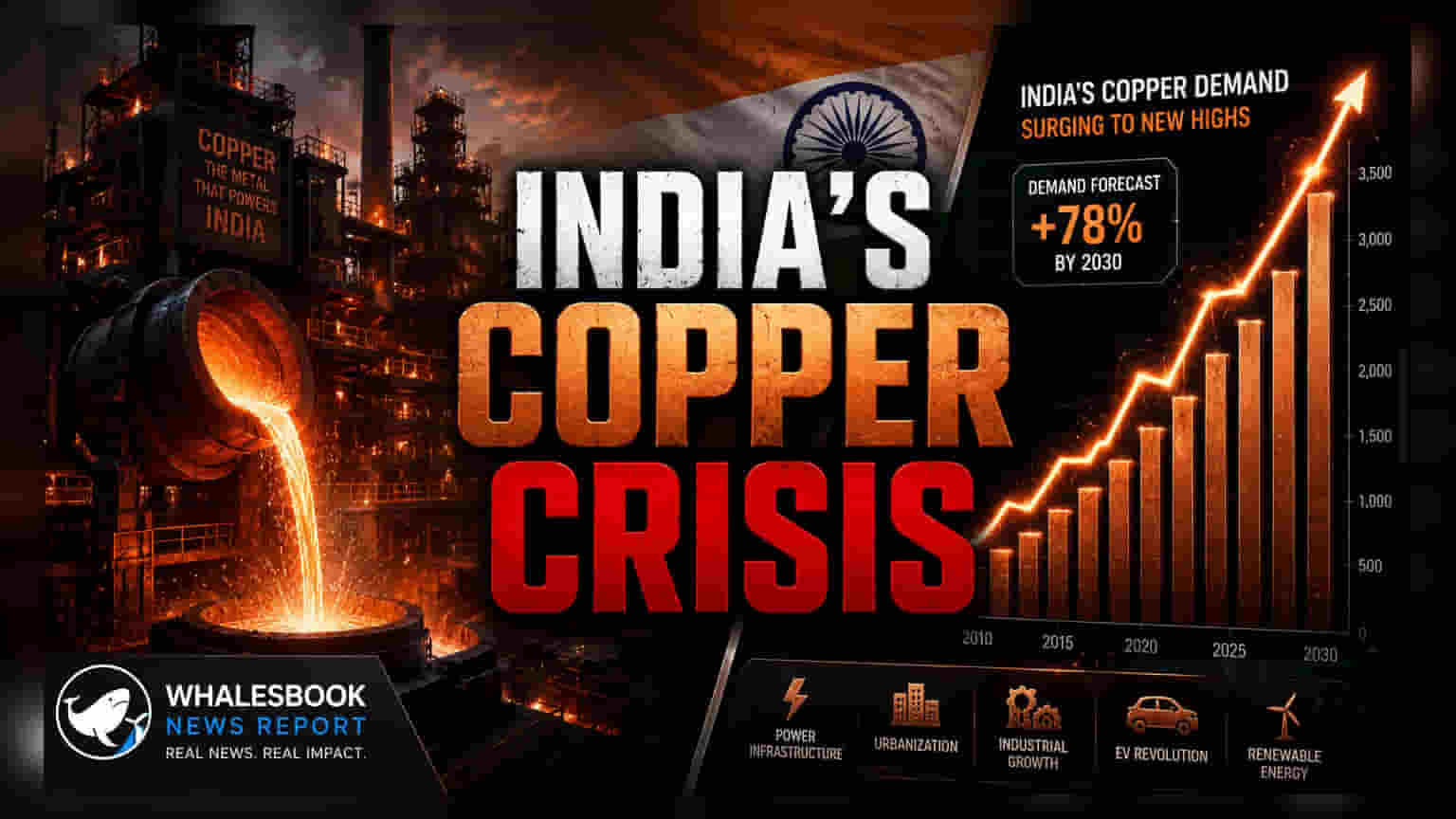

India’s annual copper demand reached 1.87 million tonnes in FY25, rising 9.3%. To bridge the growing supply gap, experts suggest the nation needs 500,000 tonnes of new refining capacity every five years. This structural deficit poses a challenge for domestic manufacturers and impacts reliance on imports for critical sectors like green energy and infrastructure.

What Happened

India is facing a widening gap between its domestic copper production and rising industrial demand. Data from the International Copper Association India (ICA India) indicates that the country consumed approximately 1,878 kilo tonnes (KT) of copper in the 2024-25 financial year, up from 1,718 KT in the previous year. To keep pace with this trajectory, experts estimate that India must add 500,000 tonnes of refined copper capacity every five years. Currently, domestic production remains insufficient to cover the total requirement, forcing the nation to rely on imports to fuel its economic activity.

Why This Matters For Investors

For Indian investors, this production deficit highlights both a structural demand story and a supply-side constraint. Copper is essential for power transmission, renewable energy infrastructure, and consumer durables. When domestic supply cannot meet demand, companies in sectors like construction, electrical equipment, and home appliances may face higher costs if they rely on imported copper, which is subject to global price volatility and currency fluctuations. Conversely, companies actively expanding domestic refining capacity may benefit from import substitution, provided they can manage execution risks and capital costs.

The Capacity And Production Picture

Recent efforts to boost domestic output include the restart of a secondary smelter by Hindustan Copper and new capacity additions by Hindalco Industries and Kutch Copper (a subsidiary of Adani Enterprises). While these projects collectively aim to add approximately 100,000 tonnes to the domestic supply, they remain modest when compared to the 1.8 million tonne demand. Investors should note that commissioning large-scale smelters involves significant capital expenditure and regulatory compliance. The speed at which these new facilities reach full operational efficiency will determine how much of the import burden can be reduced over the coming years.

Risks To The Demand Outlook

While demand growth is strong, it is not immune to cyclical pressures. The copper sector is highly sensitive to the building construction and infrastructure cycles. Any slowdown in government-led infrastructure spending or a cooling in the real estate sector could dampen the expected 9% demand growth. Furthermore, as a commodity-intensive sector, profit margins for copper producers and users are highly dependent on global LME (London Metal Exchange) price movements and raw material availability. Investors should be aware that excessive reliance on imported raw materials creates a natural hedge risk if domestic pricing does not move in sync with global costs.

What Investors Should Track

Moving forward, the primary monitorables include the commissioning timelines for the new smelter capacities at Hindalco and Kutch Copper. Investors may also track the import dependency ratio in upcoming annual reports of major copper-using companies. Additionally, any policy changes regarding import duties on copper or government incentives for domestic metal refining will be critical factors that could alter the competitive landscape for domestic players.