Turtlemint Fintech Solutions’ IPO is now open, aiming to raise ₹882.67 crore. The company saw strong interest from anchor investors, signaling institutional confidence. However, analysts are divided. Supporters highlight the firm's vast network of insurance partners as a key growth driver, while skeptics point to persistent losses, high partner commission payouts, and rich valuations as significant concerns.

What Happened

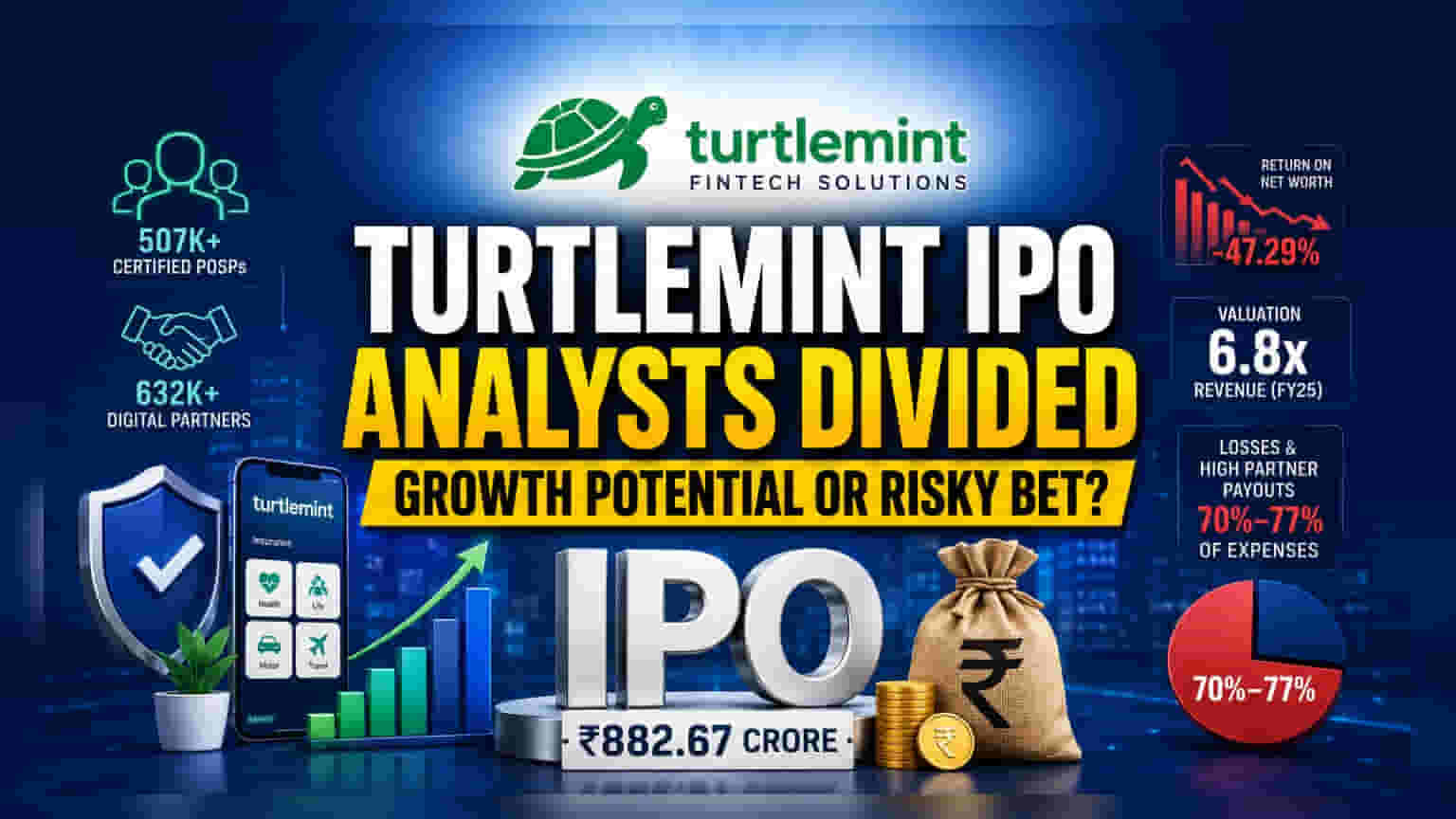

Turtlemint Fintech Solutions has launched its Initial Public Offering (IPO) on June 19, 2026. The company is looking to raise a total of ₹882.67 crore, consisting of a fresh issue of shares worth ₹660.72 crore and an offer for sale by existing shareholders valued at ₹221.95 crore. The company has set a price band of ₹144 to ₹152 per share. Ahead of the public launch, the company secured ₹397.20 crore from 32 anchor investors, including institutional names like ICICI Prudential Equity & Debt Fund and Mirae Asset. These shares were allocated at the top end of the price band, suggesting that institutional investors see potential in the company’s business model.

Why The Analyst Views Are Split

The market reaction to this IPO is clearly divided, with brokerage houses holding contrasting views. On one side, SMIFS has recommended subscribing to the issue. Their positive stance is based on the company's extensive digital footprint and the expected growth in India's insurance sector. They point to the firm’s network of over 507,000 certified Point of Sale Persons (PoSPs) and 632,000 Digital Partners as a significant business advantage, especially in smaller, Tier 30+ cities. They view this massive distribution network as a foundation for long-term growth, particularly as the company expands into mutual funds and loan distribution.

On the other side, Swastika Investmart has suggested avoiding the IPO. Their caution stems from the company's current financial health. The brokerage flagged the firm’s status as a loss-making entity and pointed to a negative Return on Net Worth of 47.29%. They also described the valuation of approximately 6.8 times the revenue for the financial year 2025 as rich, given the losses. This highlights a classic debate between betting on future digital scale versus looking at current financial performance.

The Financial and Business Context

To understand the company’s financial pressure, investors should look at its cost structure. A significant portion of the company's expenses, roughly 70% to 77%, goes toward payments to its Digital Partners. This indicates that the business is highly dependent on payouts to maintain its distribution network. While this model allows for rapid expansion without the heavy cost of physical branches, it also means that profitability is closely tied to how efficiently these partners can sell products. The company's financials, including a sharp year-on-year revenue decline noted in the previous fiscal year, underscore the difficulty of achieving consistent profitability in this tech-driven insurance distribution space.

Risks and Concerns

For investors, the primary risks involve the company's path to profitability and its cost management. The business model relies heavily on a large network of third-party sellers, and as seen in the expenses data, a large majority of revenue is shared with these partners. Investors may need to consider whether the company can maintain or increase its margins as it scales or if it will continue to face pressure from these high variable costs. Additionally, the negative return on equity suggests that the company is still in the phase of burning cash to drive growth, which can be a point of concern for investors seeking stability rather than high-risk, long-term bets.

What Investors Should Track

Investors may want to monitor the subscription data in the coming days to gauge the broader market appetite. Beyond the listing, the key areas to watch will be the company’s ability to turn its user base into profitable revenue and whether it can reduce its high reliance on partner payouts as a percentage of its total expenses. The company has stated it will use the funds for cloud and server infrastructure and product development, so the success of these technological upgrades in improving efficiency will be a major monitorable for the long-term health of the business.