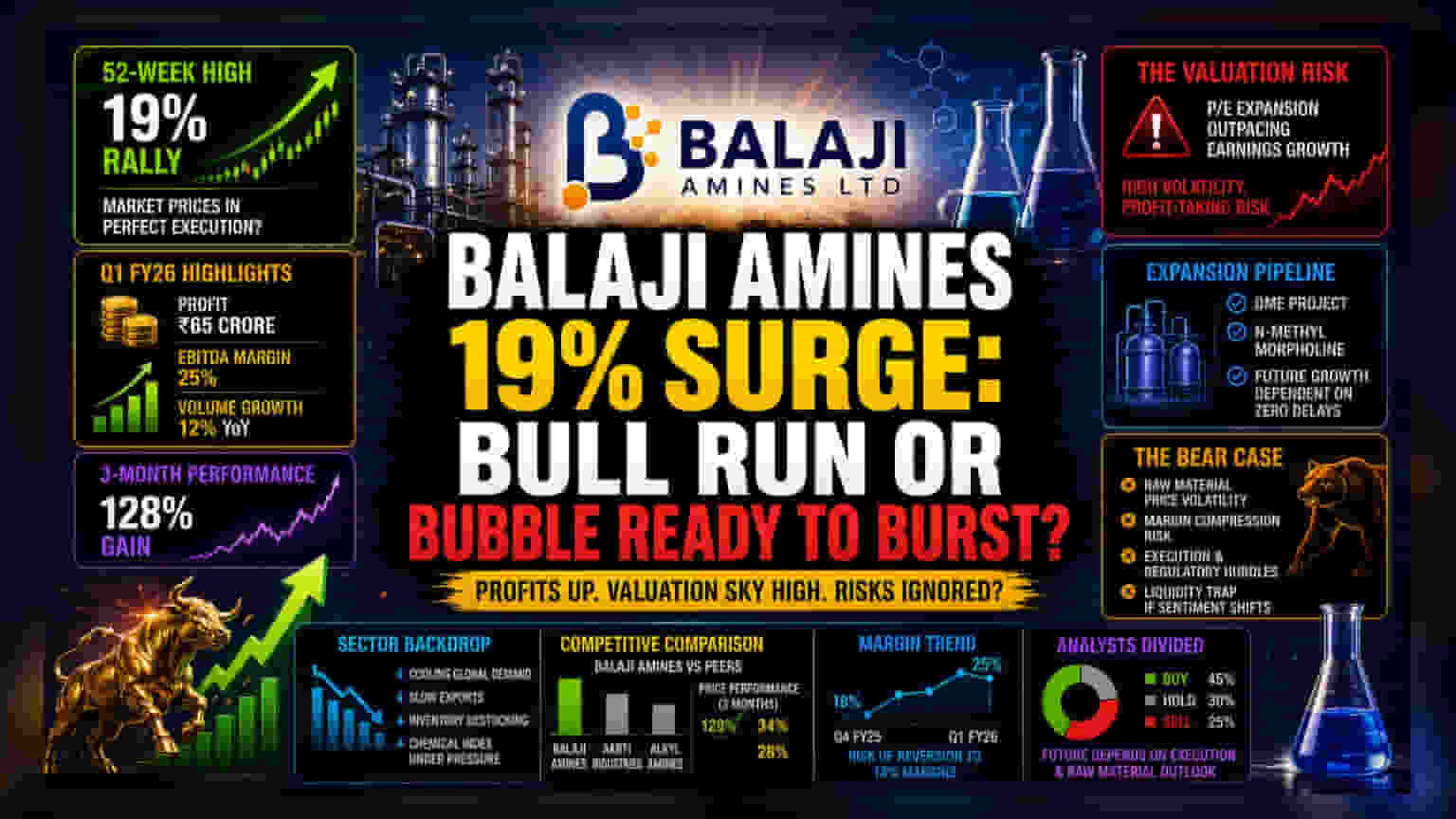

The Valuation Disconnect

The explosive 19% rally to a 52-week high reveals a market aggressively pricing in future capacity additions while potentially overlooking the cyclical nature of the recent margin expansion. Investors are currently hyper-focused on the ₹65 crore profit print, yet the primary driver—a sharp improvement in EBITDA margins to 25%—relied heavily on temporary raw material cost stabilization. As the specialty chemical sector experiences cooling global demand, the divergence between the stock's parabolic trajectory and the underlying commodity price environment suggests that the current valuation assumes perfect execution on upcoming projects like DME and N-Methyl Morpholine.

Competitive Benchmarking and Sectoral Pressure

When placed against peers like Aarti Industries or Alkyl Amines, the recent price action in Balaji Amines appears significantly decoupled from sector beta. While the broader chemical index has struggled with sluggish export volumes and inventory destocking throughout Q1, Balaji Amines has benefited from a concentrated product mix. However, the 128% three-month gain implies a massive shift in market expectations that may not be supported by the current volume growth of 12%. Historical data indicates that when specialty chemical stocks reach such rapid verticality, they often trigger institutional profit-taking, particularly when the P/E expansion outpaces earnings growth by this wide a margin.

The Forensic Bear Case

The optimism surrounding the company's expansion plans ignores significant execution and regulatory risks inherent in the specialty chemical manufacturing process. Management has historically faced scrutiny over capital allocation efficiency during aggressive expansion phases. Furthermore, the reliance on a favorable product mix creates a structural weakness; any sudden shift in input costs for key precursors would likely lead to rapid margin contraction, as the company lacks the pricing power of larger global competitors. Given that the current rally is fueled by high trading volumes, the stock is increasingly vulnerable to a liquidity trap should sentiment shift toward defensive positioning in the face of rising interest rates and geopolitical uncertainty.

Forward Guidance and Institutional Sentiment

Looking toward the next two quarters, analysts remain divided on whether the company can maintain these elevated profit levels. While the commissioning of new projects is expected to diversify the revenue stream, the market is currently pricing in zero delays. Future performance will likely be dictated by the company's ability to navigate the hardening of raw material prices, which could easily compress those newly minted 25% margins back to the 18% levels observed just one quarter prior.