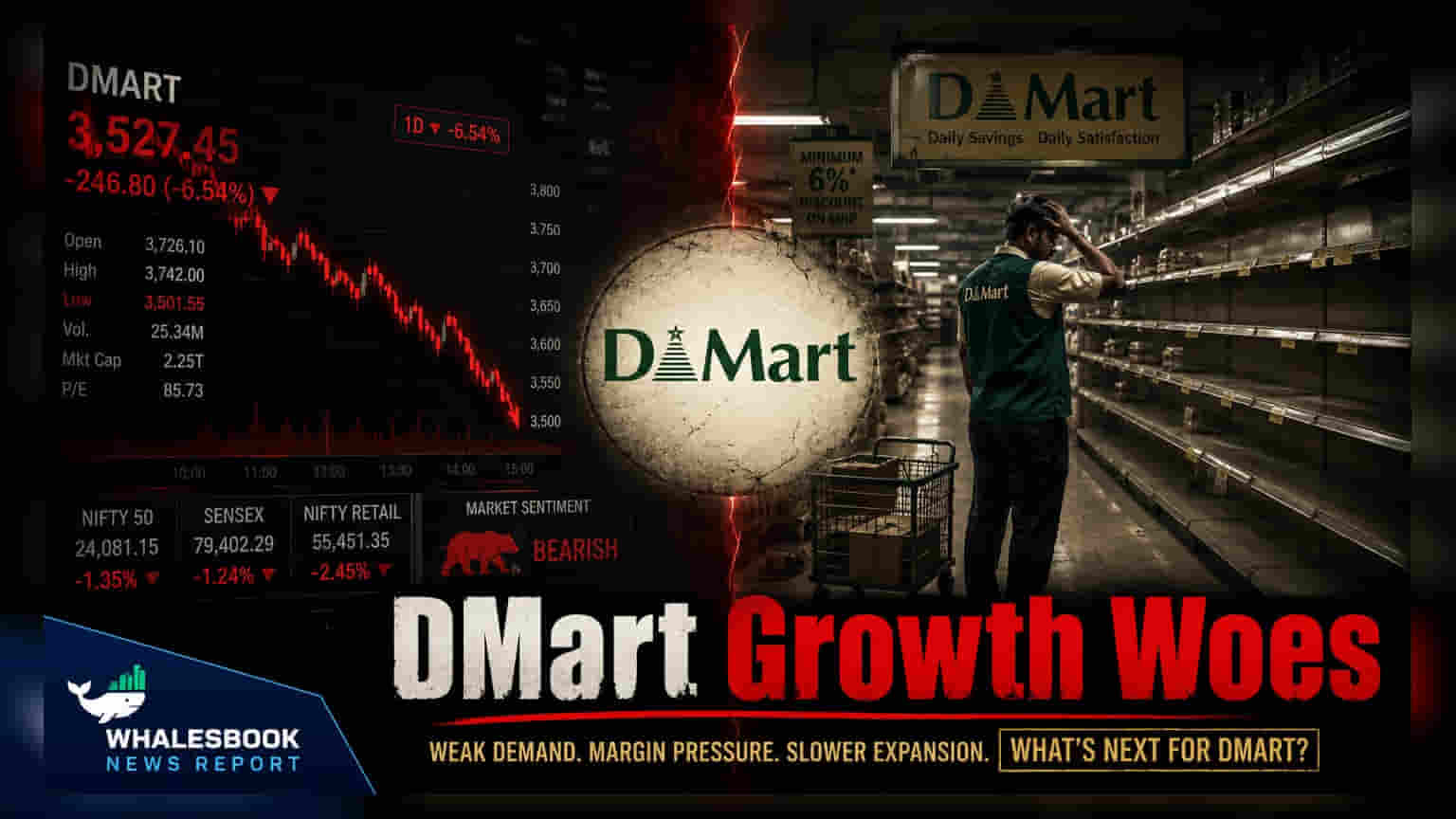

Avenue Supermarts (DMart) reported Q1 FY27 revenue of ₹18,300 crore, marking a slowdown in growth. The company added only three new stores, the lowest in twelve quarters, as quick commerce competition intensifies. Investors are now focused on same-store sales trends and margin stability amid rising operating costs.

What Happened

Avenue Supermarts, which operates the DMart retail chain, released its performance update for the first quarter of the 2027 financial year. The company reported revenue of ₹18,300 crore, reflecting a year-on-year growth rate of 15%. This figure is a deceleration from the 19% growth recorded in the previous quarter. Alongside the revenue numbers, the company's expansion pace has notably cooled, with only three net new stores added during the quarter. This is the lowest pace of store expansion the company has seen in three years, bringing the total store count to 503.

The Shift in Store Performance

Beyond the count of new stores, the underlying metrics suggest a change in demand patterns. Revenue per store saw a year-on-year decline of 3%. This is a significant shift, especially when compared to the aggressive expansion seen in the 2026 financial year, during which the company added 85 net new stores. The current trend in same-store sales—a metric that tracks revenue from older, established locations—has reportedly dipped into negative territory. This is a sharp contrast to the 10-11% growth in same-store sales recorded in the final quarter of the previous fiscal year.

Competitive Pressures

The retail landscape is currently being reshaped by the rapid growth of quick commerce and online grocery platforms. These digital competitors are increasingly targeting the metropolitan and Tier-I city segments where DMart has traditionally held a strong presence. Market observers suggest that the convenience provided by these platforms is impacting the footfall and spending patterns at physical retail outlets. While companies like V-Mart and V2 Retail have maintained their growth momentum, DMart's recent performance has sparked discussions regarding its potential loss of market share to these faster, digital-first alternatives.

Margin and Efficiency Outlook

DMart has historically maintained gross margins in the range of 14% to 14.5%. However, the company faces a two-fold pressure on its profitability. Firstly, intensified competition may force pricing adjustments that could squeeze gross margins. Secondly, operating expenses as a percentage of sales have shown a steady climb, rising from 5.8% in the 2024 financial year to 6.5% in the 2026 financial year. This rise in costs, combined with the deceleration in revenue, creates a risk that operating margins could come under pressure in the coming quarters.

What Investors Should Track

Investors will be looking for clarity on how the management plans to navigate the current competitive environment. Key monitorables include any updates on the scaling of the DMart Ready business and whether the company can stabilize its same-store sales growth. Furthermore, given the company's valuation—which has been historically high relative to its earnings—the market will likely focus on whether future quarterly reports show a recovery in store efficiency and a control on operating expenses.