Big Tech is pivoting from self-funded growth to massive debt issuance to finance AI infrastructure. With capital expenditures ballooning toward a projected $1 trillion by 2027, the shift signals an aggressive, credit-fueled arms race that threatens to reset global bond yield expectations.

The Credit Market Transformation

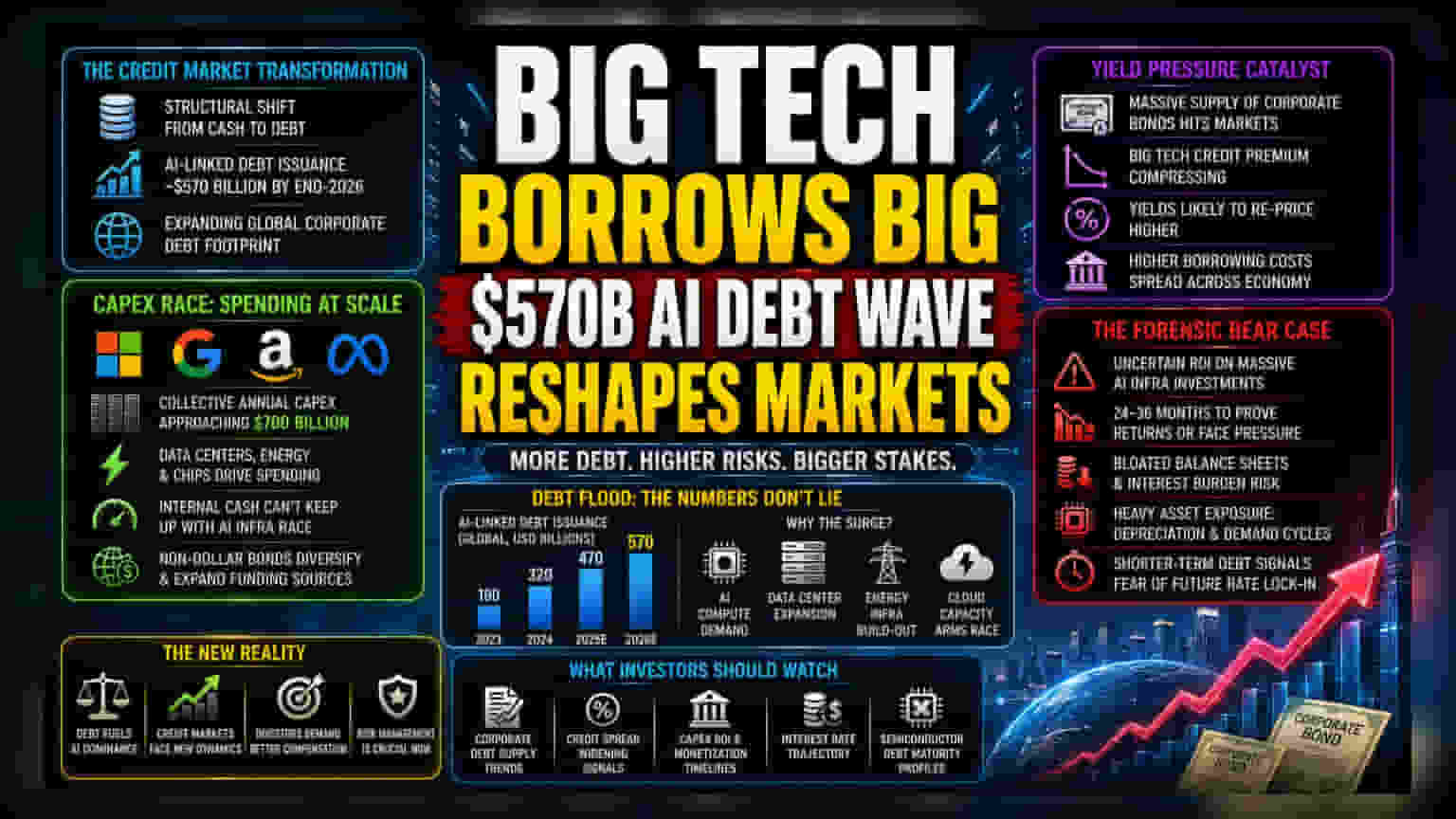

The structural foundation of corporate finance among mega-cap technology firms is undergoing a rapid metamorphosis. While these entities were historically characterized by heavy reliance on internal cash generation to fund operations, the sheer magnitude of the artificial intelligence infrastructure race has forced a pivot toward external leverage. This transition is not merely a tactical adjustment but a fundamental expansion of the global corporate debt footprint, with estimates positioning AI-linked issuance at approximately $570 billion by the end of 2026.

The Capital Expenditure Trap

Modern hyperscalers—most notably Microsoft, Alphabet, Amazon, and Meta—are engaged in a capital-intensive competition to secure dominant positioning in data center capacity, energy infrastructure, and advanced semiconductor procurement. Current projections suggest collective annual capital expenditures will approach $700 billion. This velocity of spending creates a distinct friction point within balance sheets; even firms with record-setting liquidity are finding that internal accruals cannot keep pace with the hyper-accelerated procurement cycles required to remain competitive in generative AI. By diversifying into non-dollar denominated bond offerings, these organizations are essentially betting that the long-term utility of this infrastructure will exceed the cost of servicing debt in an increasingly volatile interest rate environment.

The Yield Pressure Catalyst

The massive influx of new corporate bond supply is altering the technical dynamics of credit markets. As institutional investors digest this wave of paper, the historical premium associated with Big Tech debt is compressing. Market participants now face the reality that a sustained surge in issuance will likely force a recalibration of yields. When supply consistently outpaces historical demand profiles, the result is often a broadening of credit spreads, even for issuers with high investment-grade ratings. This shift effectively raises the floor for borrowing costs, not just for the tech giants themselves, but across the broader corporate sector as capital migrates toward the most aggressive AI-adjacent borrowers.

The Forensic Bear Case

From a risk-mitigation perspective, the current debt trajectory introduces significant margin compression potential. Skeptics point to the lack of clear, near-term monetization paths for the massive capital outlays being sunk into data centers and hardware. If the projected returns on these massive AI investments fail to materialize within the expected 24-to-36-month horizon, firms will be left with bloated balance sheets and significant interest obligations. Unlike the previous cycle of software-led growth, which required minimal physical infrastructure, the current regime demands heavy asset ownership, exposing companies to depreciation risks and cyclical downturns in hardware demand. Furthermore, the reliance on shorter-term debt instruments by some semiconductor players suggests an underlying fear of long-term lock-in at current interest rates, signaling a precarious mismatch between project life-cycles and financing windows.