Global brokerage UBS has lowered its rating on Waaree Energies to 'Neutral' and reduced its price target to ₹3,100. The revision follows concerns over the company's aggressive expansion plans and weakening profitability in the solar manufacturing sector. Investors are now focused on how the company manages its large capital spending and competitive pressures from integrated peers.

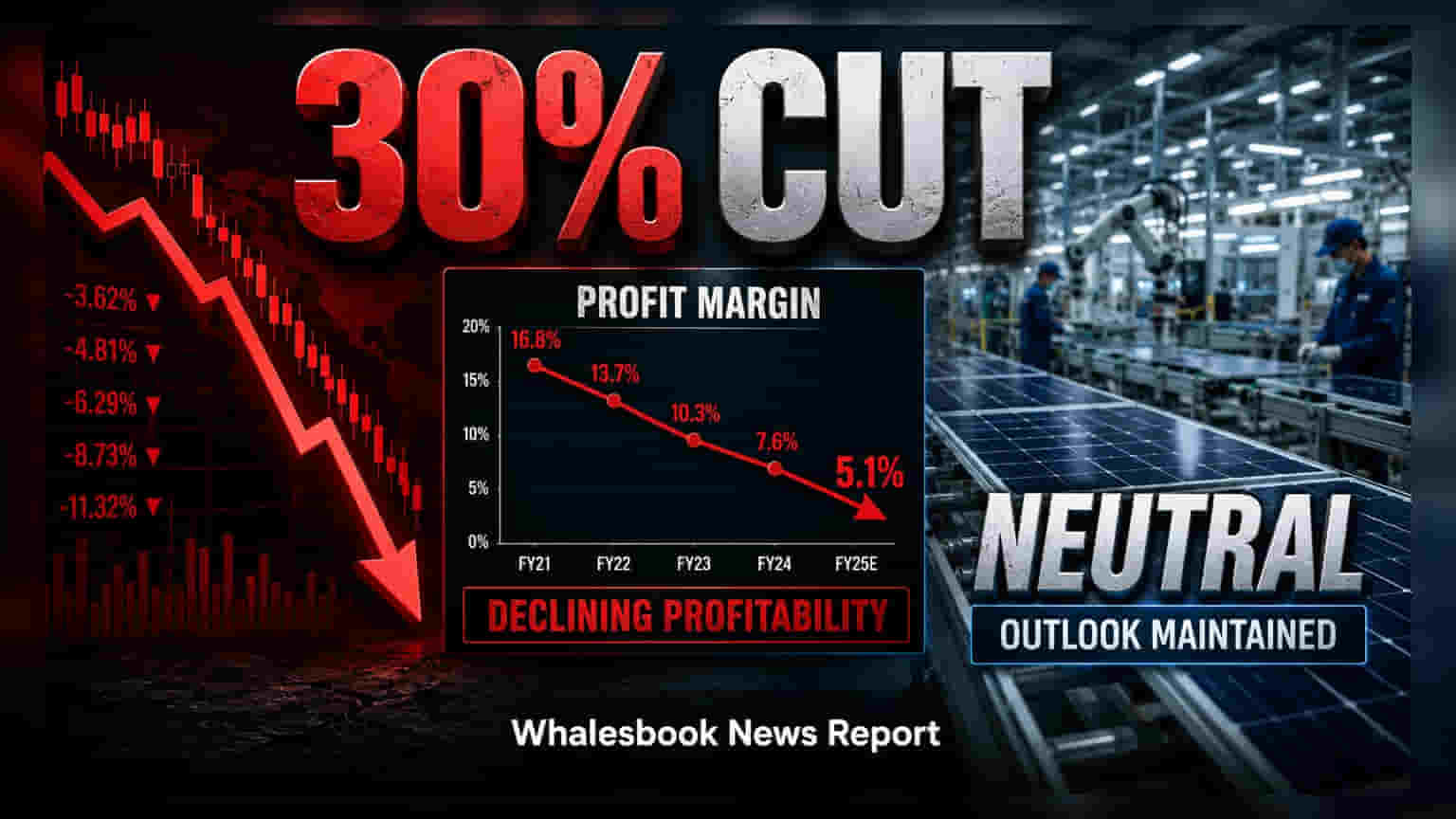

Global brokerage UBS has downgraded Waaree Energies to 'Neutral' from 'Buy' while cutting its price target by 30% to ₹3,100 from the earlier ₹4,400. This downward revision comes as the solar industry faces a phase of consolidation, prompting analysts to reassess the growth trajectory of major manufacturers.

Capital Spending and Execution Risks

A primary factor behind the downgrade is the company's massive expansion strategy. Waaree Energies has outlined plans for capital spending totaling ₹30,000 crore, a significant increase from its previous ₹13,000 crore commitment. This investment is directed toward expanding its solar module capacity to 15.4GW and building cell and ingot-wafer capacity to 10GW by the financial year 2028. While this scale is intended to strengthen its market position, UBS analysts pointed out that such aggressive spending creates execution risks and could place pressure on the company’s financial health if market conditions do not support the anticipated demand.

Profitability and Sector Pressures

The brokerage also highlighted concerns regarding the company's profitability. Earnings estimates for FY27 and FY28 have been reduced by 11% and 5% respectively, as margins in both Domestic Content Requirement and non-Domestic Content Requirement segments face pressure. The solar manufacturing sector is currently experiencing heightened competition and pricing challenges, which may impact the returns on these new projects.

Furthermore, there is limited visibility regarding the scalability and profitability of the company’s entry into Battery Energy Storage Systems. As this segment remains heavily dependent on imports, investors are expected to track how the company navigates cost structures and competition in this new area.

Competitive Position and Industry Trends

In its assessment, UBS noted that players with stronger backward integration—where a company produces its own raw materials or components—are better prepared to handle the current industry environment. The brokerage indicated a preference for peers like Premier Energies, noting that their expansion strategy appears more measured and their execution record more consistent.

For investors, the long-term outlook will depend on whether Waaree Energies can execute its projects without overleveraging its balance sheet. Future updates on project commissioning timelines, the stability of profit margins amidst sector-wide price fluctuations, and the success of its battery storage segment will be essential to track. Any improvements in export demand or a broader recovery in solar industry pricing could serve as potential triggers for the stock, though current market conditions necessitate a more cautious approach.