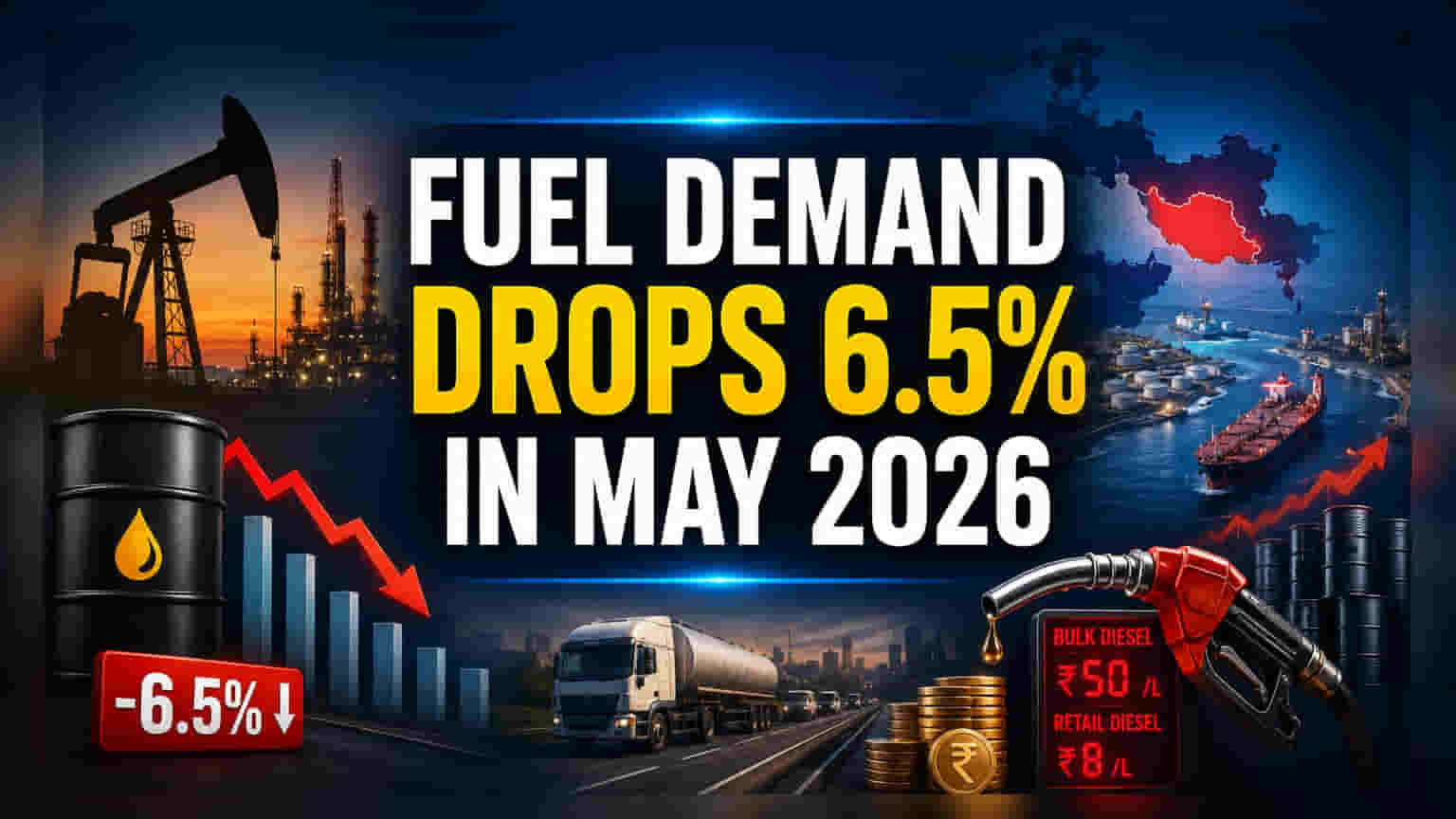

India's refined fuel consumption fell by 6.5% in May 2026, as supply chain disruptions tied to the Iran conflict raised costs. The decline in key fuels like bitumen and naphtha signals potential weakness in road construction and industrial activity, which investors are monitoring closely.

What Happened

India's refined fuel consumption saw a notable decline in May 2026, dropping 6.5% compared to the same period last year. Total consumption for the month reached 19.93 million metric tonnes. Industry data indicates that the primary driver for this slowdown is the ongoing conflict in Iran, which has disrupted global supply chains and caused a spike in energy product prices. This has created a difficult environment for fuel users, leading to a shift in how energy products are consumed across the country.

Impact Across Key Sectors

The drop in fuel demand is not limited to transportation but has spread across various industrial sectors. Consumption of naphtha fell by 29%, and bitumen usage declined by 39.4%. Because bitumen is a critical material for road construction, this sharp decline suggests a potential deceleration in ongoing infrastructure projects. Similarly, the 11.3% drop in petcoke and the 20.5% decrease in LPG consumption point to tepid industrial activity. While transport fuels like petrol and diesel saw muted growth of 3.3% and 1.5% respectively, the overall data reflects a broader cooling in economic indicators.

Price Pressures and Changing Demand

Supply chain constraints near the Strait of Hormuz have made it difficult to import certain fuels, forcing domestic refineries to adjust their production mix. To combat shortages, refineries have increased their LPG output. This adjustment has meant that less naphtha is being produced, further impacting industries that rely on it. A significant gap has also emerged between bulk diesel and retail diesel prices—bulk diesel users are currently paying roughly Rs 50 per litre, compared to around Rs 8 per litre for retail consumers. This price disparity has discouraged bulk buyers, leading them to either scale back operations or seek cheaper alternatives like fuel oil, which saw a 24% spike in demand during May.

How Investors May Read This

For investors, this news highlights two key areas of concern: economic health and the operational environment for Oil Marketing Companies (OMCs) such as Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum. The weak demand growth in core industrial fuels suggests that the economy may be facing a period of slower activity. For the OMCs, the ability to manage margins while dealing with distorted product demand and higher supply costs will be critical. The shift in sales from private retailers to state-run refiners also suggests that pricing strategies in the retail market are heavily influencing where consumers buy their fuel.

What Investors Should Track

Going forward, investors may want to track several key factors to understand the durability of this trend. First, the stability of supply routes through the Strait of Hormuz remains a primary variable that could influence import costs and availability. Second, watch for any narrowing of the gap between bulk and retail diesel prices, as this will determine if industrial consumption stabilizes. Finally, monitoring upcoming infrastructure project reports will provide clarity on whether the drop in bitumen consumption is a short-term blip or a signal of a prolonged slowdown in road construction.