The Indian cement industry is battling surplus capacity and elevated fuel costs as supply growth outpaces demand. While infrastructure projects continue to drive consumption, the seasonal monsoon dip in the second quarter is expected to challenge volumes. Investors are watching for potential relief from lower fuel prices and company-led cost-saving measures in the second half of the fiscal year.

What Happened

The Indian cement industry is currently navigating a period of financial pressure as surplus capacity and rising input costs weigh on profitability. While infrastructure development continues to act as a key support for demand, volume growth remains under pressure from seasonal factors. With capacity expected to grow at roughly 8% annually through FY28, outpacing the 6-7% demand growth, the market is dealing with a significant supply-demand gap. This environment has made it challenging for companies to fully pass on cost increases, keeping profit margins under check.

The Supply-Demand Reality

Industry-wide capacity utilization currently hovers around 70%. The steady addition of new capacity is widening the gap between supply and demand, a trend expected to persist for the next few years. This imbalance often leads to aggressive pricing strategies among manufacturers attempting to protect their market share. In the first quarter of FY27, volume growth was estimated at around 5% year-on-year. However, the second quarter typically sees a decline in activity due to the monsoon season, which impacts construction schedules across many parts of India.

Cost Pressures And Margin Impact

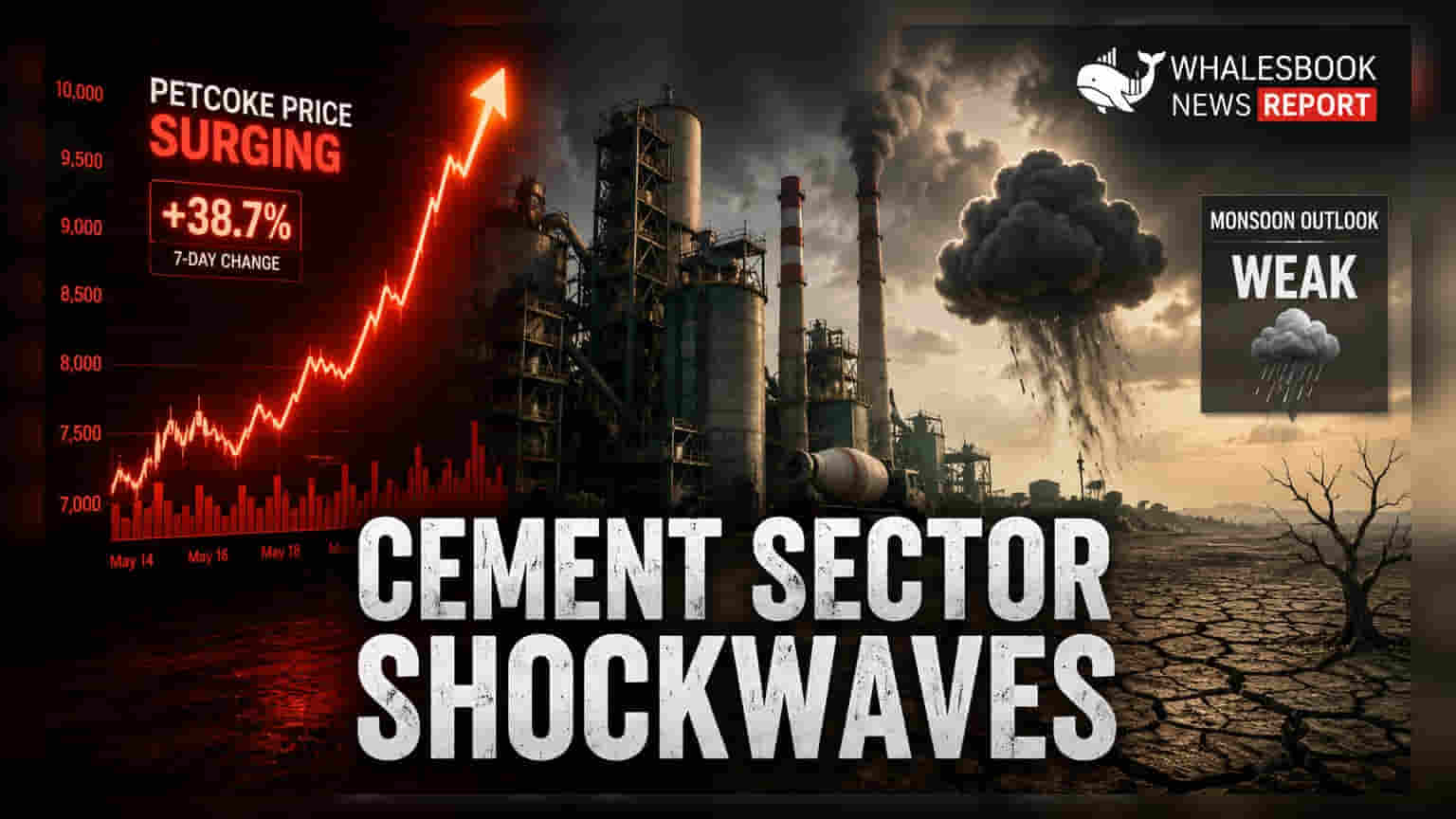

Profitability in the cement sector is sensitive to logistics and fuel costs. In the first half of FY27, fuel costs—primarily driven by coal and petcoke—rose by approximately Rs 325-350 per tonne. While international petcoke prices showed some moderation recently, overall fuel expenses remain higher compared to last year. Additionally, rising costs for diesel and packaging materials have further squeezed margins. To combat these challenges, many companies are focusing on cost-efficiency measures, such as increasing the use of renewable energy, optimizing logistics, and improving automation to reduce overheads.

Regional Demand Trends

Demand patterns have been uneven across the country. In the first quarter of FY27, the North and Central regions demonstrated better momentum compared to the South and East. The South and East, in particular, may face more pronounced volume declines in the coming months as new state governments focus on their policy agendas. Furthermore, a deficient monsoon season remains a risk, as it could dampen rural and semi-urban demand, leading to a steeper-than-expected seasonal slowdown in the second quarter.

What Investors Should Track

Investors are keeping a close watch on the second half of FY27, where a potential recovery in volume and lower fuel costs could offer relief. Key monitorables include the stabilization of petcoke and coal prices, as any further de-escalation in global energy prices could directly support margin recovery. Additionally, the sustainability of price hikes implemented in April and the success of internal cost-saving initiatives will be critical factors in determining whether companies can improve their return ratios, which have remained in the mid-single digits over the recent past.