The Geopolitical Supply Shift

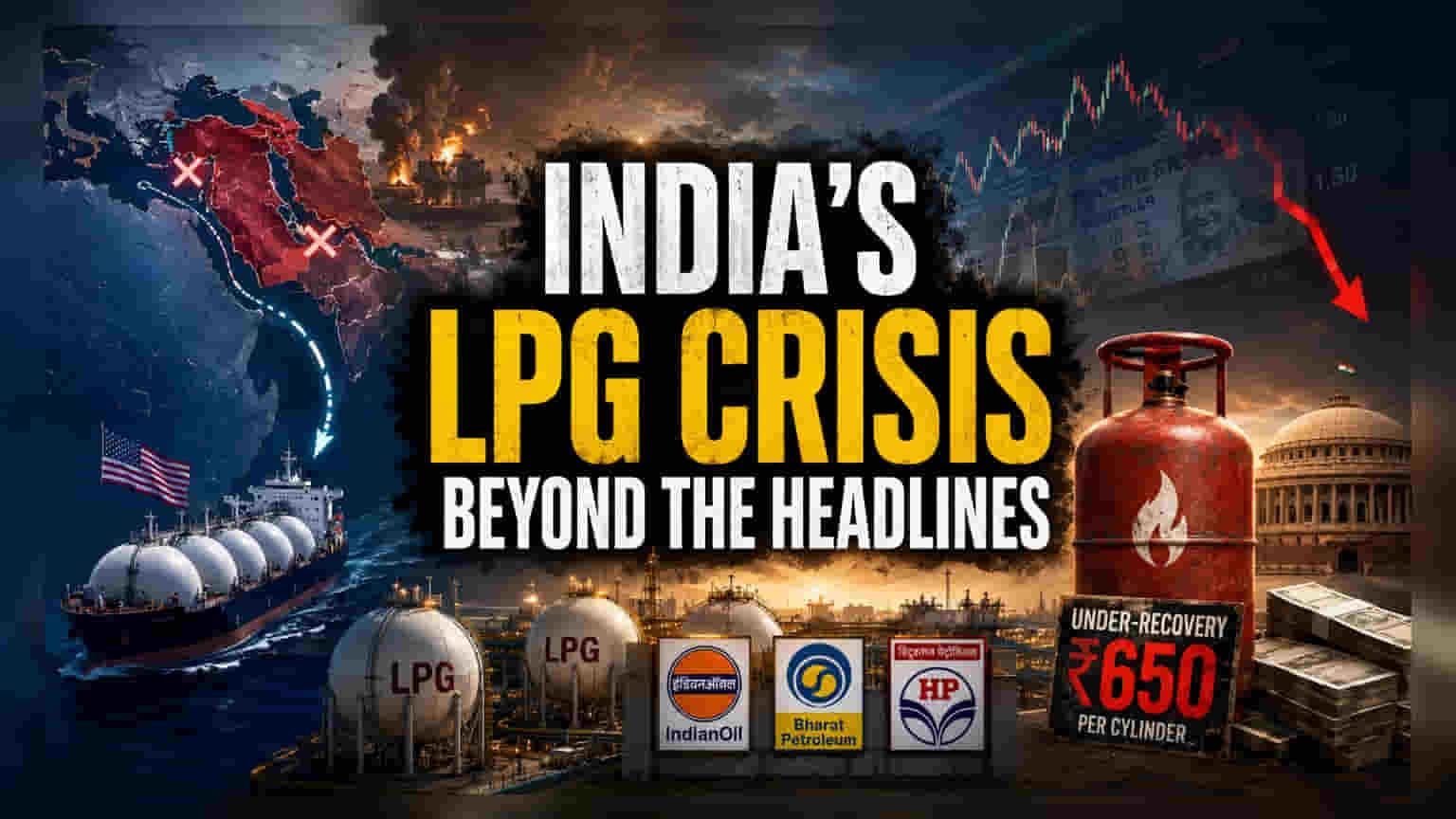

India’s energy import architecture is undergoing a forced, rapid recalibration. Following the de facto closure of the Strait of Hormuz due to escalating conflict, traditional Gulf suppliers—long the bedrock of India’s energy security—have seen their market share collapse. Shipments from Qatar plummeted 77.7%, while Saudi Arabia recorded a 75.5% decline. In a desperate bid to maintain base-load supply for its 330 million active LPG consumers, India has redirected its sourcing toward the Atlantic Basin, resulting in a 73% surge in U.S. LPG arrivals. This geographic pivot, while necessary for short-term survival, introduces significant logistical complexity and higher landed costs that the domestic market is currently struggling to absorb.

The Margin Compression Trap

While the import shift has bolstered physical inventory levels, the financial health of state-run oil marketing companies (OMCs)—Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum—remains under extreme duress. These retailers are currently incurring an under-recovery of approximately ₹650 per domestic LPG cylinder. This disconnect between global market volatility and stagnant retail pricing, despite recent hikes in auto fuel, has created a structural profitability gap. With Brent crude consistently hovering above $100 per barrel and freight rates for Very Large Gas Carriers (VLGCs) inflating long-haul costs, OMCs are effectively subsidizing national energy stability at the expense of their quarterly earnings and balance sheet liquidity.

Structural Demand Contraction

Beyond supply-side constraints, the domestic consumption landscape is shifting. Provisional data reveals a 19.2% year-on-year decline in LPG demand for May, the sharpest contraction among major petroleum products. This demand destruction is multifaceted; while government-mandated booking restrictions and supply management measures have played a role, there is growing evidence of affordability stress among low-income households, compounded by an ongoing transition in urban areas toward induction and piped natural gas. The decline suggests that for many, LPG is becoming a discretionary expense rather than a guaranteed utility.

The Risk of Institutional Erosion

Despite record domestic production reaching 52,000 tonnes per day, the concentration of supply risk remains a primary threat. Government mandates to build a 30-day reserve capacity represent a massive working capital commitment for OMCs already reeling from elevated procurement costs. Should geopolitical tensions persist and crude prices maintain their current trajectory, the reliance on US spot-market cargoes will continue to expose Indian retailers to extreme price swings. Unlike private competitors who can adjust commercial pricing more fluidly, the public sector entities remain tethered to political price-setting, risking significant erosion of their book value if federal compensation mechanisms fail to keep pace with the daily under-recovery losses currently exceeding ₹550 crore across all fuels.