Nomura expects Indian cement companies to show volume growth for the June quarter, but rising fuel and packaging costs are likely to lower profit margins. Investors may watch if price stability can offset these higher expenses as demand slows during the monsoon.

The Indian cement sector is set to navigate a difficult quarter as rising operating costs threaten to squeeze profit margins, according to a recent analysis by Nomura. While demand remains steady, with an estimated 6-7% year-on-year volume growth for the industry in the June 2026 quarter, the financial gains from this growth are expected to be limited by higher expenses.

Impact of Rising Fuel and Packaging Costs

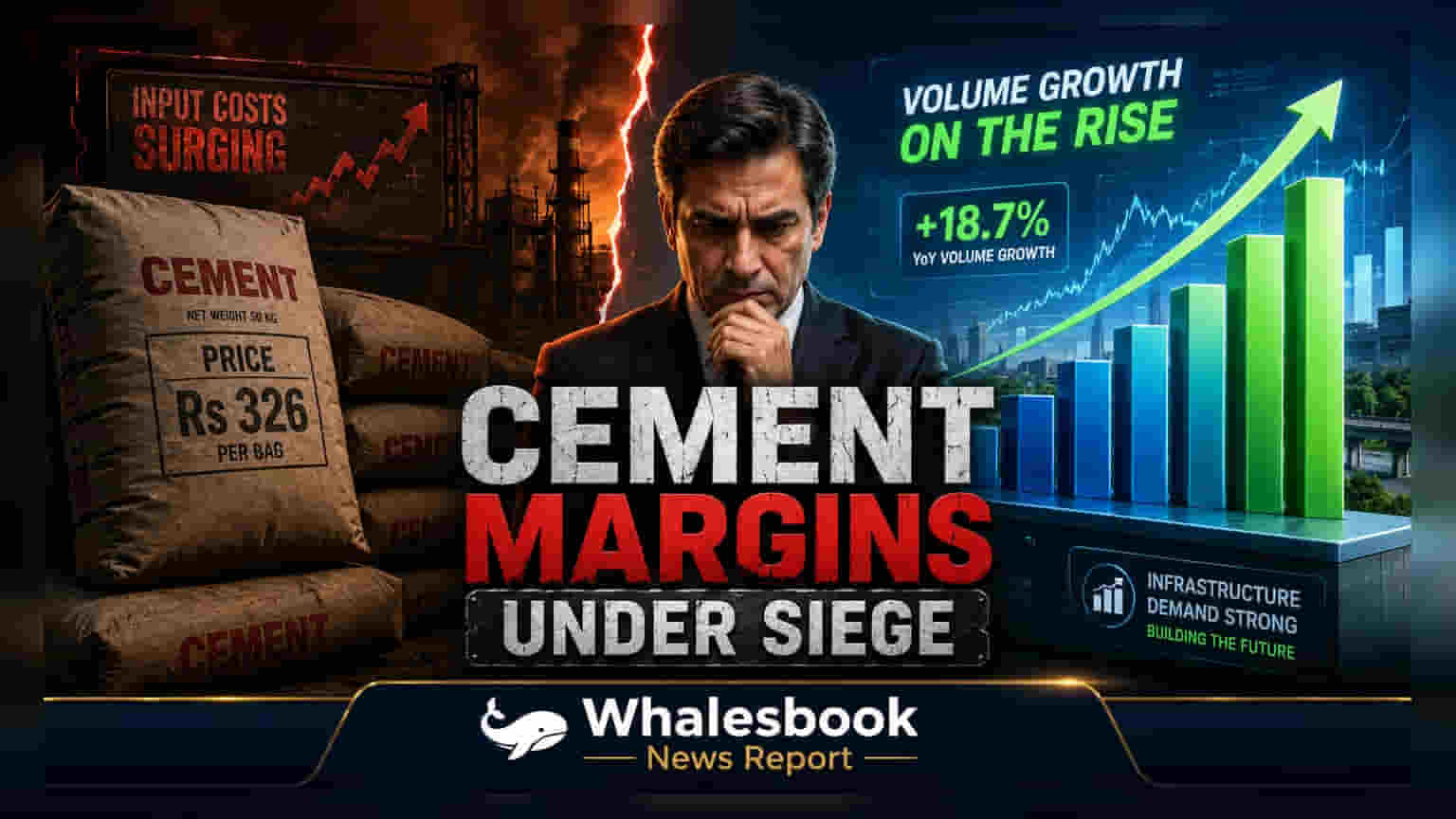

Profitability is facing downward pressure due to a significant rise in input expenses. The brokerage report notes a 4% sequential increase in operating costs per tonne. This is largely driven by geopolitical tensions, which have disrupted energy supply chains and pushed up the prices of key raw materials. Specifically, imported pet coke costs rose by 12% and thermal coal by 17% during the quarter compared to the previous three-month period. Increased diesel prices further added to the cost burden, forcing companies to absorb or pass on these expenses to customers.

Regional Pricing Trends and Profitability

To counter these rising costs, the industry implemented average price hikes of Rs 10 per bag during the quarter. This led to a sequential price improvement of approximately 3%, bringing the average price to Rs 326 per bag. Companies with a stronger presence in Northern and Western India are likely to show better performance as these regions demonstrated higher pricing power. Despite these efforts, the average EBITDA per tonne across the sector is projected to fall by Rs 50 compared to the previous quarter as cost increases outpace the benefit of higher product prices.

Strategic Outlook and Industry Performance

While the industry expects volume growth, the sustainability of margins will be a primary concern for investors in the coming months. With the monsoon season typically leading to a seasonal slowdown in construction activity and cement demand, the ability of companies to maintain current price levels will be crucial. Future profitability will depend less on input cost reductions and more on the industry's ability to protect pricing in a softer demand environment. Among individual players, some companies are expected to navigate these pressures better than others, with Shree Cement projected to see strong volume growth, while Ambuja Cement is noted as a potential exception for its ability to maintain its profit margin per tonne.