fiscal year 2026 had mixed results, highlighting a key challenge for India's banking sector: balancing economic stimulus with the need for banks to maintain profits. Bank of Baroda's detailed analysis shows this policy easing was not fully passed on to borrowers. While the weighted average lending rate (WALR) on new loans decreased by about 93 basis points, the median Marginal Cost of Funds-based Lending Rate (MCLR) adjusted by only 45 basis points. This difference shows that while borrowing costs fell, the full benefit of the RBI's planned relief didn't reach all borrowers equally. Bank of Baroda, with a market capitalization of ₹45,000 crore and a P/E ratio of 12.5x, operates within this complex environment.

Bank Types Show Different Pass-Through Speeds

Banks' strategies for managing deposit rates to protect their profit margins (NIMs) also influenced these benchmark rates. The report highlights differences by bank type. Foreign and private sector banks passed on rate cuts faster, mainly because more of their loans are tied to external benchmarks (EBLR). Foreign banks had about 94% of loans on EBLR, and private banks 89%. Public sector banks, with only 51% of loans on EBLR, were slower to pass on the cuts. This variation can give banks with more flexible rate-setting abilities a competitive edge. For comparison, Bank of Baroda's P/E is 12.5x, while HDFC Bank trades around 20x and State Bank of India at 10x.

Loan Types Saw Varied Rate Reductions

Rate cuts also differed greatly by loan type. Unsecured retail loans had the highest rates (averaging 10.1%), followed by agriculture loans (9.81%). Rupee export credit had the lowest rates (6.78%). Within retail, housing loans were 7.63%, while vehicle and education loans were over 9%. The biggest rate drops occurred in export credit and education loans, falling over 160 basis points. MSME and unsecured retail loans also saw significant reductions, closer to the repo rate cut. Agriculture, professional services, and large industry loans experienced smaller rate decreases.

Borrower Savings and Economic Boost

Borrowers saved an estimated ₹19,000 crore overall due to lower interest costs, with housing and MSME loans seeing the biggest relief. However, the slower rate cuts for some loan types and public sector banks meant the economy didn't get the full boost expected from lower borrowing costs. This could unfairly impact small businesses and retail borrowers not on external rates, potentially slowing investment and spending.

Questions on Rate Cut Effectiveness

The Bank of Baroda report implicitly questions how effective monetary policy is within India's current banking setup. The large difference in how quickly public sector banks pass on rate cuts compared to private and foreign banks points to a structural issue. Critics suggest public sector banks prioritize protecting profit margins over quickly passing on rate cuts. This inertia or strategic profit management buffers banks from rate swings but weakens the impact of RBI's actions on the wider economy. Concerns about loan quality, especially in unsecured retail and MSME loans, also persist, potentially making banks hesitant to cut rates aggressively. Analyst views on Bank of Baroda are mixed; some see its valuation as attractive, while others point to potential challenges in profit and loan quality compared to more nimble private banks.

Market Outlook and Bank of Baroda's Position

With interest rates stabilizing, lending rates are unlikely to change much soon, unless the RBI signals a policy shift. Markets will watch how banks adapt to new regulations and competition. Analysts generally believe the banking sector has gained from economic recovery, but the complex way rate cuts are passed on means the full benefit of lower rates won't be shared equally. For example, price targets for Bank of Baroda suggest little immediate upside, due to ongoing challenges in profit margins and the competitive market.