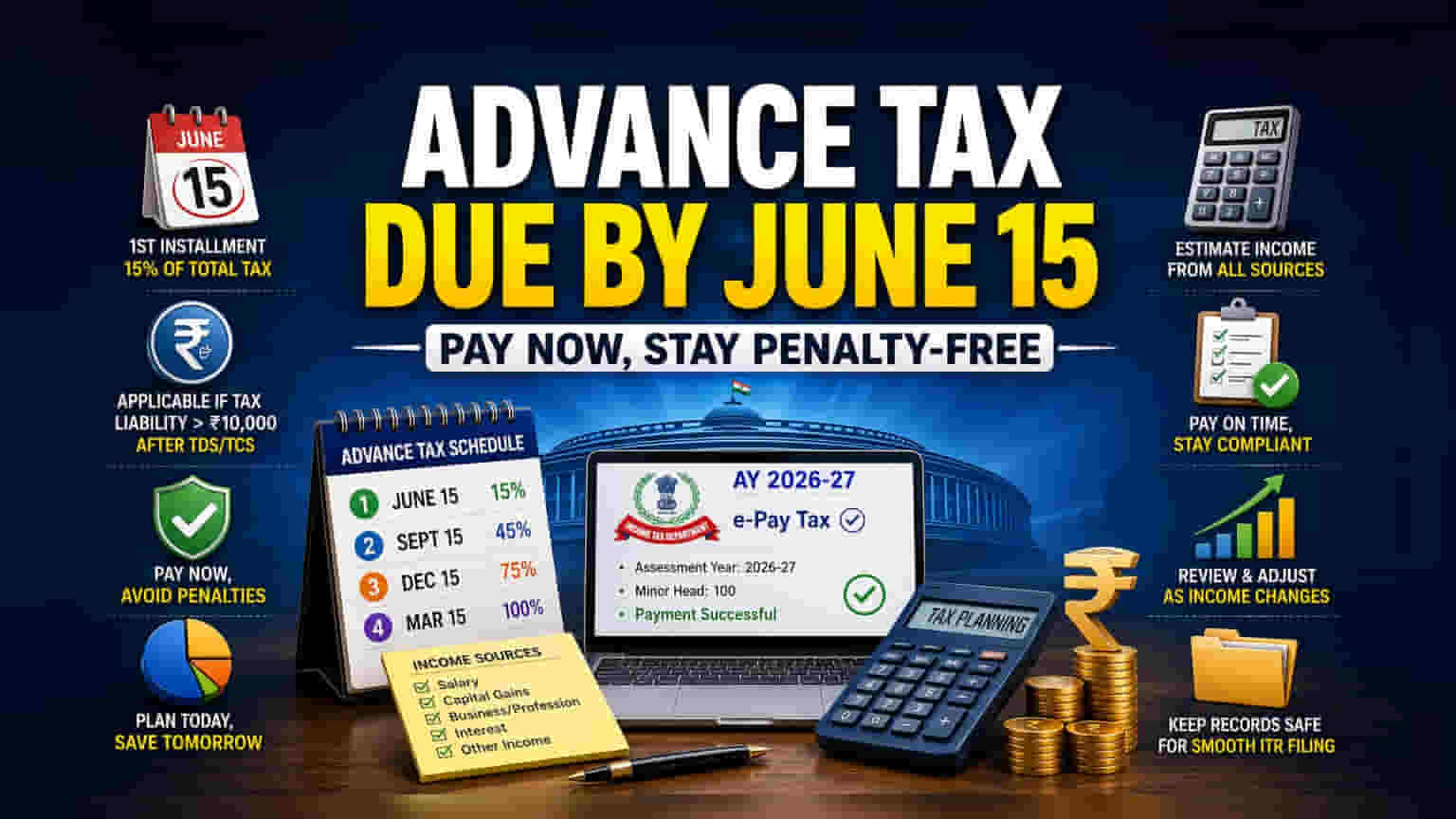

The first advance tax installment for FY 2026-27 is due by June 15. Investors and taxpayers with an estimated tax liability exceeding Rs 10,000—after considering TDS and TCS—must pay at least 15% of their total tax to avoid interest penalties under the latest Income Tax provisions.

What Happened

The first installment of advance tax for the Financial Year 2026-27 is due by June 15. Under India’s “pay-as-you-earn” tax system, taxpayers whose total estimated tax liability for the year exceeds Rs 10,000—after accounting for Tax Deducted at Source (TDS) and Tax Collected at Source (TCS)—are required to pay their taxes in quarterly installments. For this first installment, taxpayers are expected to deposit at least 15% of their total estimated tax liability.

Why This Matters For Investors

Many investors mistakenly believe that tax is only a year-end responsibility settled during Income Tax Return (ITR) filing. However, market-linked income such as capital gains from stock trading, profits from Futures & Options (F&O), dividends, and interest income often do not have sufficient TDS coverage. When these income sources push an individual’s annual tax liability above the Rs 10,000 threshold, advance tax payments become mandatory. Failure to estimate and pay this tax on time can lead to interest penalties, increasing the overall cost of tax compliance.

Understanding The Penalty Provisions

Under the current framework of the Income Tax Act, 2025, non-compliance or underpayment of advance tax attracts interest charges. Specifically, Section 424 (which corresponds to the former Section 234B) levies interest if less than 90% of the total tax due is paid by the end of the financial year. Additionally, Section 425 (corresponding to the former Section 234C) applies if installments are not paid according to the prescribed schedule. In both cases, interest is typically charged at 1% per month on the unpaid or short-paid amount. These provisions are designed to ensure the government receives a steady revenue stream throughout the year, rather than a single lump sum at the end.

Who Needs To Pay

Advance tax applicability is broad. It includes salaried individuals who have significant income outside of their salary, such as rental income or substantial interest from fixed deposits. For traders and investors, profits from stock market activities are treated as business income or capital gains and must be factored into the advance tax estimation. Freelancers and consultants, who often do not have a standard TDS mechanism covering their entire income, must also self-assess and pay advance tax. Resident senior citizens aged 60 years or above are exempt from advance tax, provided they do not derive any income from a business or profession.

How To Estimate And Pay

Calculating advance tax requires an estimation of your total income for the entire financial year. Investors should aggregate income from all sources—salary, business, capital gains, and interest—and subtract applicable deductions. After accounting for any TDS that has already been deducted, the remaining tax liability determines the advance tax amount. Payments can be made through the Income Tax Department’s e-filing portal under the ‘e-Pay Tax’ section. Taxpayers should ensure they select the correct assessment year (AY 2026-27) and the appropriate minor head code (Code 100) to ensure the payment is credited correctly.

What Investors Should Track

As the financial year progresses, market conditions and personal income can fluctuate. Investors should periodically review their tax estimation, particularly if capital gains from stock market transactions turn out to be higher or lower than initially expected. If income increases significantly during the year, subsequent installments in September, December, and March should be adjusted to meet the total liability and avoid potential penalties. Keeping a record of all tax challans and payment receipts is essential for a smooth ITR filing process later.