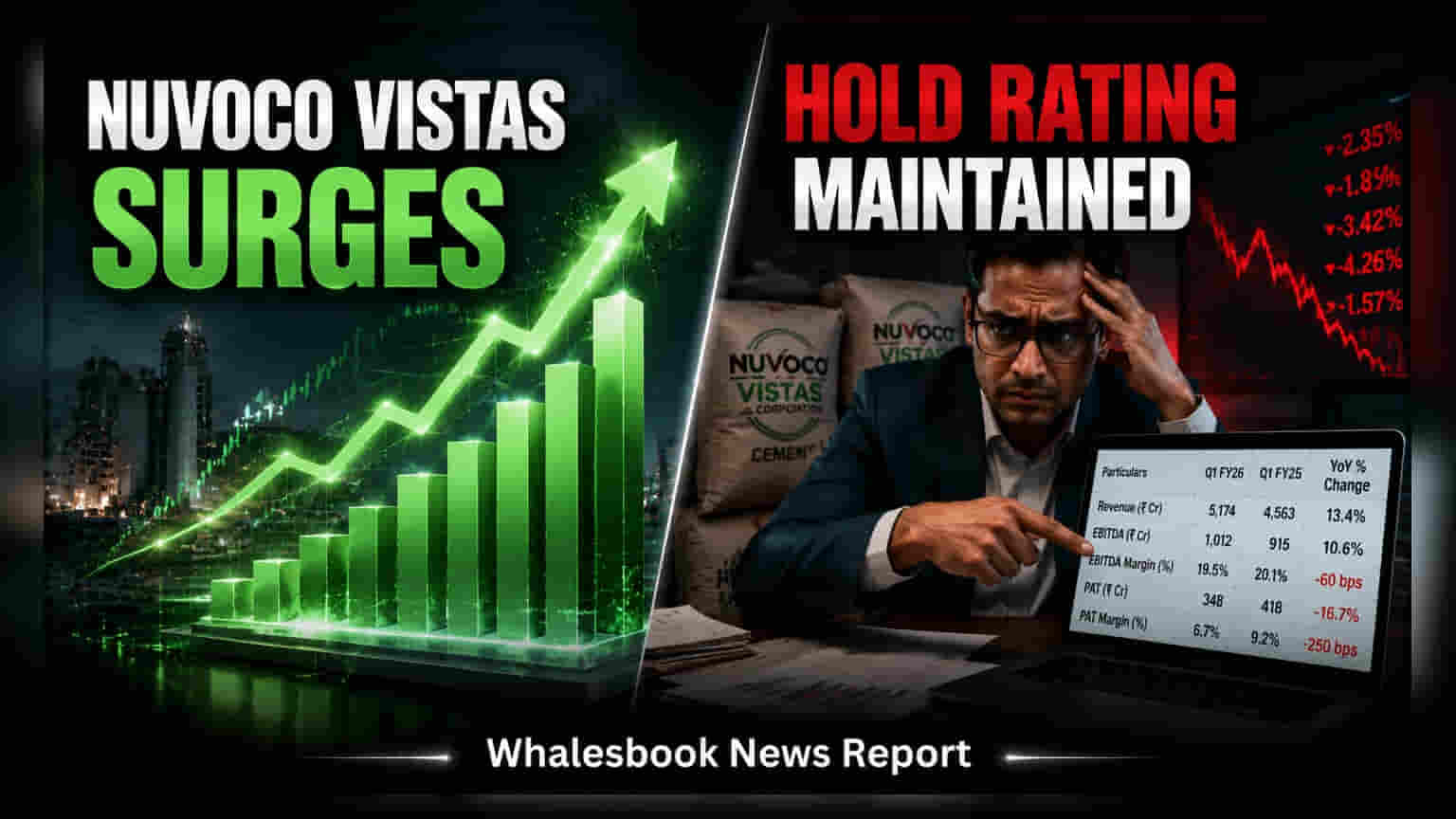

Nuvoco Vistas saw a better-than-expected Q1FY27 performance, with EBITDA per tonne reaching ₹1,072. However, ICICI Securities has maintained a 'HOLD' rating, citing concerns over high debt levels and low return on equity despite raising its price target to ₹358.

Nuvoco Vistas Corporation delivered a strong operational performance in the first quarter of fiscal year 2027, exceeding market expectations due to improved price realisations. Following these results, ICICI Securities has updated its outlook on the stock, increasing its price target to ₹358 from ₹320 while retaining a 'HOLD' recommendation.

Operational Gains in Q1FY27

The company reported an EBITDA per tonne of ₹1,072 for the quarter, marking a 10% increase compared to the previous quarter and a 5% rise year-on-year. This performance was notably 29% higher than the brokerage’s initial projections. The primary factor behind this improvement was a 7.6% quarter-on-quarter rise in realisations, which significantly outpaced the anticipated 3% growth. This operational success has prompted the brokerage to lift its EBITDA estimates for both FY27 and FY28 by 11% and 7%, respectively.

Structural Challenges and Market Risks

While the recent quarterly numbers indicate improved operational efficiency, analysts remain cautious about the long-term outlook. Key areas of concern include the company’s balance sheet, specifically its high debt levels, with net debt to EBITDA currently projected at 2.2x for FY27. Additionally, the company is grappling with a muted return on equity of approximately 5%, a metric that limits its attractiveness compared to more efficient players in the cement sector.

The broader cement industry also faces several challenges that could impact Nuvoco Vistas in the coming quarters. Competitive intensity remains elevated due to aggressive capacity expansion by major industry players, which puts constant pressure on pricing power. Furthermore, the company must contend with the possibility of subdued demand if the monsoon season remains weak, alongside the ever-present volatility in global fuel costs, which directly impacts production expenses. These persistent structural and macro factors are the primary reasons behind the conservative rating, suggesting that operational improvements need to be sustained over a longer period to overcome existing debt and return-ratio limitations.

Investors monitoring the stock will likely watch for future management commentary regarding debt reduction strategies and capital spending plans. Other critical monitorables include the trend in cement realisation prices, sustained improvement in EBITDA margins, and whether the company can effectively navigate the ongoing capacity-led competition within the Indian cement market.