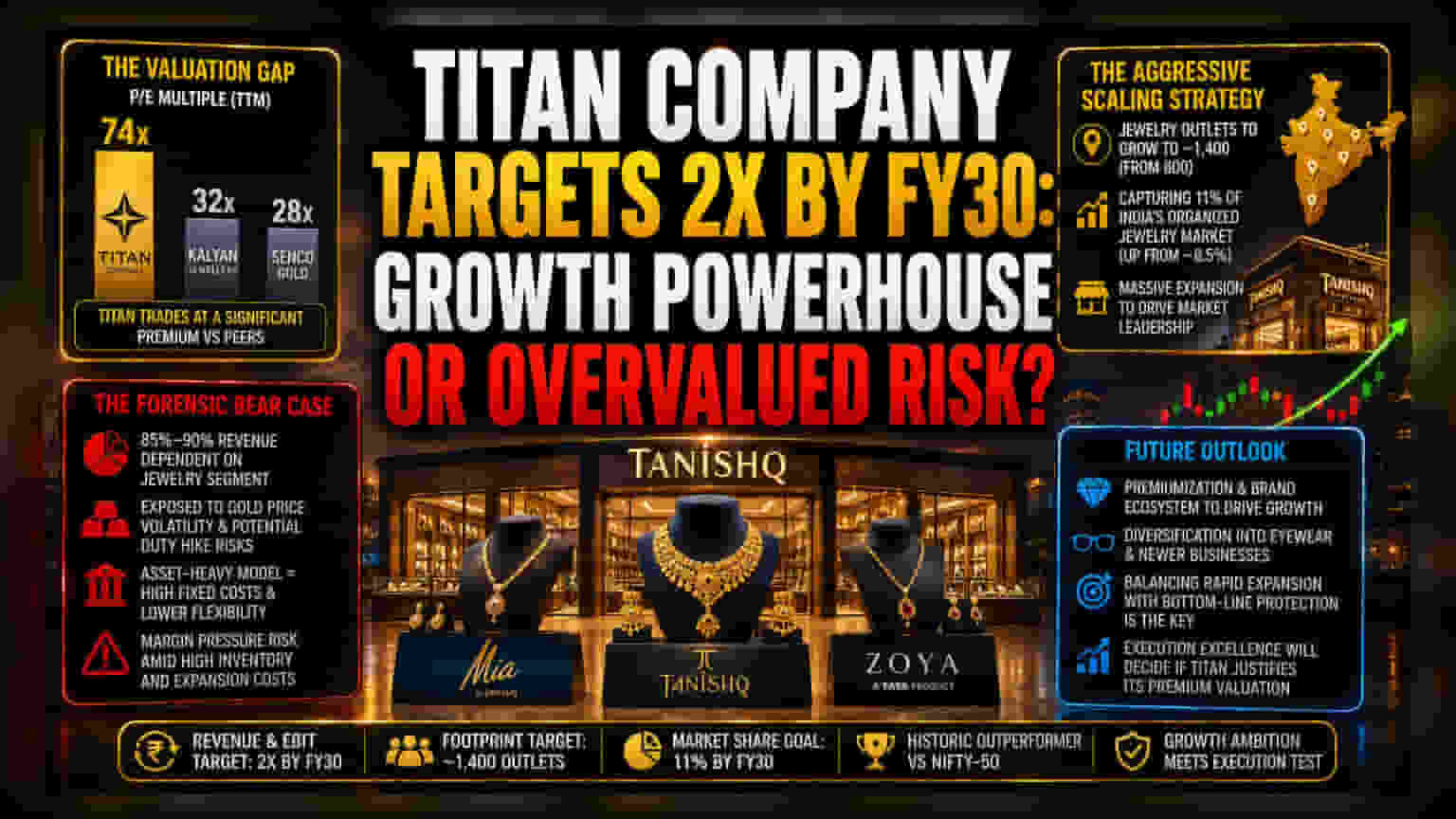

The Valuation Gap

Titan Company’s recent commitment to double its revenue and EBIT by FY30 has catalyzed a fresh wave of analyst optimism, reflected in the stock’s recent rally. However, the market’s pricing of this ambition is aggressive. Trading at a trailing price-to-earnings multiple of roughly 74x, the company commands a significant premium over peers like Kalyan Jewellers and Senco Gold, which typically trade at lower multiples. This valuation suggests that investors have already priced in near-perfect execution, leaving little margin for error if same-store sales growth faces any deceleration in the coming quarters.

The Aggressive Scaling Strategy

The core of the FY30 roadmap is a massive physical expansion, with plans to grow the jewelry network to approximately 1,400 outlets from the current base of 800. This strategy is designed to capture 11% of India’s organized jewelry market, up from the current ~8.5%. While the company’s ability to leverage the Tanishq, Mia, and Zoya brand ecosystem is well-documented, the sheer scale of the rollout introduces significant operational risk. Expanding the store footprint at this velocity requires massive capital allocation, effectively tying the company’s future to its ability to maintain high store-level profitability in an increasingly competitive environment.

The Forensic Bear Case

Despite the long-term compounding narrative, the business model carries inherent structural vulnerabilities. Titan remains heavily dependent on the jewelry segment, which contributes approximately 85% to 90% of its total revenue. This concentration creates acute exposure to macro-volatility, specifically the ongoing volatility in global gold prices and potential regulatory adjustments to import duties. Unlike competitors that may employ leaner, more capital-efficient retail models, Titan’s integrated, asset-heavy infrastructure creates high fixed costs. During periods of economic contraction or reduced discretionary spending, these assets can rapidly transition from competitive advantages into liabilities. Furthermore, the company’s margin resilience remains under scrutiny, as management navigates the challenge of maintaining double-digit EBIT margins while managing the high inventory costs associated with a broader physical footprint.

The Future Outlook

Brokerage consensus remains anchored by the company’s historical ability to outpace the NIFTY-50 following major strategic announcements. Analysts anticipate that the shift toward premiumization, combined with the integration of newer categories like eyewear and emerging businesses, will serve as necessary diversifiers. However, the path to FY30 will be marked by the company’s ability to balance rapid store additions with bottom-line protection. The ultimate test will be whether Titan can sustain its market-share gains without sacrificing the operational agility that defined its earlier phases of growth.