Godrej Consumer Products expects high-teen revenue growth for Q1FY27, supported by strong performance in India and Indonesia. While sales are climbing, rising raw material costs may impact profit margins despite recent price hikes in soaps and household insecticides.

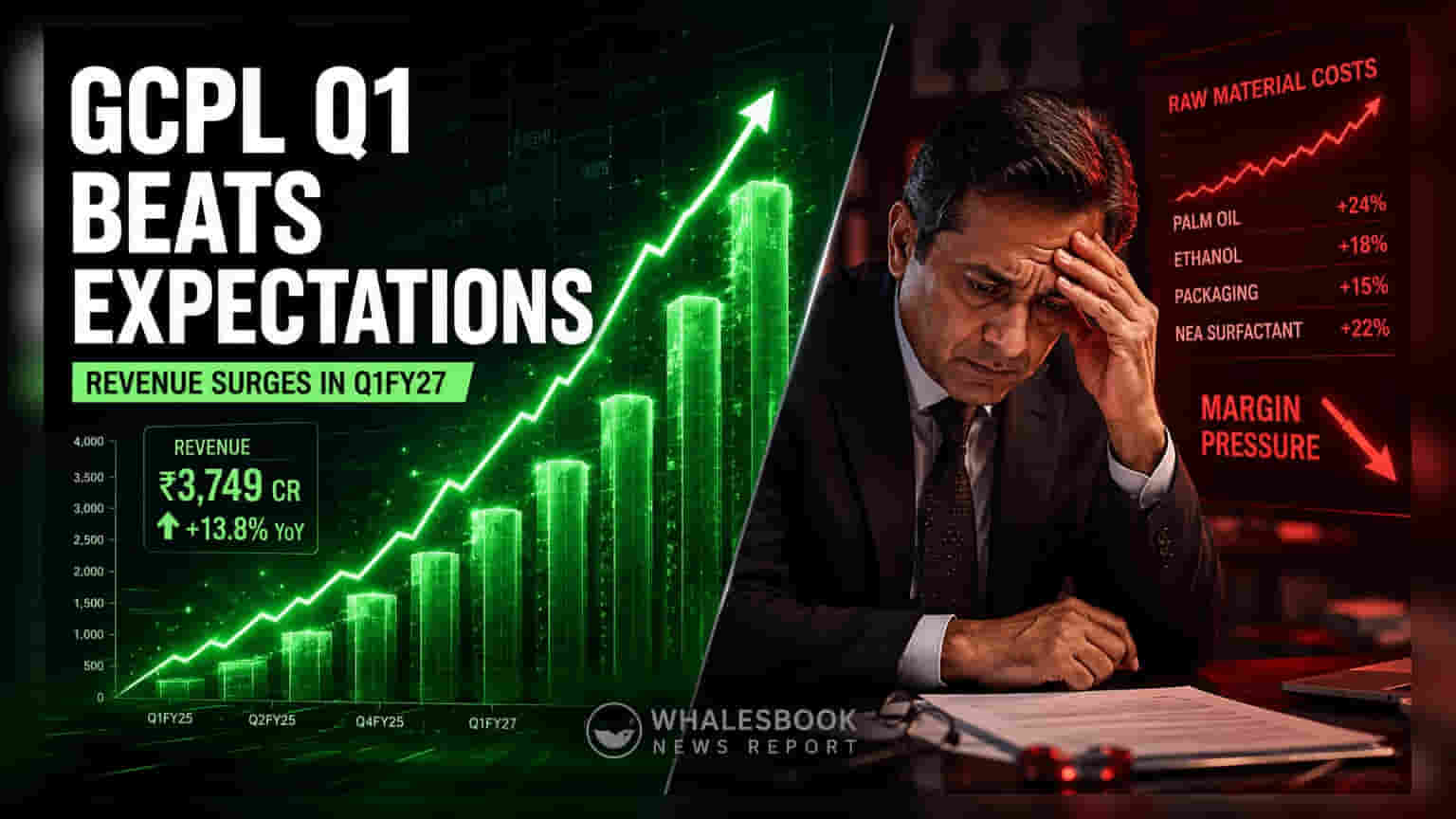

Godrej Consumer Products Limited (GCPL) has reported a strong start to the 2027 fiscal year, with performance across its domestic and international markets exceeding initial expectations. For the first quarter, the company is projected to see consolidated revenue grow in the high teens compared to the same period last year. This uptick follows an 11% growth rate recorded in the final quarter of the previous fiscal year.

Margin Pressures and Pricing Strategy

Despite the growth in sales, profit margins are expected to face pressure during the quarter. The company is dealing with an input cost inflation estimated between 6% and 9%, which is likely to cause a slight contraction in gross and operating margins. To combat these rising costs, GCPL implemented price adjustments at the start of the fiscal year. This includes a 5% price increase for soaps and household insecticides, and a 7% hike for detergents, resulting in an overall average price increase of 3% to 4% across its product portfolio.

Management is focusing on recovering these margins through a combination of targeted pricing actions, operational efficiencies, and adjustments to advertising and media spending. Investors will be monitoring these measures to see if the company can offset the impact of inflation on its bottom line.

International Market Performance

The company’s international operations have shown signs of a significant recovery. The Indonesian market, which contributes 12% to the company's consolidated sales, delivered mid-teen revenue growth, marking a recovery from the low single-digit growth seen in the previous quarter. This improvement was driven by double-digit volume growth and increased market share.

Similarly, the Godrej Africa, USA, and Middle East (GAUM) segment, responsible for 21% of total sales, reported strong results with high-teen volume growth. The segment also benefited from favorable currency movements, which are expected to contribute to a roughly 25% boost in reported sales growth for the region.

Investor Monitorables

The primary focus for investors in the coming quarters will be the company’s ability to sustain volume growth while managing the cost of raw materials. Key areas to track include the effectiveness of the recent price hikes, the stability of raw material prices, and the consistency of the recovery in international markets like Indonesia and Africa. Future financial disclosures will provide clarity on how much of the inflationary pressure the company has successfully absorbed and how its ongoing portfolio transformation in India is impacting overall profitability.