The Logistics-Driven Margin Shift

The transformation of the Indian cold coffee market is less about changing consumer taste profiles and more about the logistical efficiency provided by the rise of quick-commerce infrastructure. By reducing the friction between product availability and consumption, platforms such as Zepto and Flipkart Minutes have effectively eliminated the traditional 'summer-only' revenue curve that historically plagued the beverage industry. This reduction in demand volatility allows larger corporations to achieve better inventory management and lower storage costs. However, the reliance on these hyper-local delivery channels introduces a new layer of platform dependency that may eventually necessitate higher marketing spend to maintain visibility in a crowded digital feed.

Competitive Benchmarking and Institutional Positioning

While Nestle India continues to leverage its massive distribution network to push high-margin formats like Iced Roast, Hindustan Unilever is playing a defensive game by scaling its Bru brand to retain market share among price-sensitive consumers. Compared to the beverage industry's historical performance, the current trend shows a decoupling of coffee demand from ambient temperatures. This is a critical divergence from the industry's traditional seasonality, which analysts previously utilized to forecast quarterly revenue fluctuations. As Tier-2 city penetration accelerates, the competition is shifting from brand loyalty to shelf-space dominance in the digital warehouse.

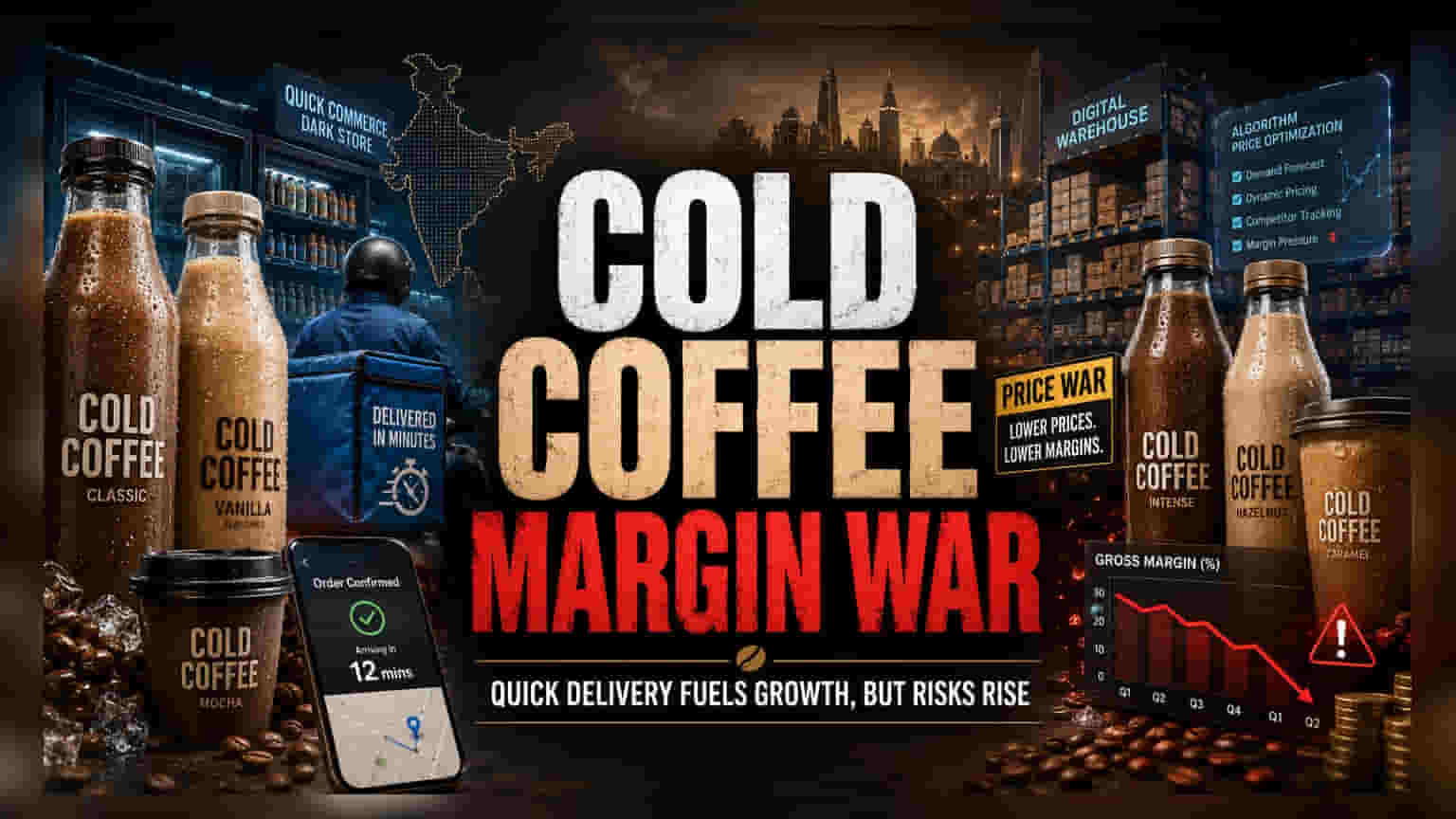

The Forensic Risk Assessment

The aggressive pursuit of this segment carries significant structural risks. Investors should scrutinize the potential for margin dilution as companies transition from established, high-margin hot coffee formats to the more competitive, operationally expensive ready-to-drink space. Furthermore, the reliance on quick-commerce platforms subjects these firms to the volatility of delivery commissions and the risk of sudden platform algorithm changes. There is also the threat of regulatory intervention regarding sugar content and high-caffeine marketing targeting younger demographics, a concern that has hampered similar beverage sectors in other emerging markets. Unlike established categories with steady demand curves, the current growth trajectory in cold coffee is heavily supported by the 'newness' of convenience, which may lack long-term retention if platform subsidies for quick delivery eventually decline.

Future Outlook and Sector Velocity

Industry consensus suggests that the normalization of year-round consumption will continue to attract smaller, agile competitors, potentially forcing larger incumbents into defensive price wars. The focus for investors will remain on whether these companies can sustain high double-digit volume growth without eroding their overall operating margins. As the category matures, the ability to maintain brand equity in an environment defined by rapid digital discovery will determine the long-term winners in this high-velocity space.