Hindustan Copper plans to invest Rs 7,188.6 crore by FY30 to nearly triple ore production. While the company recently reported strong earnings, investors are weighing this ambitious expansion plan against its high valuation compared to global copper peers.

What Happened

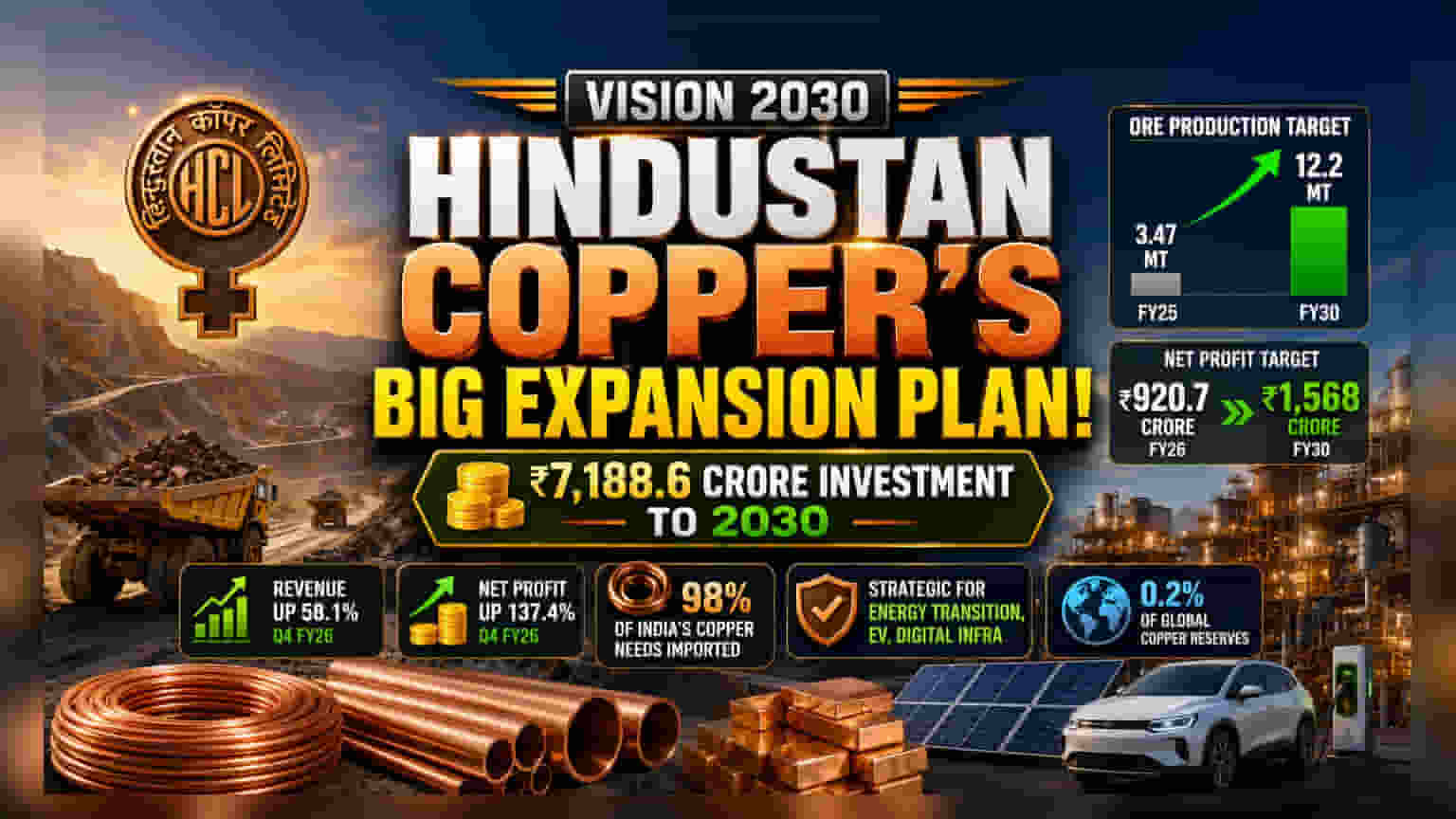

Hindustan Copper has announced an ambitious capital expansion plan under its 'Vision 2030' initiative. The company intends to spend Rs 7,188.6 crore by the fiscal year 2030. The primary goal of this investment is to ramp up ore production significantly, targeting an output of 12.2 million tonnes by FY30, compared to 3.47 million tonnes in FY25. Along with this production growth, the company has set a target to increase its net profit to Rs 1,568 crore by FY30, up from the Rs 920.7 crore recorded in FY26.

Why This Matters For Investors

Copper is a critical material for the global energy transition, electric mobility, and digital infrastructure. For an Indian public sector company, increasing domestic production is strategically important, as India currently imports 98% of its refined copper needs. The success of this expansion could reduce the country's import reliance and position the company to benefit from long-term demand for the metal. However, investors are balancing this growth potential against the execution risks involved in such a large-scale project.

The Valuation Question

While the growth plans are substantial, market participants are keeping a close watch on the company’s current valuation. Hindustan Copper is currently trading at a price-to-earnings (P/E) ratio of 49.9. This means investors are paying a premium compared to global copper mining giants. For comparison, global peers like Freeport-McMoRan trade at a P/E of 36.2, Southern Copper Corporation at 31.9, and BHP Group at 22.0. This difference suggests that the market has priced in high growth expectations, and investors are assessing whether the company can consistently deliver on its production targets to justify this valuation.

Financials And Production History

The company's recent financial performance has been robust. In the quarter ended March 2026, Hindustan Copper reported a 58.1% year-on-year increase in revenue and a 137.4% jump in net profit. For the full fiscal year 2026, the company recorded a 97% increase in net profit. However, historical operational data highlights the challenges the company has faced; in FY25, ore and metal-in-concentrate production declined by nearly 8% year-on-year. This history of production fluctuations makes execution efficiency a key point for shareholders to monitor as the company attempts to ramp up operations.

Market Dynamics and Sector Context

Copper prices are sensitive to global economic conditions. While the move toward clean energy and AI data centers drives long-term demand, copper prices have been volatile recently due to geopolitical tensions and concerns about industrial demand slowdowns. The company is also constrained by India’s limited copper reserves, which account for only 0.2% of global reserves. This structural limitation means the company’s growth is heavily dependent on its ability to maximize extraction from existing mines and successfully execute the new expansion projects.

What Investors Should Track

Moving forward, the primary monitorable for investors will be the execution speed of the 'Vision 2030' plan. Shareholders will likely look for consistent updates on project milestones, commissioning dates, and actual production numbers in upcoming quarterly reports. Additionally, keeping an eye on global copper price trends and whether the company can maintain its profit margins while scaling up production will be important. Investors may also watch to see if the company can meet these ambitious targets without needing to raise external capital, which could impact earnings per share.