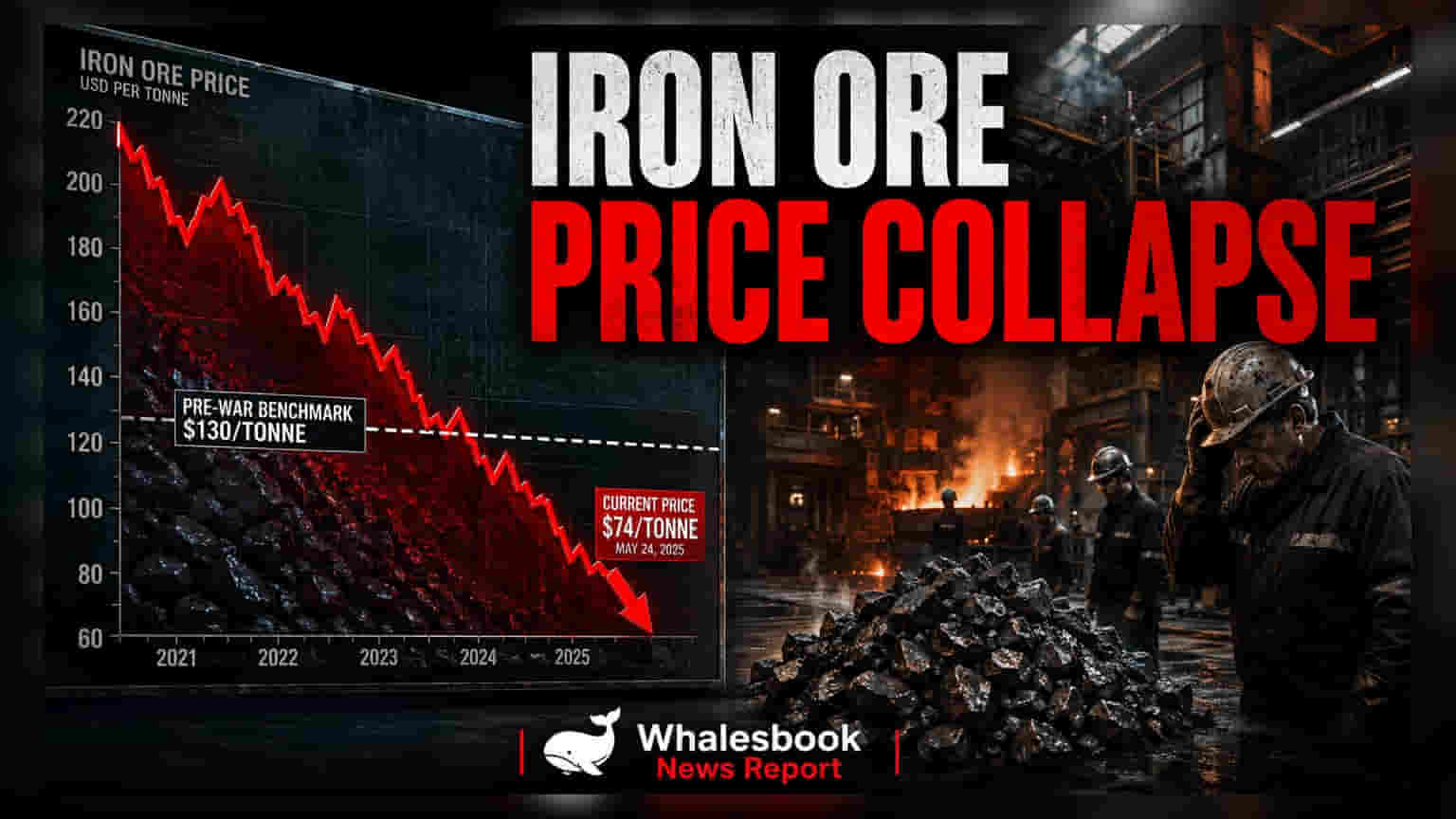

Iron ore prices have dropped to $98 per tonne, hitting levels not seen since early 2026. This decline reflects cooling global demand, particularly from China's struggling property market. For Indian investors, the trend creates a complex environment where lower raw material costs could lead to reduced steel prices and increased pressure from cheaper imports.

Iron ore prices have dropped to $98 per tonne for 62% steel content fines, falling back to levels seen before the commodity price surge earlier this year. This decline marks a sharp retreat from the peak of $111 per tonne reached during recent months of volatility. While prices often rise during times of global uncertainty, the current drop indicates that industrial demand factors are now weighing heavier on the market.

The primary driver behind this price shift is a slowdown in China, the world's largest steel producer and the biggest importer of iron ore. Data indicates that Chinese steel production fell by 3.7% in the first five months of 2026 compared to the same period last year. A lack of major stimulus measures, combined with a long-standing slump in China's property sector, has left the global market with excess supply and weak demand. Global iron ore production has also moderated, down 1.5% year-on-year, yet this has not been enough to balance the market given the sharp drop in consumption.

For Indian steel companies, the impact of falling iron ore prices is a double-edged sword. On one hand, cheaper iron ore can lower the cost of production for domestic steelmakers. However, history shows that steel prices typically follow raw material trends over time. If iron ore prices remain low, it often leads to a decline in finished steel prices, which can squeeze the profit margins of manufacturers.

Furthermore, the current environment poses a risk regarding global steel trade. With demand weak in major economies, there is an oversupply of steel circulating globally. India remains one of the few markets with robust internal consumption, making it an attractive destination for foreign steel. If global steel prices remain suppressed, Indian producers may face increased competition from cheaper imports. This dynamic has previously led domestic companies to request government policy support, such as import duties or trade protections, to shield local capacity from being undercut by lower-priced foreign steel.

Investors should monitor how Indian steel companies manage their inventory and pricing strategies in this environment. The next important indicators to track will be the quarterly financial results of major domestic producers to see if they can maintain their profit margins despite the softening commodity prices. Additionally, any updates on government trade policies related to steel imports will be a critical monitorable, as these could influence the competitive landscape for Indian steelmakers in the coming months.