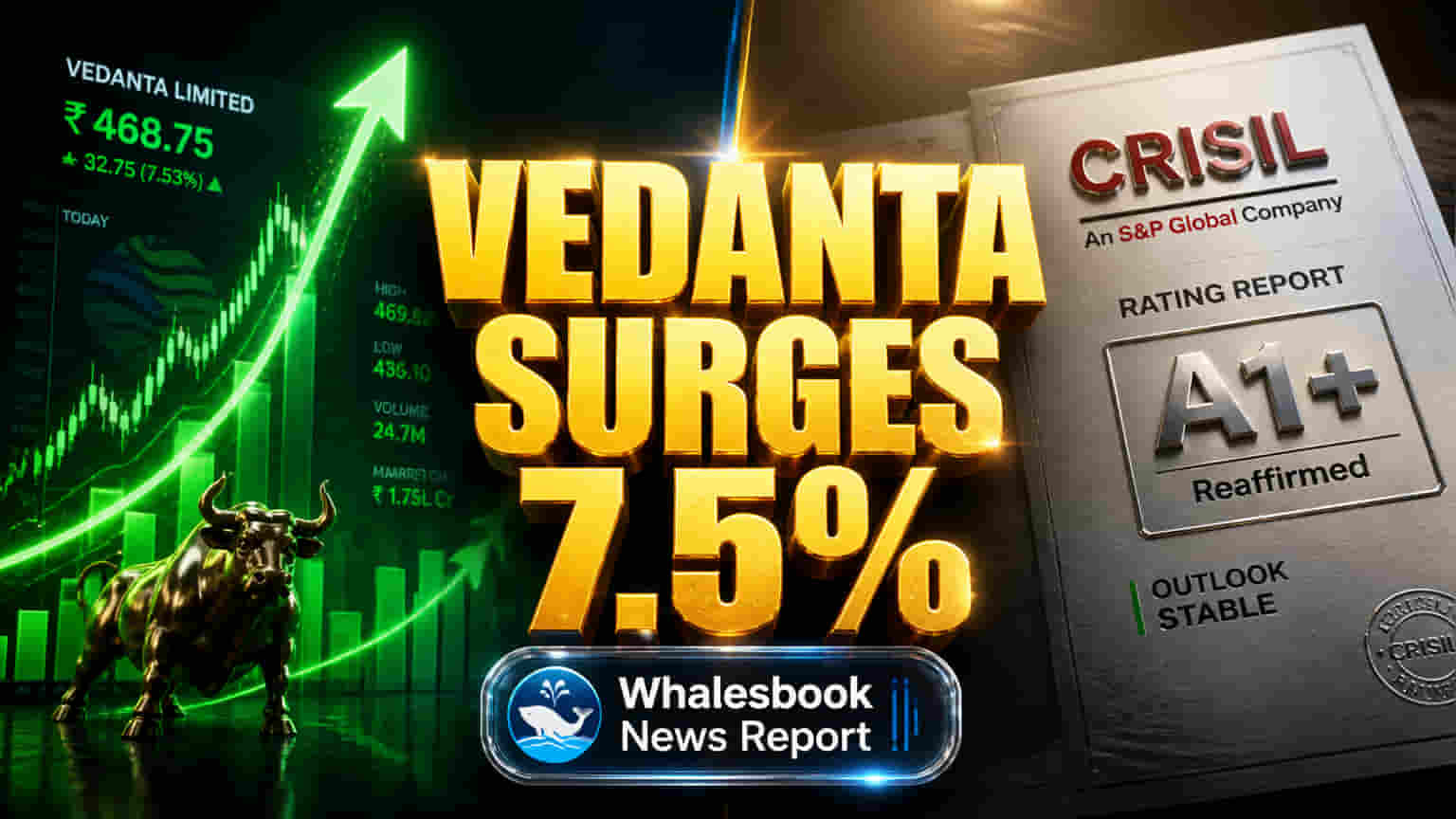

Vedanta Stock Rises on Rating News, FII Inflow

Vedanta Ltd saw a significant jump in its share price and trading activity on Monday, May 4, 2026. This was driven by CRISIL Ratings reaffirming the company's long-term credit rating at 'AA' with a 'Watch Developing' status, alongside a confirmation of its short-term rating at 'CRISIL A1+'. These ratings for certain non-convertible debentures offer some clarity amid Vedanta's major restructuring. However, the 'Watch Developing' status indicates the rating agency is closely monitoring the evolving financial setup after the demerger. Adding to positive sentiment, Foreign Institutional Investors (FIIs) increased their stake to 13.93% in the March 2026 quarter, up from 12.15% previously, suggesting renewed, though cautious, investor interest.

Vedanta's Demerger Plan: Five New Companies and Valuation

The company is undergoing a major demerger, a strategic move intended to unlock shareholder value by splitting its diverse businesses into five separate, independently listed companies: Vedanta Aluminium, Vedanta Oil & Gas, Vedanta Power, Vedanta Iron & Steel, and a residual holding company. This structure aims to unlock value by ending the conglomerate discount and allowing each business to be valued and funded independently. Vedanta's stock, trading around ₹290 on May 4, 2026, is worth about ₹1.13 lakh crore. Its Price-to-Earnings (P/E) ratio varies between reports, from about 6.7x to over 24.0x (TTM). This valuation looks competitive compared to peers like Hindalco Industries (P/E ~14.5x) and National Aluminium Co Ltd (P/E ~13.1x), and is undervalued versus Hindustan Zinc (P/E ~18.22x). The broader Indian metals and mining sector is currently recovering, thanks to strong domestic demand, higher infrastructure spending, and recovering commodity prices. Global events have also pushed up prices for commodities such as aluminum. India's strong standing as a global aluminum producer and government support for industry growth provide tailwinds. The sector is expected to grow about 7.84% annually from 2024 to 2028. Vedanta's stock had previously delivered strong returns, gaining significantly in the three years leading up to April 2026. However, its five- and ten-year returns have lagged broader market indexes. A sharp ~64% price drop on April 30, 2026, occurred as the stock traded ex-demerger, indicating the market is starting to value the remaining entity apart from the spun-off businesses.

Challenges Ahead: Debt, Execution Risks, and Rating Scrutiny

Despite the positive rating reaffirmation, the persistent 'Watch Developing' status from CRISIL highlights ongoing uncertainties about the demerger's financial impact. While transferring ₹6,089 crore in non-convertible debentures to Vedanta Aluminium Metal Ltd. is a key move, distributing significant group debt across five new companies creates complex execution challenges. Analyst price targets range widely from ₹480 to over ₹1000, reflecting uncertainty about the demerger's long-term success and how the market will value each new business. Vedanta's dividend yield is attractive at over 15%, but reports suggest a shift in its dividend policy away from a flexible 30% of profits. This change could affect its appeal to income investors. Past financial performance has been mixed, with promoter holding, for example, declining over the last three years. The 'Watch Developing' outlook from CRISIL, combined with the complexity of managing five distinct businesses and their debts, calls for caution. Initial market enthusiasm might overlook these structural challenges.

Analyst Views: Mixed Outlook Amid Demerger Uncertainty

Most market analysts maintain a 'Buy' rating for Vedanta, with average 12-month price targets around ₹860-877, indicating potential upside. Analysts like Kotak Securities expect clearer valuations and better capital allocation after the demerger. However, the wide range in price targets (₹480 to ₹1000) shows differing views on the demerger's outcome and the company's future. While the sector benefits from strong domestic demand and policy support, success hinges on executing the demerger smoothly, managing group debt across entities, and securing further positive rating developments. Investors should study each demerged entity separately as the market works to establish fair values for these new, focused businesses.