The Valuation Gap

Monika Alcobev has carved a unique niche in the Indian beverage sector by eschewing the traditional, capital-intensive distillery model in favor of an execution-heavy distribution strategy. By focusing on the import, marketing, and placement of over 100 premium global brands, the company has successfully bypassed the massive capex requirements typically associated with spirits manufacturing. However, the market’s reception since its July 2025 public debut has been tepid. With the stock trading significantly below its earlier highs, investors are clearly weighing the company’s scalability against the inherent risks of a trading-centric business.

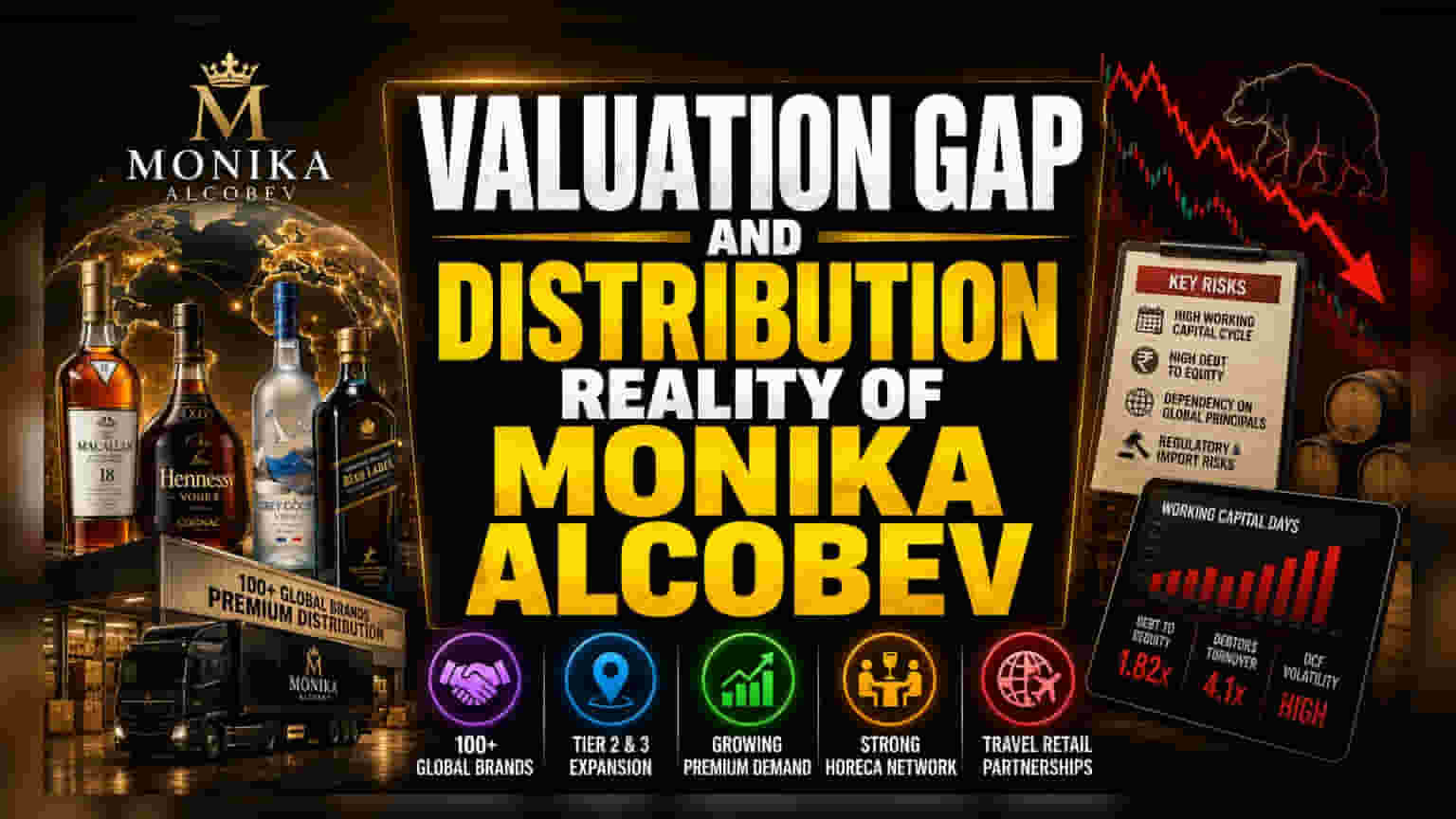

Execution Risks and Financial Realities

Unlike traditional manufacturers that control their production cycle, Monika Alcobev is tethered to the performance of its global principals. This dependency creates a structural vulnerability; the company does not own the underlying brand equity, meaning it is susceptible to contract renegotiations or principal shifts. Furthermore, the company’s financial health displays classic signs of a strained working capital cycle. Operating cash flows have shown volatility, and the firm faces a high debtor turnover ratio, a common challenge in the fragmented, high-regulation Indian liquor market. While the company claims to bridge the gap between global luxury and local demand, it must manage extended credit periods from state trading corporations, which can trap liquidity for up to a year.

The Forensic Bear Case

The bear case for Monika Alcobev centers on the sustainability of its 'behavioral land grab' strategy. While aggressively filling retail shelves and building HORECA relationships helped the company capture market share, this approach is essentially a race to control physical space. As competition in the premium imported liquor segment intensifies, the cost of maintaining this shelf visibility will likely exert significant pressure on profit margins. Additionally, the company’s reliance on debt to support its distribution infrastructure and inventory buffers poses a risk during economic downturns, particularly given its high Debt-to-Equity ratio. Any regulatory shift regarding import duties or state-level licensing could disproportionately impact a pure-play distributor compared to diversified, integrated distillers.

Future Outlook

Management remains focused on expansion into Tier-2 and Tier-3 cities, betting that rising discretionary income will continue to drive demand for premium spirits. The company has also begun to diversify its revenue streams through travel retail and embassy partnerships. However, analyst consensus suggests that long-term outperformance will require more than just distribution prowess; it will demand a shift toward higher-margin service offerings and the successful management of its rising working capital days. As the company prepares for its upcoming annual general meeting, shareholders will be looking for concrete signs of margin improvement and a reduction in the days of outstanding debt, which remain the primary indicators of operational health.