Mrs. Bectors Food Specialities crossed Rs 2,000 crore in revenue for FY26, but rising costs and intense competition hit profit margins, which fell to 6.9%. The stock has seen a significant correction since its 2024 peak as the company struggles to balance growth with profitability. Investors are now watching if the bakery maker can manage inflationary pressures and return to its 14% margin target.

What Happened

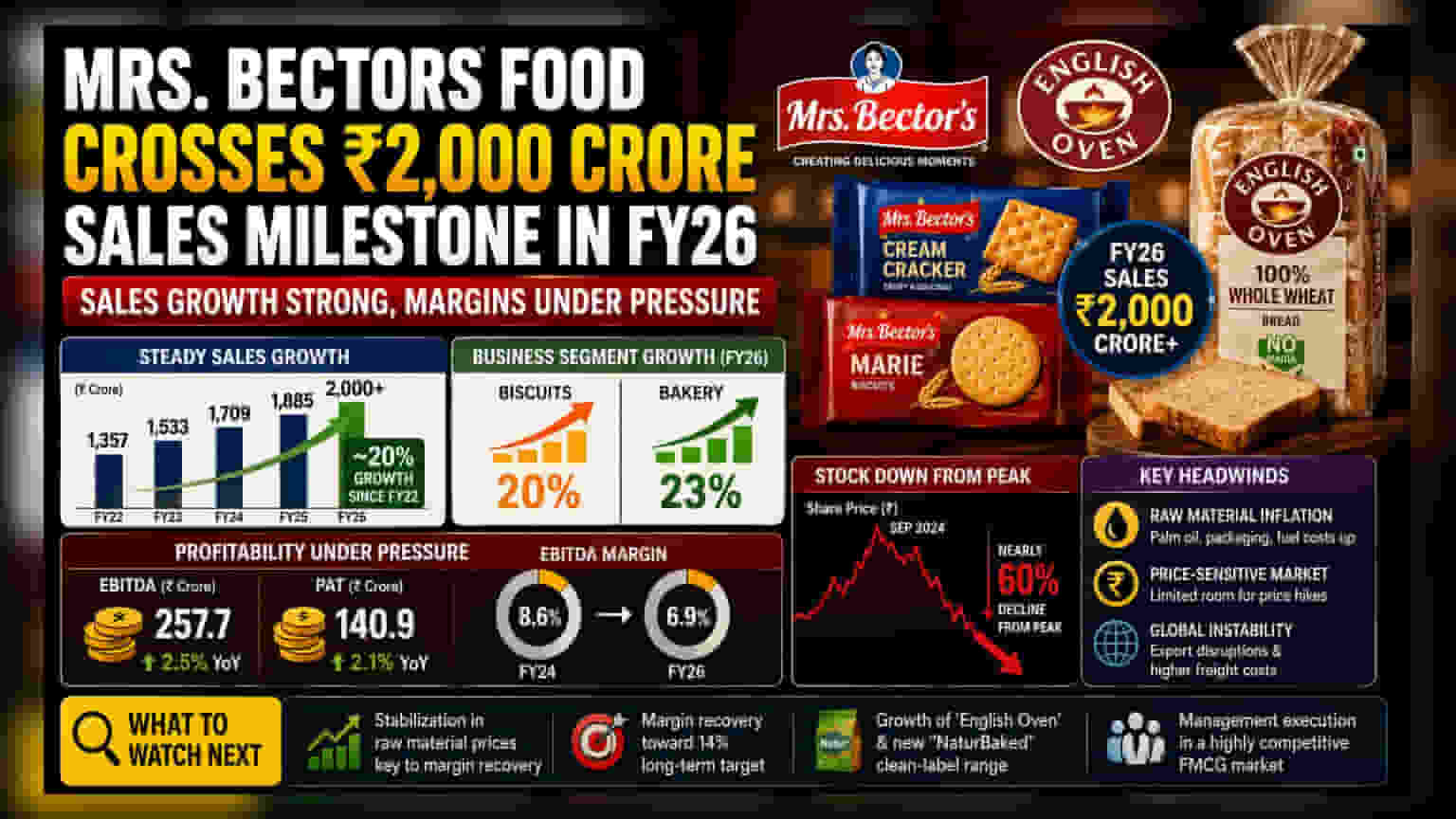

Mrs. Bectors Food Specialities, the company behind the Mrs. Bector's biscuit brand and the 'English Oven' bakery business, has reached a significant scale, crossing Rs 2,000 crore in annual sales in FY26. This reflects a steady growth of roughly 20% since FY22, with the biscuit segment growing at 20% and the bakery business expanding by 23%. However, while sales have grown, the company’s profitability has faced a noticeable decline, signaling a gap between business scale and earnings growth.

The Margin And Profit Picture

Despite the jump in revenue, the company's financial health shows signs of stress. EBITDA, which measures operational profit, reached Rs 257.7 crore in FY26, a modest increase of 2.5%. The profit after tax stood at Rs 140.9 crore, and importantly, margins dropped to 6.9%, down from 8.6% in FY24. In the competitive FMCG sector, such margin compression often happens when a company cannot pass on increased production costs to customers without risking a loss in volume. The company’s long-term goal of achieving a 14% margin has been delayed by these current financial pressures.

Why Investors Are Concerned

The stock market has reflected these challenges, with the share price declining by nearly 60% from its high in September 2024. For investors, the concern lies in the company's ability to maintain its profit margins while competing in a market dominated by large, well-entrenched players like Britannia, Parle, and ITC. When raw material costs rise, these larger players often have better bargaining power, making it difficult for smaller or specialized players to protect their bottom line.

Sector Headwinds And Risks

The business is dealing with a combination of difficult factors. First, raw material inflation, specifically in palm oil, packaging, and fuel, has pushed production costs higher. Second, the Indian biscuit market is extremely price-sensitive; any significant price hike can lead to a drop in sales as consumers switch to cheaper alternatives. Third, global geopolitical instability has disrupted exports, making international sales less predictable and more expensive due to higher freight costs. These external pressures have made it harder for the company to sustain the high growth rates seen in previous years.

What To Watch Next

While the 'English Oven' brand remains a strong growth engine and new initiatives like the 'NaturBaked' clean-label product line show promise, the immediate focus remains on profitability. Investors should track whether raw material prices stabilize, as this is the most critical factor for the company to improve its margins back toward its 14% target. Management’s ability to navigate competition while managing input costs will be the primary monitorable in upcoming quarters.