A new OECD-FAO report projects that food crops like maize and vegetable oils will remain the primary sources for global biofuel production through 2035. This reliance creates persistent competition between food supplies and fuel needs, particularly in emerging economies like India, where ethanol blending programs are shifting farmer preferences and potentially affecting domestic food price stability.

The latest agricultural outlook report from the OECD and FAO indicates that the global transition to advanced, non-food biofuel feedstocks is stalling. Despite long-standing discussions regarding sustainability, first-generation biofuels derived from common food crops such as maize, sugarcane, and vegetable oils are expected to maintain their dominant market position for the next decade.

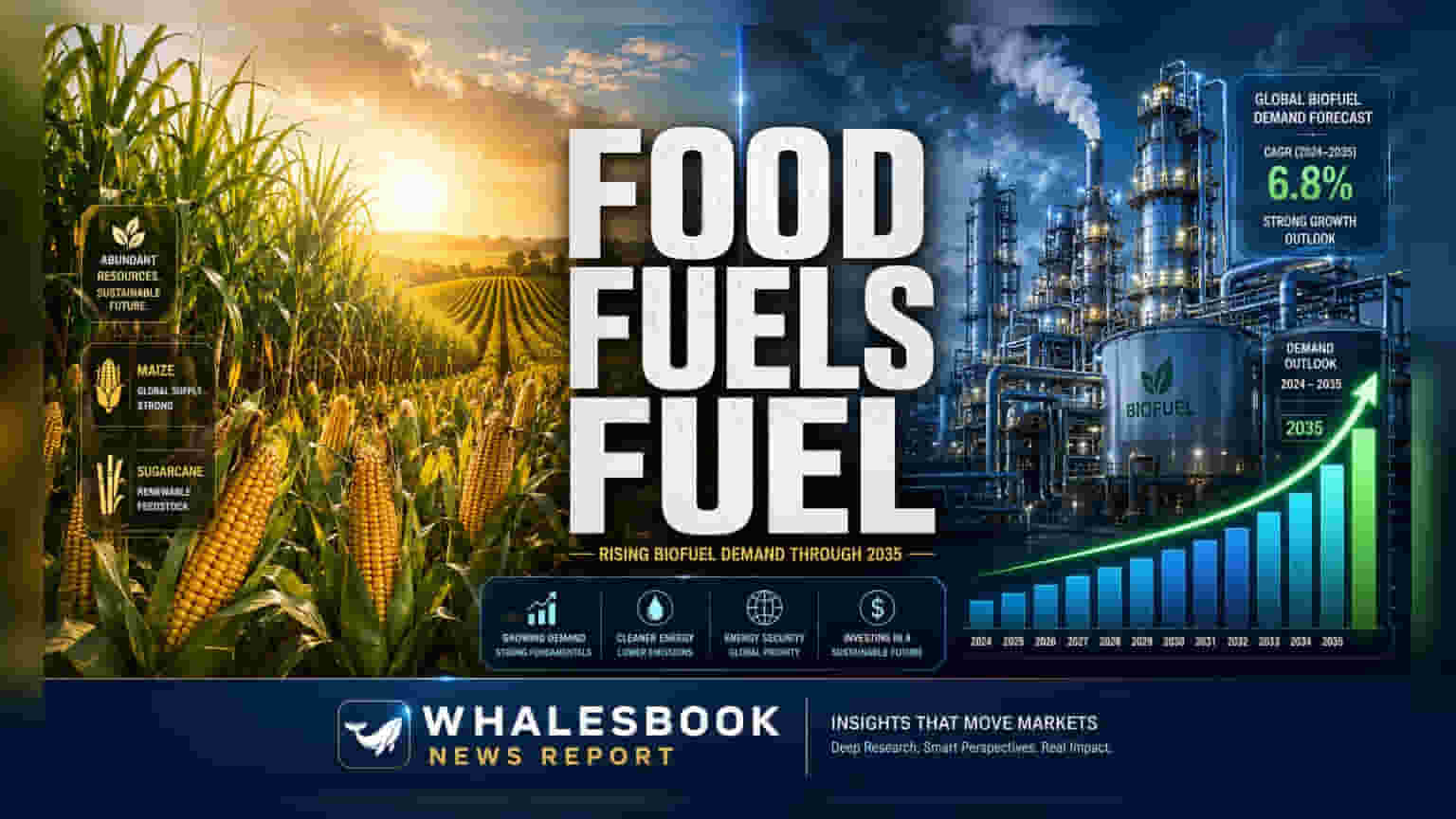

Impact on Global Agricultural Resources

The reliance on food-based feedstocks through 2035 means that the global agricultural system will face continued pressure to balance three competing demands: human food consumption, livestock feed, and industrial energy production. The report notes that second-generation biofuels, which use agricultural waste or non-food woody biomass, are not expected to gain significant market share in the coming years. This lack of diversification means that land and resources currently used for staple crops will remain tightly coupled with energy market requirements.

Challenges for India’s Ethanol Program

For Indian investors, the report carries specific local implications highlighted by recent government observations. The Economic Survey 2025-26 has previously expressed concern over the domestic ethanol blending program’s influence on cropping patterns. As demand for maize rises to meet ethanol production targets, there is a risk that farmers may shift away from cultivating essential commodities like pulses and oilseeds. Such a transition can have dual financial consequences: it may increase India's structural dependence on imports for edible oils and contribute to price volatility in the domestic food market.

Shifting Demand to Emerging Economies

While the overall growth rate for global biofuel production is expected to slow to 1.4% annually through 2035—roughly half the pace of the previous decade—the center of demand is shifting. High-income nations are seeing a decline in traditional fuel consumption, leading to a projected drop in their contribution to global biofuel growth from 40% to just 10%. Conversely, emerging economies, specifically India, Brazil, and Indonesia, are set to account for 80% of the future increase in global biofuel demand. This geographical shift places the responsibility for managing the food-versus-fuel trade-off directly on the policy and agricultural frameworks of these nations. Investors monitoring companies in the ethanol, sugar, and agricultural input sectors may watch for future shifts in government blending mandates and land-use policies, as these will be central to determining profitability and operational risks for firms tied to the biofuel supply chain.