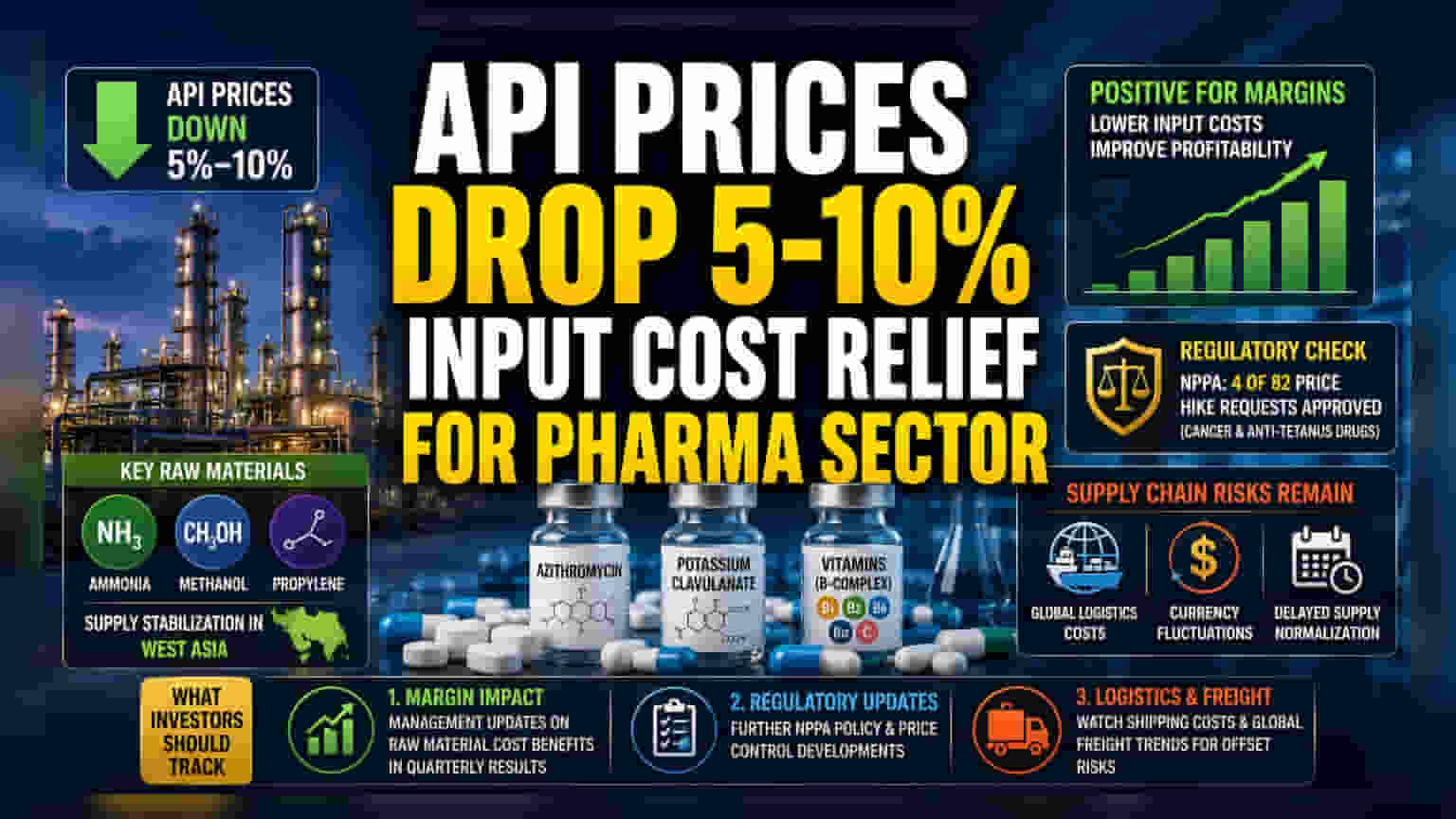

Active pharmaceutical ingredient (API) prices have slipped by 5-10% following easing geopolitical tensions in West Asia. This drop offers a potential boost to the gross margins of Indian drug manufacturers. However, with the National Pharmaceutical Pricing Authority (NPPA) maintaining strict control over drug price hikes, investors should watch whether these cost savings will improve profitability or if regulatory price caps will continue to limit margin flexibility.

What Happened

Active pharmaceutical ingredient (API) prices have dropped by 5% to 10%, providing a much-needed cooling effect on input costs for the Indian pharmaceutical sector. This decline is largely linked to the stabilization of geopolitical tensions in West Asia, a critical region for the supply of petrochemical-based raw materials like ammonia, methanol, and propylene, which are essential for drug manufacturing. Specific APIs, including azithromycin, potassium clavulanate, and several vitamin components, have seen a decline in price. Industry experts suggest that while this is a positive trend, the normalization of supply chains is a gradual process that could take several months.

Why This Matters For Investors

For Indian pharmaceutical companies, raw material costs are a significant component of their total expenses. When API prices rise, it typically squeezes gross margins, especially for manufacturers of generic drugs who operate in highly competitive markets with thin profit margins. A 5-10% reduction in these costs could theoretically improve profitability for companies that have been struggling with elevated input inflation over the recent periods. Investors generally look for expansion in gross margins as a sign of improved operational efficiency and a better ability to manage supply chain shocks.

The Regulatory Pricing Hurdle

While lower input costs are a positive development, the ability of pharma companies to benefit from them is tempered by regulatory oversight. The National Pharmaceutical Pricing Authority (NPPA) has recently shown a conservative stance toward allowing price increases for pharmaceutical products. Reports indicate that out of 82 applications from manufacturers seeking to raise prices, the regulator recommended approval for only four, primarily for specific cancer and anti-tetanus medications where supply shortages were critical. This indicates that even if input costs fall, the regulator continues to enforce strict pricing caps on essential medicines, which limits the ability of companies to adjust their pricing strategy dynamically.

Supply Chain And Execution Risks

Despite the easing of geopolitical tensions, the supply chain for APIs remains complex and interconnected. Relying on imports for key starting materials means companies are still exposed to global logistics costs, currency fluctuations, and potential delays in shipping and port handling. While the current price drop is a relief, it does not guarantee long-term stability. The industry is still navigating a period where full normalization is expected to be slow, meaning that temporary fluctuations in raw material availability could still occur in the coming quarters.

What Investors Should Track

Investors monitoring the sector should look for three key updates in the coming months. First, management commentary in upcoming quarterly results will be crucial to understand if the company is actually benefiting from these lower input costs or if previous high-cost inventory is still impacting margins. Second, keep an eye on any further communication or policy updates from the NPPA regarding price control measures, as this will determine the pricing power of companies. Finally, watch for any shifts in global logistics costs, as shipping and freight dynamics can quickly offset the gains made from cheaper raw materials.