India’s expenditure on crude oil imports surged nearly 70% to $35.5 billion in April-May 2026, as global prices stayed above $100 per barrel. This sharp increase, driven by geopolitical tensions, impacts the Indian Rupee, inflation risks, and the profit margins of Oil Marketing Companies (OMCs).

What Happened

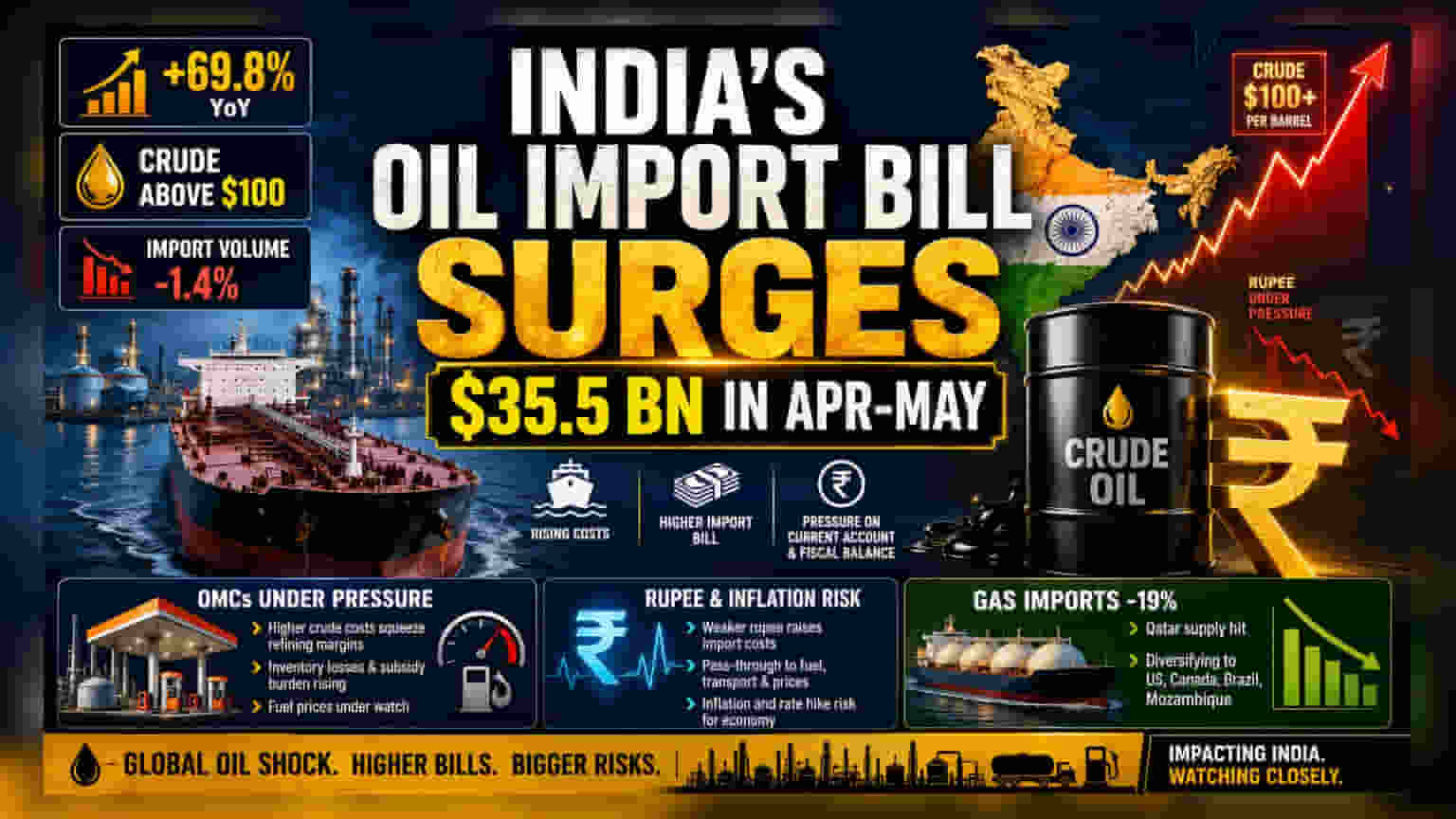

India’s import bill for crude oil rose significantly, reaching $35.5 billion for April-May 2026. This represents a 69.8% jump compared to $20.9 billion in the same period last year. According to data from the Petroleum Planning and Analysis Cell (PPAC), the surge is primarily due to global crude prices crossing the $100 per barrel mark. Interestingly, this spike in spending happened even as the physical volume of oil imports dipped by 1.4%, with shipments falling to 41.7 million tonnes from 42.3 million tonnes in the previous year. Geopolitical tensions in West Asia, particularly the conflict involving Iran and Iraq and the resulting supply route disruptions, have fueled this price volatility.

The Impact on the Indian Economy

For Indian investors, a rising oil import bill is a key economic indicator. India imports the vast majority of its oil requirements. When global crude prices rise, the country must spend more foreign currency (US Dollars) to buy the same amount of fuel. This puts downward pressure on the Indian Rupee, as demand for dollars increases to settle import bills. Furthermore, higher crude costs often feed into domestic inflation, as the cost of transporting goods and manufacturing increases, potentially impacting corporate margins across several sectors.

Pressure on Oil Marketing Companies (OMCs)

Public sector Oil Marketing Companies (OMCs) like Indian Oil Corporation (IOCL), Bharat Petroleum (BPCL), and Hindustan Petroleum (HPCL) are directly in the line of fire when crude prices remain elevated. These companies purchase crude oil at international market rates. If they are unable to pass on these higher costs to consumers through retail fuel price hikes, their marketing margins come under severe pressure. Investors typically watch the management commentary of these companies closely during periods of high oil volatility to understand how they plan to balance profitability and retail pricing.

The Natural Gas Supply Challenge

India’s energy import challenges have spread to natural gas, where imports declined by 19% in the first two months of the fiscal year. A critical factor here is damage to QatarEnergy's facilities at Ras Laffan, a hub that accounts for nearly 45% of India's natural gas imports. To manage this shortfall, government officials have stated that India is aggressively looking to diversify its procurement sources, focusing on the United States, Canada, Brazil, and Mozambique.

What Investors Should Track

Investors may monitor a few key factors in the coming months:

- Crude Oil Price Trends: Movements in the Brent crude benchmark directly correlate with the import bill and domestic inflationary pressure.

- OMC Profitability: Any updates or policy changes regarding retail fuel pricing that could provide relief to OMC marketing margins.

- Currency Movement: The stability of the Indian Rupee against the US Dollar, which acts as a proxy for the balance of trade and oil import costs.

- Energy Supply Diversification: Progress on securing natural gas from new international suppliers, which will determine the stability of gas-based industrial sectors.