The oil market is currently focused on immediate supply disruptions and the impact of geopolitical events. But beneath high prices, deeper changes in market structure and falling demand are starting to emerge, pointing to a future for oil values that is more complex than the current rally over scarcity suggests.

Supply Shock and Geopolitical Tensions Drive Prices

Brent crude settled near $108 per barrel on May 5, a substantial premium reflecting over 55% above pre-conflict levels, despite a technical pullback from its early April peak of $128. This pricing reflects the profound impact of the US-Iran conflict, which has effectively closed the Strait of Hormuz. Daily transits have collapsed from over 120 ships to just four on May 4, severely restricting a vital route for about 20 million barrels of oil daily. The International Energy Agency (IEA) has characterized this as the "largest supply shock in history." Major Gulf producers like Iraq, Saudi Arabia, Kuwait, the UAE, Qatar, and Bahrain collectively stopped an estimated 9.1 million barrels of crude in April, causing global supply to drop by 10.1 million barrels in March. Around 10-12 million barrels of crude from these Gulf producers are still stuck.

UAE Quits OPEC+, Weakening Coordination and Sparking Demand Worries

The UAE's exit from OPEC+ on May 1 is a major shift in market structure. Abu Dhabi, which historically held significant spare production capacity, has left. This weakens OPEC+'s ability to manage the market, potentially leading to more price swings and less support for prices. This, along with the ongoing conflict, suggests less coordinated supply management and could lead to more competition among producers. For Saudi Arabia, the UAE's departure means it's the main producer left to adjust output to stabilize prices, adding to its burden.

Falling demand is also becoming a real issue. The IEA has revised its 2026 global oil demand outlook from growth to a contraction of 80,000 b/d, with a severe Q2 contraction of 1.5 mb/d projected – the steepest since the COVID-19 pandemic. This drop in demand is most noticeable in Asia and the Middle East, impacting products like naphtha, LPG, and jet fuel. Global oil stockpiles have fallen significantly, leading Japan and other IEA members to release oil from strategic reserves. Supply limits are now more about where the oil is located and can get to, rather than just how much is in storage.

Russia has been an unintended beneficiary, with its March export revenue nearly doubling to approximately $19 billion. Urals crude prices rose sharply, narrowing the discount to Brent. India's imports of Russian crude surged 88% to 1.9 mb/d, and China's seaborne intake reached 1.8 mb/d. This surge in revenue shows how disrupted traditional supply routes are changing global trade patterns.

Demand Destruction Looms as Prices Stay High

The current high prices seem to focus more on immediate supply shortages than on the underlying demand for oil. While Brent crude has peaked near $128, the UAE's departure from OPEC+ suggests less coordinated supply management ahead, potentially leading to greater price swings. The ongoing closure of the Strait of Hormuz, while pushing prices up due to geopolitical risk, also signals that demand destruction could follow. History shows that long periods of high oil prices, even when caused by supply shocks, often lead to economic slowdowns and lower consumer demand. For instance, the 1973 oil shock led to a quadrupling of prices and a subsequent recession.

The current situation is already fueling inflation, with fertilizer prices up about 40% and rising inflation expected in developing economies. This inflation could push central banks to keep interest rates higher, which would slow economic growth and, in turn, reduce oil demand.

Outlook: Prices Could Climb, But Demand Could Stall

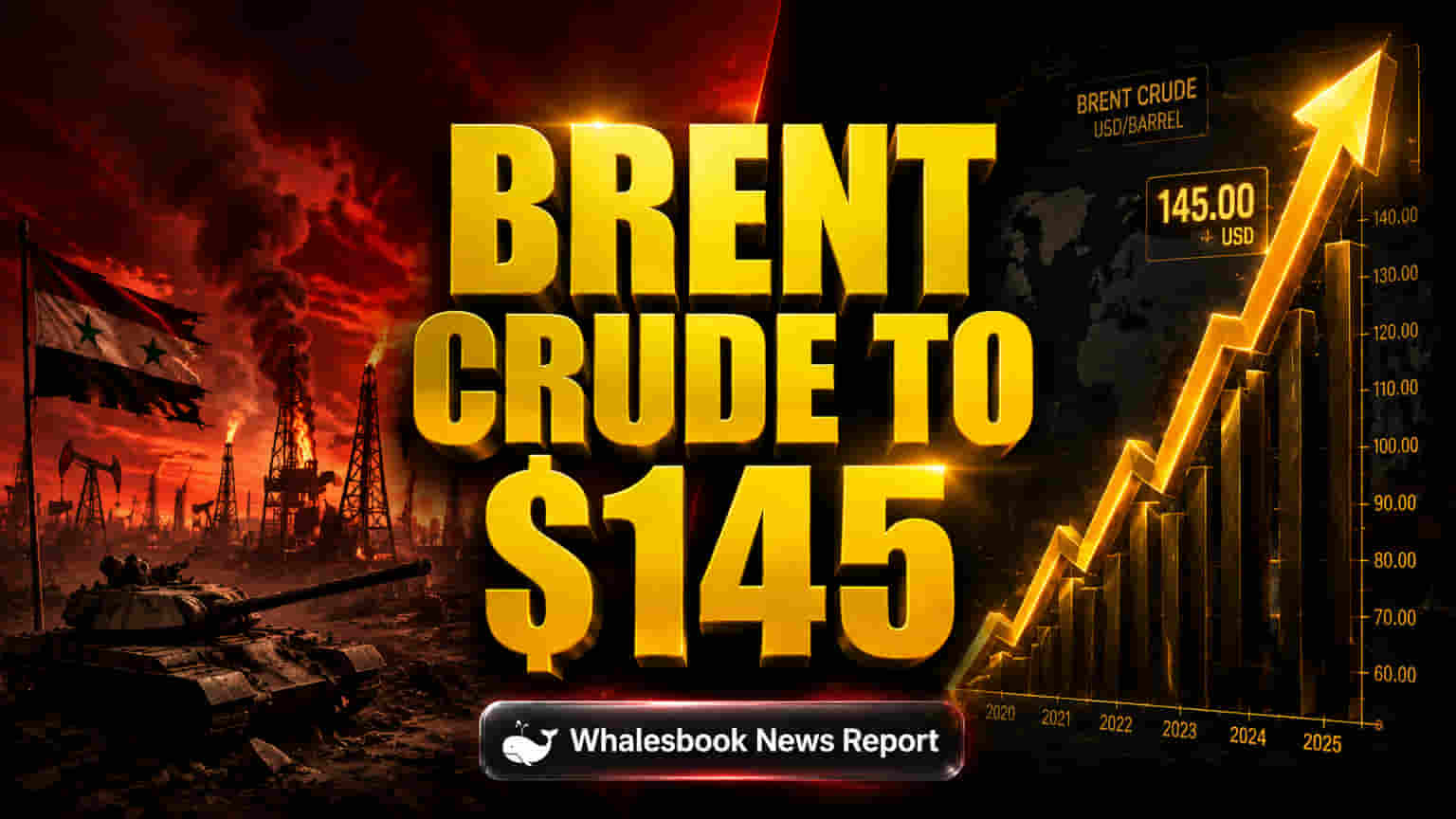

Analysts believe that if the conflict continues for another eight weeks without the Hormuz blockade being resolved, Brent prices could reach $130-$145 per barrel. However, the market is starting to focus more on how long supply will be disrupted rather than strong demand growth. The World Bank forecasts that if current trends persist, Brent prices could average $115 for the year, with potential risks pushing them as high as $150. The structural changes within OPEC+ and the growing signs of falling demand create a complex outlook, balancing immediate supply risks against factors that could lower prices in the medium term.