What Happened

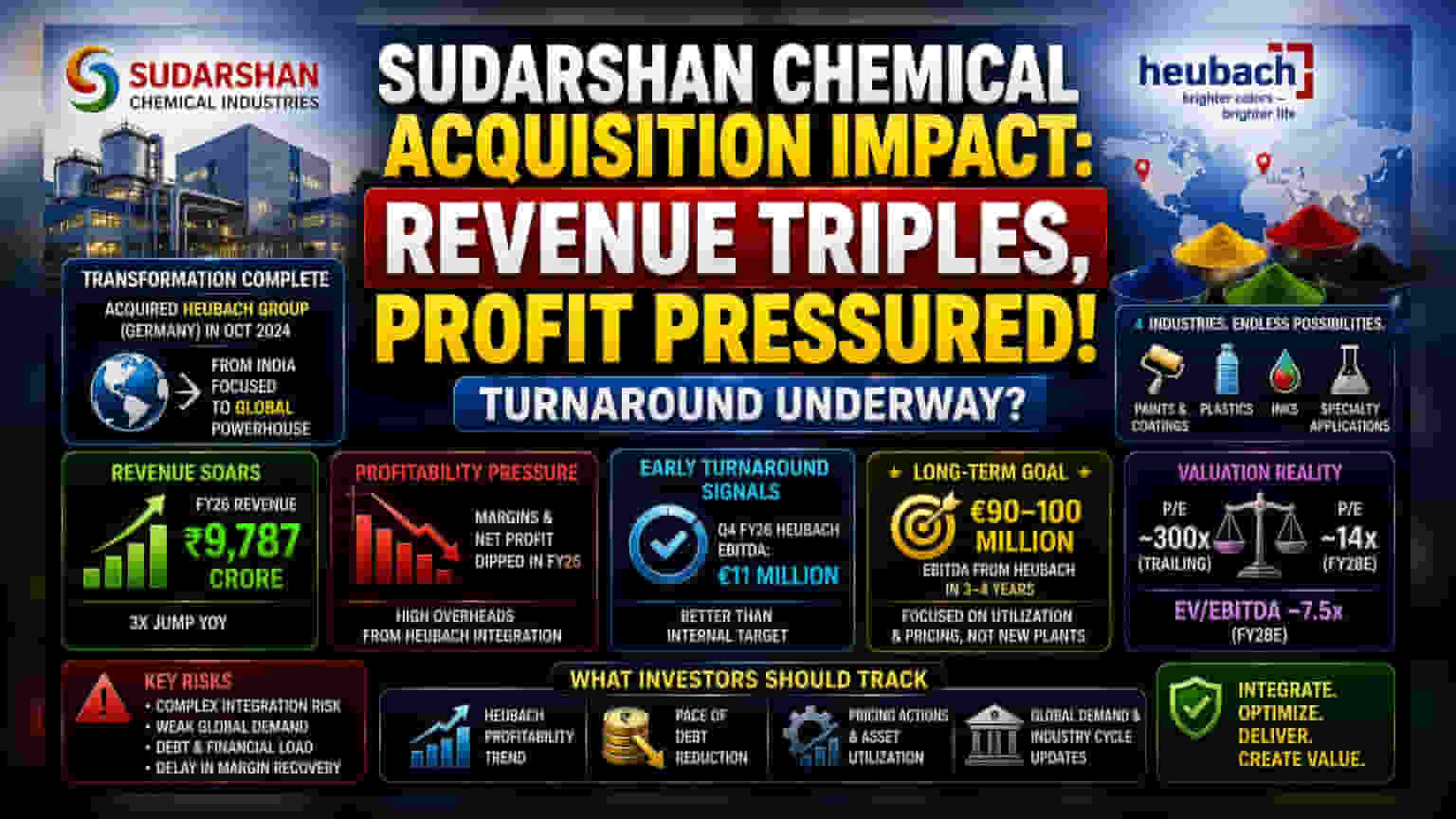

Sudarshan Chemical Industries, a major player in the Indian pigment market, completed a significant transformation by acquiring the Germany-based Heubach Group in October 2024. This deal was a major shift, moving the company from a domestic-focused business to a global entity. The impact on the top line was immediate, with the company's revenue tripling to ₹9,787 crore in the financial year 2026. This acquisition provided access to new markets in the US and Europe and added specialized technology to the company's product portfolio.

The Profitability Challenge

While the revenue jump was significant, the integration of Heubach brought serious financial strain. Heubach was dealing with insolvency before the takeover, meaning it came with baggage including high overheads and operational inefficiencies. Because of this, Sudarshan saw a sharp dip in operating margins and net profit during FY26. The company chose to absorb these extra costs to ensure it could keep supply chains running and maintain relationships with the customers it inherited from the deal. For investors, this meant that while the business became larger, it also became less profitable in the short term.

Signs of Turnaround

There are early signs that the integration efforts are beginning to pay off. In the fourth quarter of FY26, the Heubach operations showed a positive trend, generating €11 million in EBITDA, which was better than what the company had internally targeted. The management has also focused on cleaning up the balance sheet by reducing inventory levels and lowering net debt. The company’s long-term goal is to reach an EBITDA contribution of €90 million to €100 million from the Heubach operations within the next three to four years. The management believes this can be done by improving how existing assets are used and adjusting pricing, rather than by spending massive amounts on new factories.

The Valuation Confusion

Investors looking at the stock might notice a very high trailing price-to-earnings (P/E) ratio, which is currently around 300x. It is important for investors to understand that this number is skewed because the company's profits took a major hit during the restructuring phase in FY26. When analysts look ahead to FY28, they estimate a much lower P/E of around 14x and an EV/EBITDA of 7.5x. These future-looking numbers suggest that the market is waiting to see if the company can return to normal profit margins as the integration settles.

Risks and Concerns

Integrating an insolvent company is a complex and risky task. The primary risk for shareholders is execution; if the company fails to streamline Heubach’s operations or if global demand in the paint and coating sector weakens, the planned margin recovery could be delayed. Additionally, while net debt has begun to decrease, the company still carries the financial weight of the acquisition. Any failure to manage this debt or a slowdown in the chemical sector could pressure the company’s financial health.

What Investors Should Track

Moving forward, investors will likely monitor a few specific points. First, the quarterly profitability of the Heubach operations is critical to verify that the turnaround is sustainable. Second, the pace of debt reduction will be a key indicator of financial stability. Finally, any management updates on pricing actions and asset utilization will show whether the company is successfully passing on costs and improving efficiency without needing to invest significant new capital.