The Valuation Gap

The sector currently stands at an inflection point where top-line growth is decoupled from organic demand volume. While the industry expects revenue acceleration, the reliance on passing cost increases to end-users is becoming increasingly precarious. Investors should note that while cables often comprise a marginal percentage of total project costs—rarely exceeding 5%—this historical immunity to inflation is being tested by sustained volatility in LME-traded copper and aluminum markets. The current market pricing appears to be baking in optimistic margin preservation, yet historical data suggests that as capacity additions hit the market, the ability to maintain these price premiums will likely diminish.

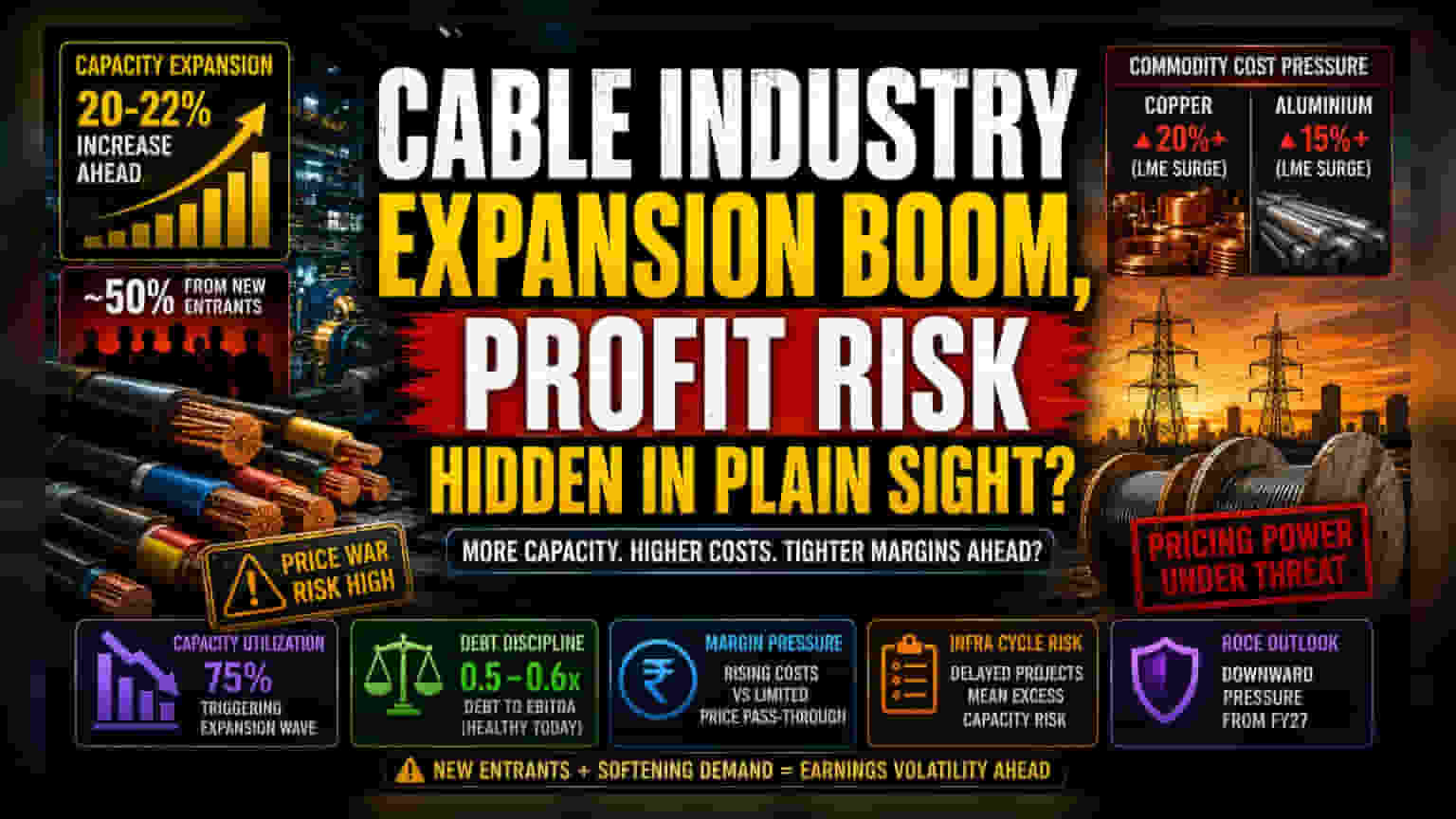

The Competitive Shift and Capacity Risk

Industry capacity utilization hovering at 75% has acted as a catalyst for a massive, sector-wide expansion push. However, the concentration of this growth among new entrants is the silent variable that analysts are underestimating. With roughly 50% of the projected 20-22% capacity increase arriving from firms lacking the legacy brand equity of market leaders, the stage is set for a price war. Unlike the stable environment of the previous decade, the current influx of capital-intensive production facilities means that fixed-cost absorption will become more difficult if infrastructure project timelines face even moderate delays. The reliance on internal accruals and equity to fund this expansion is a prudent move for balance sheet health, keeping debt-to-EBITDA ratios in the 0.5-0.6 range, yet it leaves companies with less cushion should cash flows turn negative due to a sudden downturn in real estate absorption.

The Forensic Bear Case

The primary risk lies in the structural sustainability of current pricing power. The assumption that customers will continue to absorb commodity-linked price hikes is predicated on a high-inflation, high-growth environment. Should the government’s infrastructure spending cycle face fiscal constraints or bureaucratic bottlenecks, the cable sector will be left with excess capacity and severely limited pricing leverage. Furthermore, the reliance on global PVC supplies—which have already seen double-digit price increases—introduces a geopolitical sensitivity that many local players have failed to hedge adequately. Historical performance metrics show that during previous cycles of heavy commodity inflation, companies that failed to consolidate their market share quickly were forced into deep discounting, leading to a permanent impairment of operating margins that lasted several quarters beyond the initial commodity price drop.

The Future Outlook

Brokerage consensus remains cautious regarding mid-term profitability, with many firms signaling a shift from growth-at-any-cost to margin-focused metrics. The industry's ability to maintain a debt-to-EBITDA ratio below 0.6 is positive, but the return on capital employed (ROCE) will likely face downward pressure as the new capacity comes online in fiscal 2027. Investors are monitoring the interplay between private equity-backed entrants and listed incumbents, as the former is likely to prioritize market share over short-term profitability, creating an unpredictable headwind for sector-wide earnings stability.