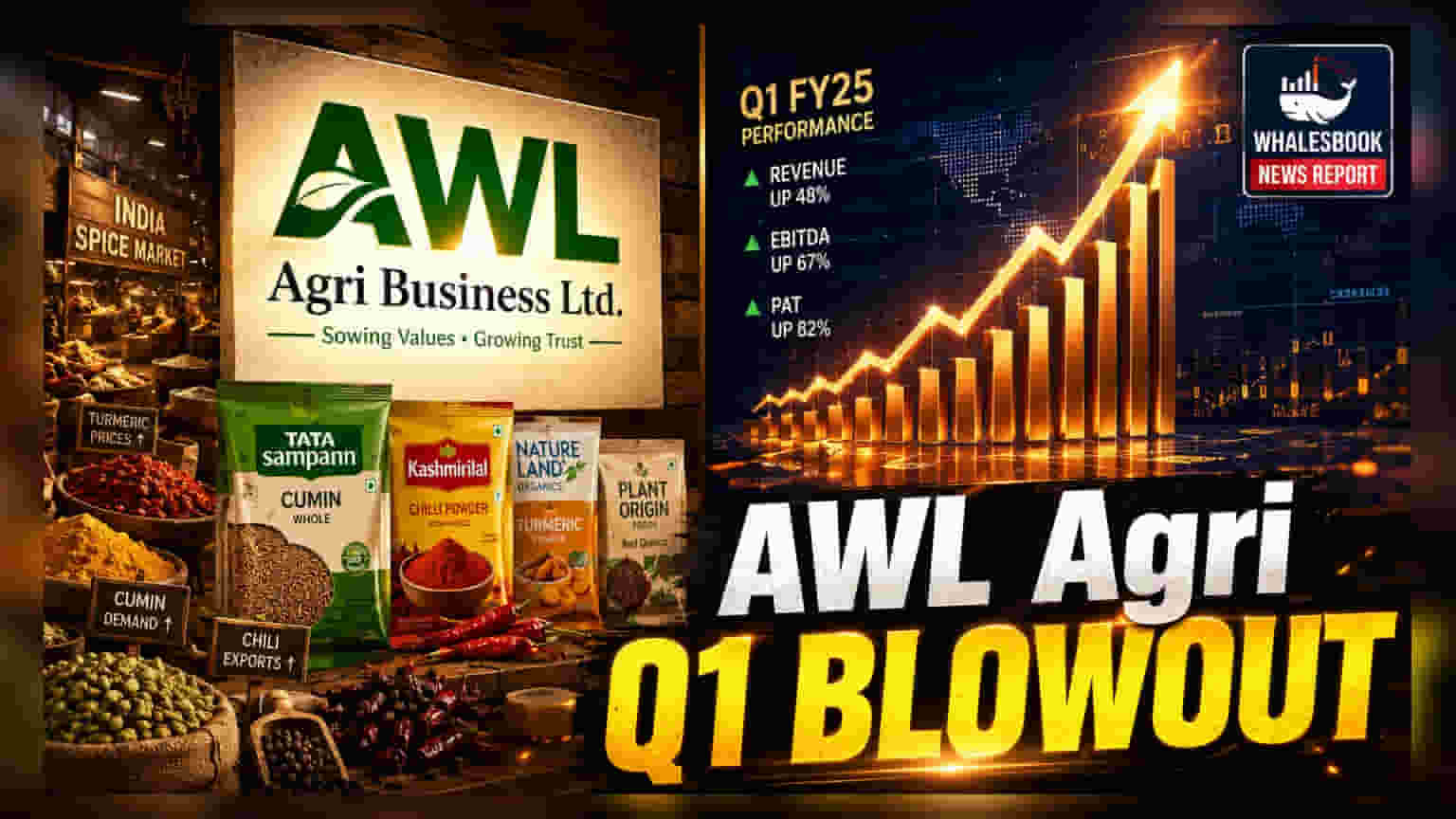

AWL Agri Business reported mid-single-digit overall volume growth for Q1 FY27. Performance was led by a 20% surge in the Food & FMCG segment, while the Industry Essentials division saw a 30% revenue increase. Investors may look for updates on raw material costs and volume stability in the edible oil business.

What Happened

AWL Agri Business Ltd has announced its financial results for the first quarter of the 2027 fiscal year. The company recorded mid-single-digit growth in total volumes. The standout performer was the Food & FMCG segment, which saw year-on-year revenue climb by more than 20%, supported by a 17% increase in volumes. Additionally, the company integrated the 'Madhur' brand via a new licensing agreement, aiming to expand its footprint in the consumer goods space.

Segment Performance Breakdown

The company’s Food & FMCG division saw significant demand, particularly in rice sales, which grew by over 40%. Other staples including pulses, sugar, besan, and personal care items collectively rose by 25% compared to the same period last year. Meanwhile, the Edible Oil business reported a 13% revenue increase, though volume growth was described as stable. The Industry Essentials segment proved to be a strong contributor as well, posting 14% volume growth and a 30% revenue boost, led primarily by demand for specialty chemicals and oleochemicals.

How Investors May Read This

Investors often look for volume growth as a sign of underlying demand, and the performance in the Food & FMCG segment suggests successful expansion in high-value categories. The stable volume growth in Edible Oils reflects a cautious approach to inventory, likely due to global supply chain and geopolitical factors. While the revenue figures appear strong, profitability will ultimately depend on how the company manages raw material costs, which can be volatile in the agriculture and edible oil space.

The Business Context

The strategy to move into higher-value products like specialty chemicals and personal care is a common trend for large food processing companies looking to diversify away from commodity-linked businesses. The licensing of the Madhur brand is another step toward this goal. For investors, the ability to maintain these margins while scaling the non-oil segments will be a key indicator of the company’s long-term business advantage.

What Investors Should Track

The primary monitorables for the coming quarters will be the volume trend in the Edible Oil business and the cost-to-income ratio in the Industry Essentials segment. Investors should also watch for management commentary regarding raw material price fluctuations, which frequently impact the profit margins of large-scale food and chemical companies. Furthermore, updates on the integration of the Madhur brand and its impact on overall profitability will be important for evaluating the success of this licensing strategy.