Hindustan Copper aims to increase production capacity at its Malanjkhand mine to 5 million tonnes by 2030. This expansion is part of a broader goal to reach 12.2 million tonnes of total annual output, supporting domestic mineral security. Investors may watch the project's execution timeline and capital spending impact on the company's financial position.

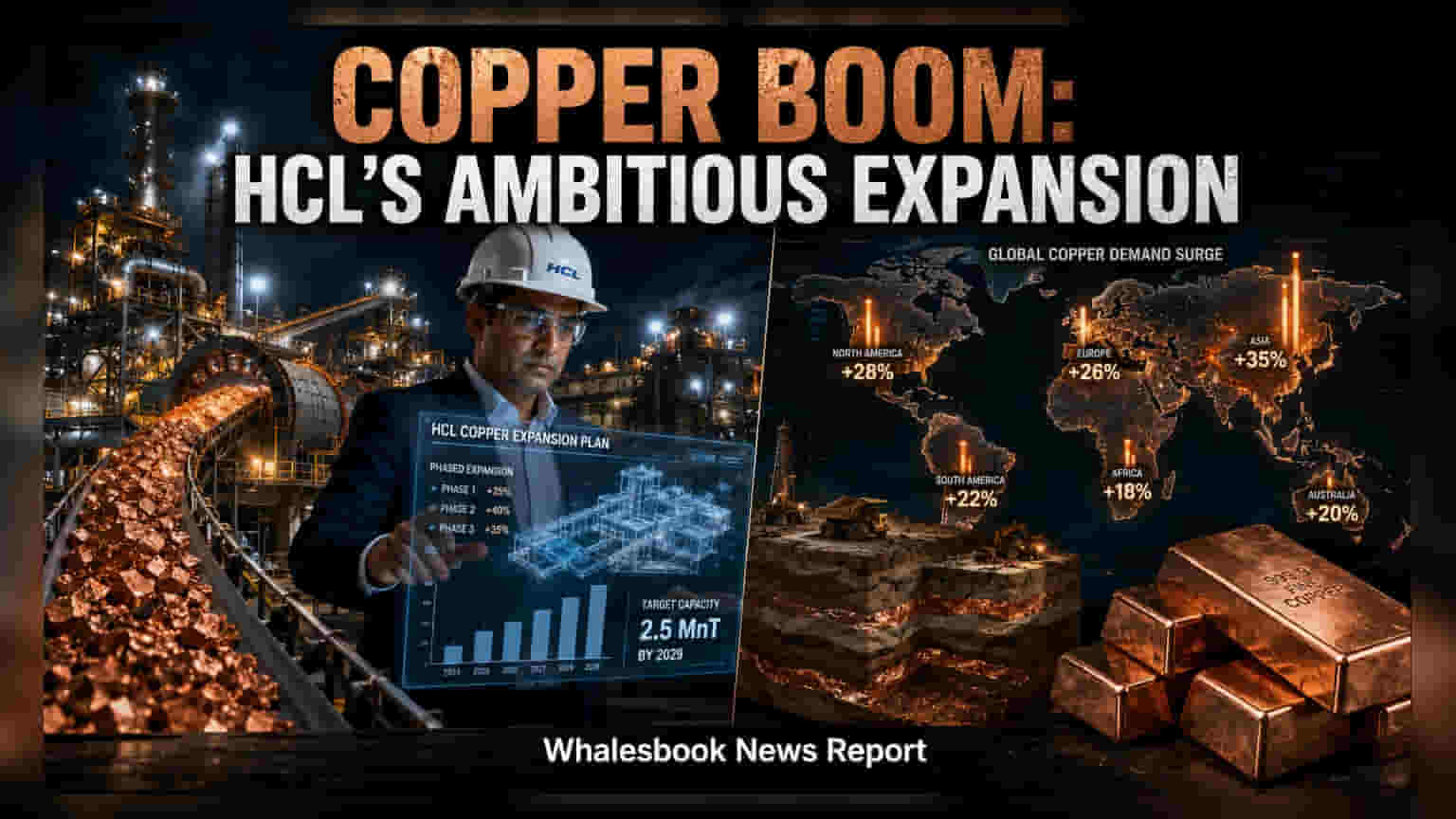

Hindustan Copper Limited (HCL) has set a clear growth target to scale its copper ore production to 12.2 million tonnes annually by 2030. A primary component of this strategy is the expansion of the Malanjkhand Copper Project (MCP) in Madhya Pradesh, where the company plans to double its capacity from 2.5 million tonnes to 5 million tonnes over the next four years.

Strategic Expansion at Malanjkhand

The Malanjkhand project is currently the backbone of the company's operations, contributing roughly 70% of its total output. To achieve the 5 million tonne goal, the company is building new production and service shafts alongside updated winder systems. Additionally, the project includes the construction of a new concentrator plant and a paste-fill plant, which are designed to support higher extraction volumes. As a state-owned entity, HCL is executing these plans to address the gap between domestic copper production and industrial demand within India.

Operational Priorities and Financial Context

Under new leadership, the company has indicated a focus on mission-mode execution to ensure that infrastructure projects meet their set deadlines. Because these expansions require significant capital spending, the primary investor monitorable will be how the company manages its cash flow and debt levels during this construction phase. While the company is also working to increase capacity at its Khetri Copper Complex in Rajasthan and the Indian Copper Complex in Jharkhand, the scale of investment required for these projects could impact the company's margins if execution costs rise or if project timelines are delayed.

Sector Dynamics and Risks

Copper is a highly cyclical commodity, and its price is heavily influenced by global supply and demand trends. While the move to increase domestic capacity aligns with long-term industrial growth, it exposes the company to risks associated with raw material price fluctuations and the high cost of maintaining large-scale mining operations. Furthermore, mining projects often face regulatory and environmental compliance hurdles, which can sometimes lead to unexpected delays or additional costs.

Investors should track the upcoming quarterly financial results for details on how much capital has been deployed toward these projects and how it affects the company's debt-to-equity ratio. The long-term success of this expansion plan will ultimately depend on the company's ability to maintain efficient operations while managing the substantial capital requirements needed to bring the expanded capacity online by 2030.