Sudarshan Chemical Navigates Post-Acquisition Landscape with Revenue Boom and Net Loss

Sudarshan Chemical Industries Limited has reported a dramatic financial shift following its acquisition of the Heubach Group, showcasing a monumental leap in consolidated revenue alongside a significant net loss for the quarter and nine months ended December 31, 2025 (Q3 FY26).

📉 The Financial Deep Dive

The Numbers:

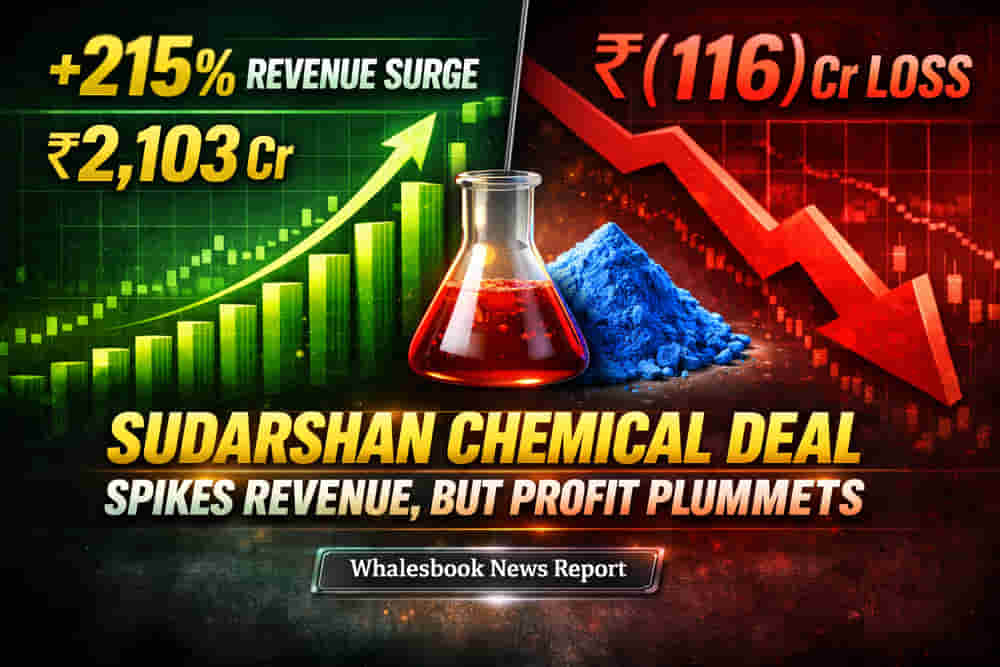

- Consolidated Revenue: Surged by an astounding 215% year-on-year to ₹2,103.0 crore in Q3 FY26. This colossal increase is primarily attributed to the completion of the Heubach Group acquisition on March 3, 2025.

- Consolidated Net Loss: In stark contrast to the revenue growth, the company reported a consolidated net loss of ₹116.0 crore for the quarter, a significant downturn from a marginal profit of ₹0.5 crore in the corresponding prior period.

- Consolidated Diluted EPS: Stood at ₹(14.7) for the quarter.

- Standalone Revenue: Showed resilience with a slight decrease of 4.1% year-on-year to ₹550.3 crore.

- Standalone Net Profit: Witnessed a robust 40% year-on-year growth to ₹22.5 crore.

- Standalone Diluted EPS: Improved to ₹2.9 from ₹2.3 year-on-year.

- Exceptional Items: The consolidated results were impacted by exceptional items totalling ₹45.4 crore, including costs related to new Labour Codes and acquisition integration expenses. Standalone results also bore exceptional items of ₹26.5 crore.

The Quality & Scale Shift:

The acquisition of Germany's Heubach Group for €151.9 million (approximately ₹1,389.9 crore) has fundamentally altered Sudarshan Chemical's scale. Consolidated segment assets ballooned from ₹2,618.9 crore in Q3 FY25 to ₹9,620.4 crore in Q3 FY26. The transaction resulted in a provisional bargain purchase gain of ₹1,243.9 crore, recognized in Other Comprehensive Income (OCI), rather than impacting the profit and loss statement directly. Crucially, the company noted that the financial results for the current period are not comparable with previous periods due to this transformative acquisition.

The Grill (Implied Narrative):

While no direct management grilling occurred in this filing, the financial report presents a compelling narrative: a massive revenue injection from a strategic acquisition versus an immediate profitability hit. The market will keenly observe how the company integrates Heubach, realizes synergies, and navigates the challenges of turning around the acquired entity, which has previously faced financial headwinds. The resilience of the standalone business offers a positive offset, but the consolidated picture demands investor scrutiny regarding the acquisition's long-term value creation.

🚩 Risks & Outlook

- Integration Risk: The paramount challenge lies in the seamless integration of the Heubach Group and realizing the projected synergies to drive profitability.

- One-Off Impact: Significant exceptional items directly impacted the quarterly net loss, highlighting the temporary costs associated with the acquisition and regulatory changes.

- Guidance Vacuum: This announcement did not include forward-looking guidance from management, leaving investors to await further insights from the scheduled analyst call.

- Financial Leverage: The acquisition likely involves significant debt, necessitating careful management to ensure debt servicing and financial stability.

- Valuation Scrutiny: Sudarshan Chemical historically traded at a premium valuation. The current consolidated results, particularly the net loss, could pressure this valuation if integration and profitability challenges persist.

Investors will be closely watching the company's ability to leverage its expanded global footprint and product portfolio while effectively managing costs and debt in the upcoming quarters.