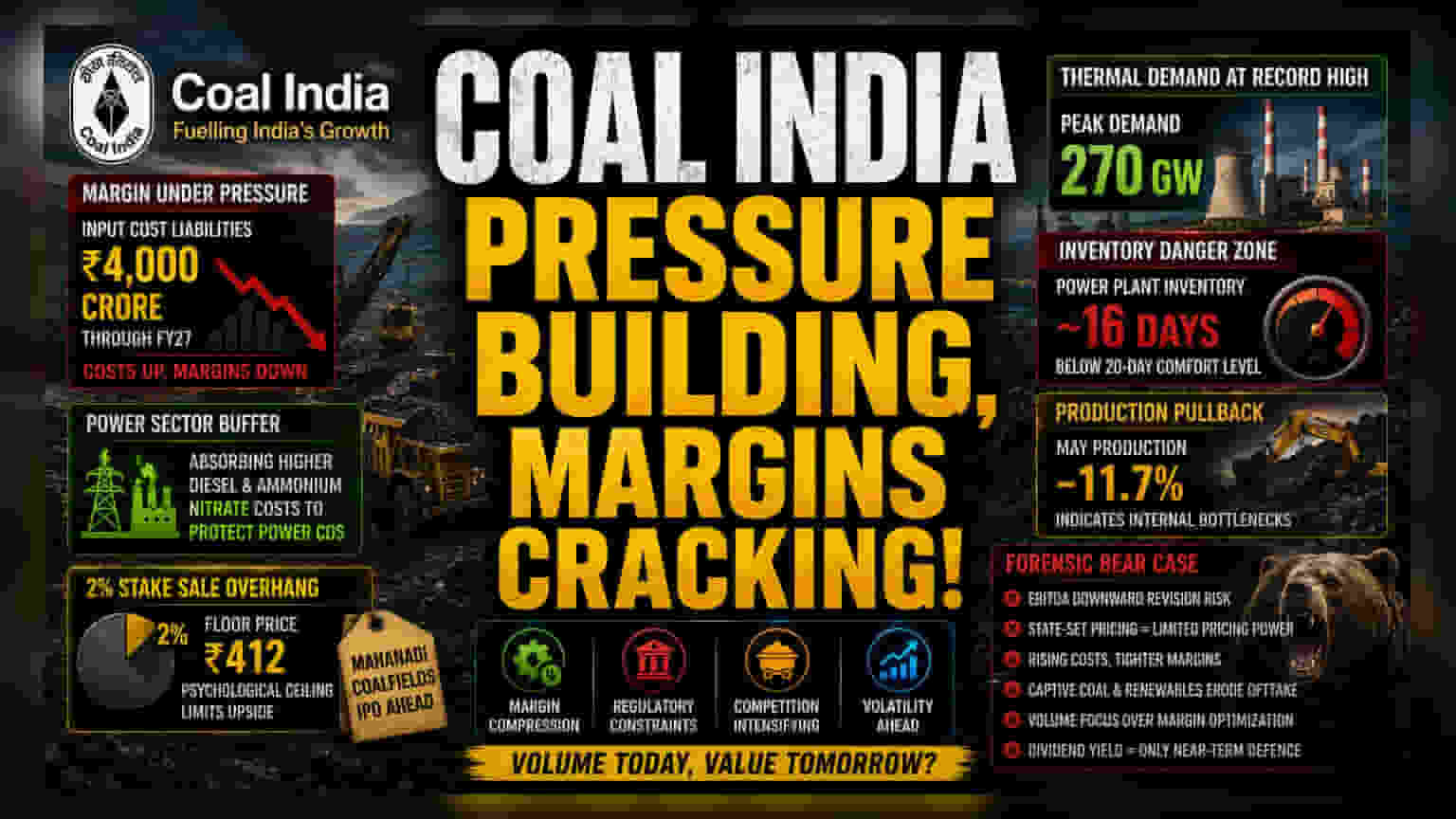

Structural Margin Compression and Cost Absorption

The narrative surrounding Coal India is often dominated by topline growth, yet the real story lies in the tightening of operating margins. By electing to shield downstream power utilities from the full brunt of spiking industrial diesel and ammonium nitrate prices, the company is effectively functioning as a buffer for the national power sector. This policy creates a structural drag on earnings that is unlikely to vanish in the short term. With input cost liabilities projected to reach ₹4,000 crore through FY27 if current geopolitical tensions persist, the reliance on operational efficiency to offset these expenses is reaching a breaking point.

The Divestment overhang

Market participants are currently pricing in the volatility associated with the government’s 2% stake sale. The floor price of ₹412 has created a psychological ceiling, tempering bullish sentiment as institutional investors weigh the dilution against the long-term value of the Mahanadi Coalfields listing. Unlike typical growth-focused equities, Coal India operates within a rigid regulatory framework where social mandates often override pure profit maximization. The pending IPO of Mahanadi Coalfields serves as a tactical move to unlock value, yet it simultaneously forces a re-evaluation of the parent company’s asset quality as the crown jewel subsidiary prepares for independence.

Competitive Vulnerability and Inventory Reality

While thermal power demand reaches a record peak of 270 GW, Coal India’s influence is being quietly challenged by the expansion of captive coal blocks and the structural integration of renewable energy. The decline in power plant inventory levels to roughly 16 days indicates a supply chain that is operating with razor-thin margins. Historically, when inventories drop below the 20-day threshold, production must accelerate aggressively; however, May’s 11.7% production pullback suggests internal bottlenecks that could stifle the company's ability to capitalize on elevated spot market e-auction premiums.

The Forensic Bear Case

Investors must account for the high likelihood of EBITDA downward revisions. Unlike private sector mining peers that possess greater pricing power and leaner cost structures, Coal India remains tethered to state-mandated pricing that struggles to keep pace with rapid commodity inflation. Furthermore, the management’s historical tendency to prioritize volume targets over margin optimization remains a lingering risk factor. Any further delay in production recovery, combined with the potential for captive supply expansion to cannibalize offtake, could leave the stock struggling to find a catalyst for a sustained valuation re-rating, leaving the dividend yield as the primary defense against potential price downside.