Global oil refiners are reporting record profit margins as a sudden influx of crude supplies after the Strait of Hormuz reopening lowers costs. While fuel demand remains strong, analysts caution that these elevated margins may be temporary as crude prices normalize.

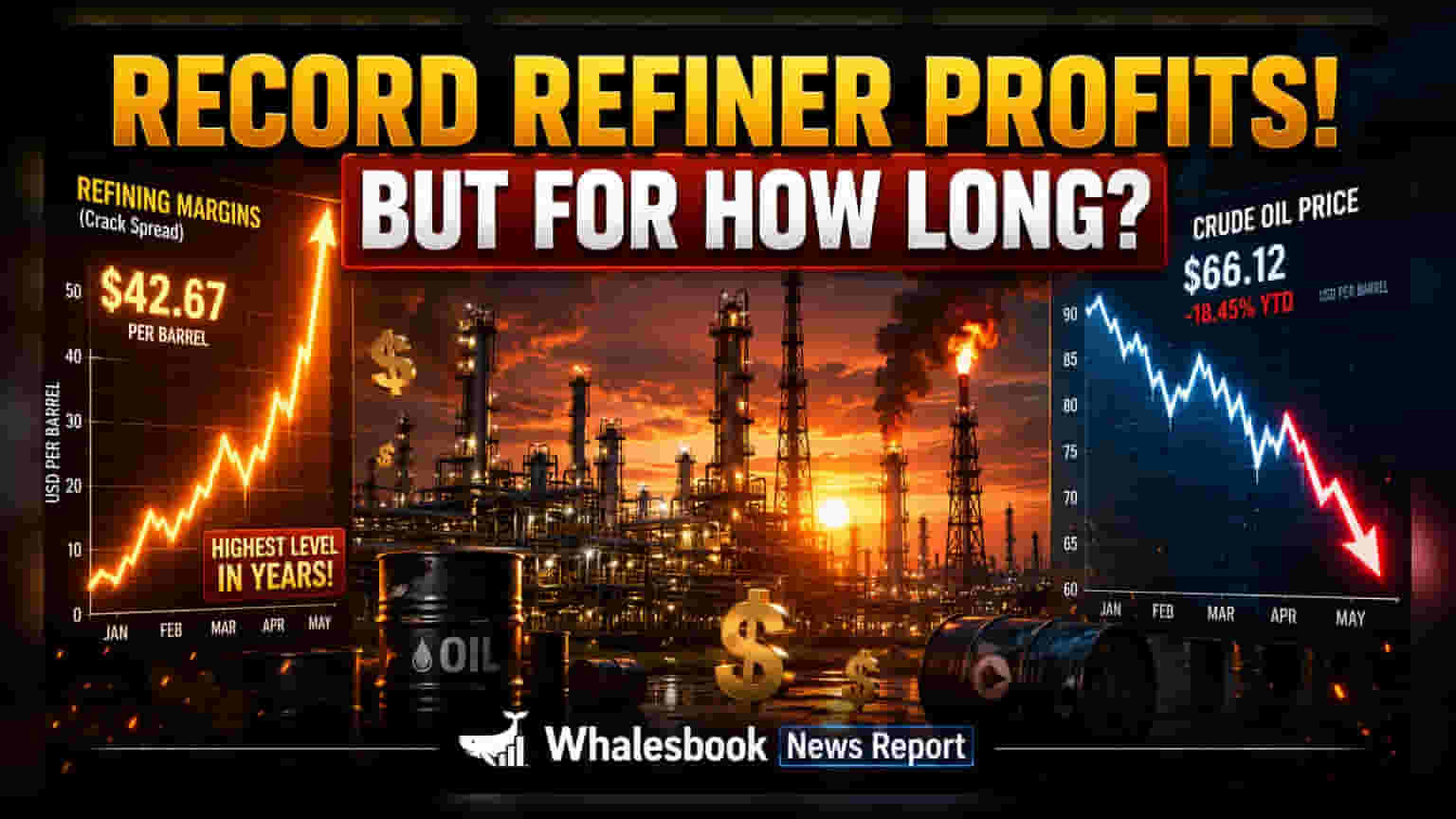

Oil refiners worldwide are currently benefiting from an unusual market environment that has pushed refining profits to historic highs. The primary driver is a dramatic shift in crude oil supply following the reopening of the Strait of Hormuz. As shipping routes normalized, a significant volume of oil that was previously held up has flooded the global market. Data indicates that Middle East crude exports climbed to 12.35 million barrels per day in June, a sharp increase from less than 8 million barrels per day in May. This influx has temporarily eased feedstock costs for refiners, with benchmark Brent crude futures hovering around $70 a barrel.

Impact of Refined Product Demand

While crude supply has increased, the market for refined products like gasoline and diesel remains tight. This imbalance has pushed the benchmark U.S. 3-2-1 crack spread—a key measure of refining profitability—past $60 a barrel. In the United States, gasoline refining margins have risen by over 60% since early June, reaching levels above $56 a barrel. This strength is partly due to low inventories heading into the peak summer driving season, a result of earlier supply chain disruptions during the regional conflict. Similarly, European diesel margins have stayed above $50 a barrel, supported by lower availability of Russian diesel following recent drone strikes on their refinery infrastructure.

Sustainability and Investor Risks

The current profit expansion is widely viewed by market observers as unsustainable. In a typical energy market cycle, high demand for refined fuels eventually pushes crude prices higher as refiners increase their intake of raw materials. Investors should note that the current wide gap between low crude costs and high fuel prices is likely to narrow. As the temporary supply glut from the Middle East is absorbed, crude prices are expected to rise, which would naturally put pressure on the exceptionally high refining margins currently being reported. The primary concern for shareholders is the potential for these margins to revert to historical averages once global supply and demand dynamics find a new equilibrium. Going forward, the most critical factors for investors to monitor include crude oil price movements, the pace of inventory replenishment for gasoline and diesel, and any changes in geopolitical stability that could affect export volumes from the Middle East.