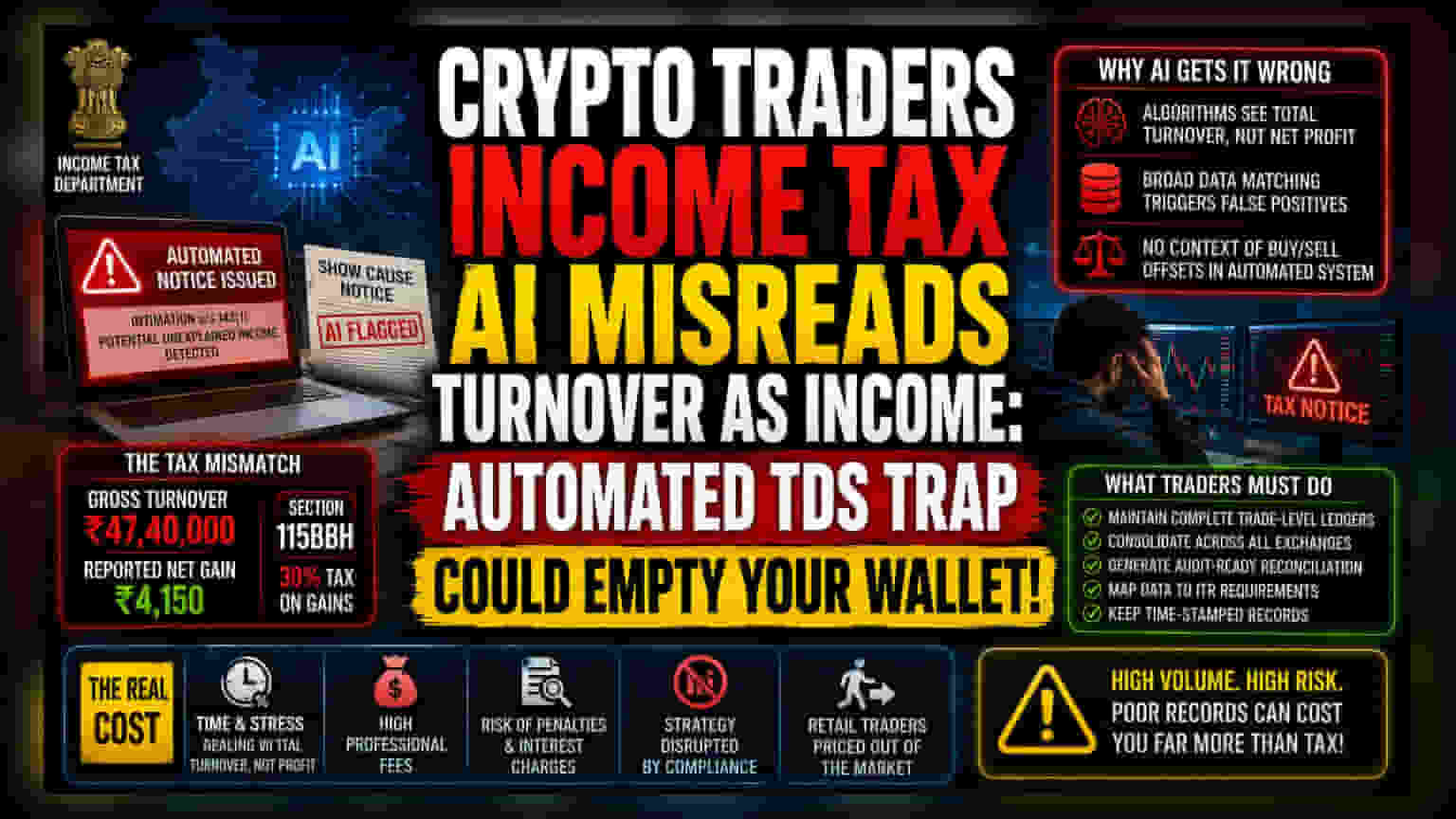

The Algorithmic Tax Mismatch

The automation of India’s tax infrastructure has created a hazardous environment for high-frequency digital asset traders. While the Income Tax Department leverages advanced data matching to capture tax evasion, these algorithms frequently misinterpret massive trading turnover as unexplained income. When an investor executes a high volume of trades, the aggregate transaction value reported by exchanges under Section 194S often dwarfs the actual net gain, creating a false-positive flag in the government’s automated compliance systems.

Systemic Friction in VDA Taxation

The fundamental disconnect lies in how Section 115BBH interacts with exchange reporting. Tax authorities view the 1% Tax Deducted at Source (TDS) as a marker of total activity rather than a simple entry point for profit assessment. In the recent Bengaluru case, the discrepancy was not a result of malfeasance but of data granularity. While the investor reported a net gain of approximately Rs 4,150, the tax portal observed Rs 47.40 lakh in gross turnover. Because the tax department’s AI-driven scrutiny relies on broad transaction summaries rather than individual trade ledger analysis, the system automatically generated a notice under the assumption that the gross turnover represented unreported revenue.

The Operational Risk for Traders

For active traders, the danger is administrative rather than fiscal. Compliance requires moving beyond simple profit and loss statements. Modern tax resolution requires a complete, audit-ready reconciliation of every buy and sell order executed across all platforms. Reliance on exchange-provided tax summaries is insufficient, as these documents often fail to map directly to the specific categories required by the Income Tax Return filing interface. Without a granular breakdown that isolates net profit from total turnover, traders remain exposed to show-cause notices that demand human intervention from jurisdictional Assessing Officers to rectify.

The Bear Case for Retail Participation

Regulatory complexity is effectively squeezing retail participants out of the digital asset market. The combination of a flat 30% tax on gains, the inability to set off losses against other income categories, and the heavy burden of manual proof during automated audits creates a significant barrier to entry. Unlike traditional equities, where brokers provide simplified consolidated tax statements that are generally accepted by revenue authorities, the fragmented and often opaque nature of exchange-based digital asset reporting increases the likelihood of errors. Investors who fail to maintain independent, time-stamped ledgers face high professional costs to defend their filings against automated scrutiny. The overhead required to remain compliant now represents a hidden tax on liquidity, potentially discouraging the high-frequency strategies that provide essential market depth.