Motilal Oswal Securities has issued positive outlooks for Marico, Kalyan Jewellers, and PN Gadgil Jewellers, citing strong revenue growth and expansion plans. Investors should note that these projections depend on future earnings and market conditions. The brokerage expects these firms to benefit from cooling raw material costs or aggressive retail growth in the coming quarters.

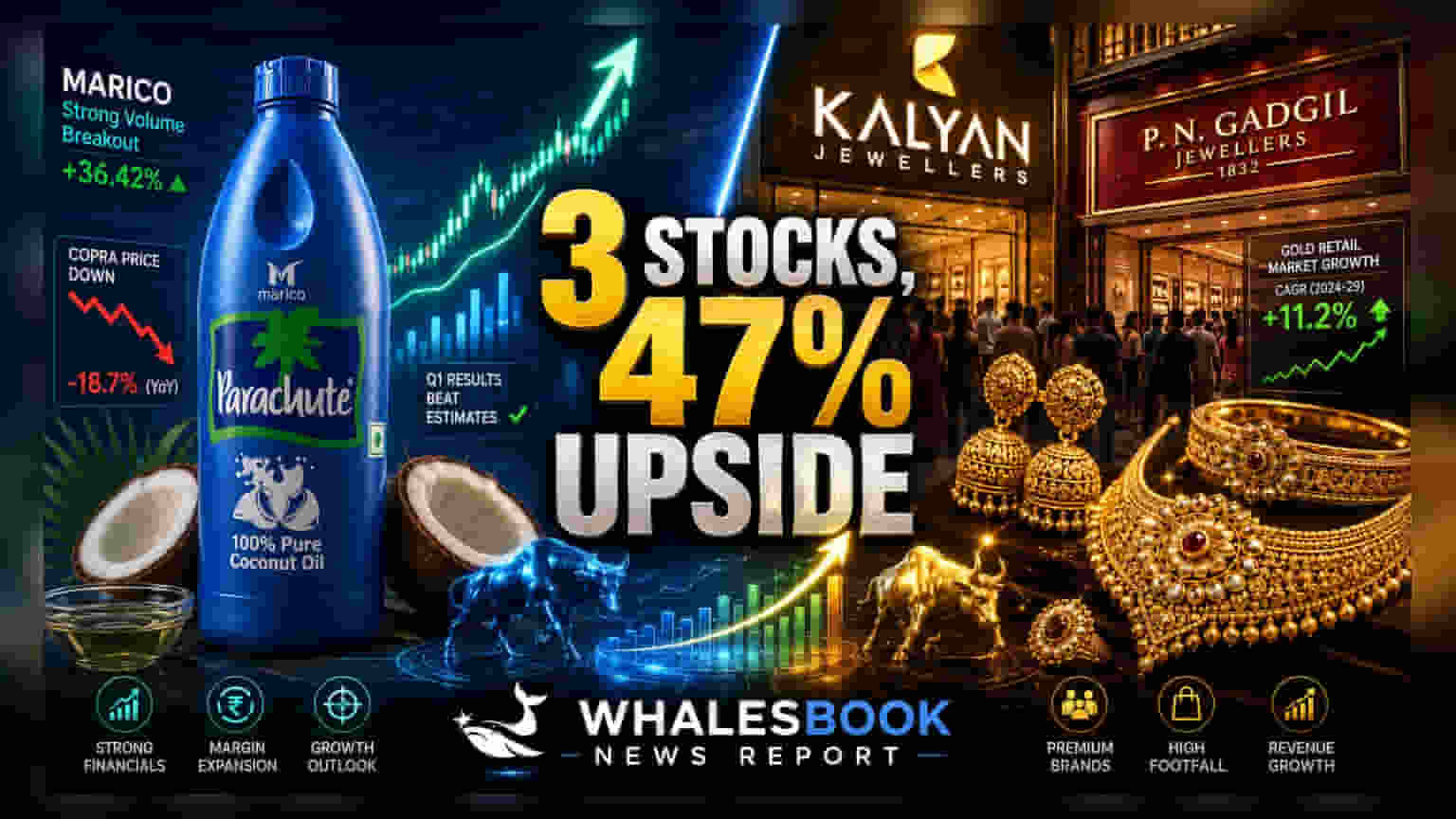

Motilal Oswal Securities has released a report highlighting growth prospects for three consumer-focused companies: Marico, Kalyan Jewellers, and PN Gadgil Jewellers. The brokerage firm points to strategic business initiatives and favorable cost trends as reasons for its positive outlook on these stocks.

Kalyan Jewellers and PN Gadgil Jewellers Expansion

The jewellery sector has shown strong activity, with both Kalyan Jewellers and PN Gadgil Jewellers reporting robust revenue growth for the first quarter of the 2027 financial year. Kalyan Jewellers recorded a 38% year-on-year rise in consolidated sales. The company has been aggressively expanding its footprint, ending the quarter with 524 global showrooms. A key strategy for the company is its 'Shine with India' campaign, which aims to increase the intake of recycled gold, with this segment contributing over 55% of revenue as of June 2026.

PN Gadgil Jewellers also demonstrated strong momentum, reporting 41% year-on-year revenue growth for the same period. The company's retail segment saw a 56% surge, supported by a 46% same-store sales growth. PN Gadgil is currently focusing on scaling its presence in northern and central India, with plans to add 25 new stores in FY27 to reach a total of 103 locations. Investors should monitor whether these companies can maintain their rapid store addition pace without putting undue pressure on cash flow or operational margins.

Marico and the Impact of Raw Material Costs

Marico’s outlook is partly tied to the softening of key raw material prices. Copra, which is essential for its Parachute coconut oil business, has seen its price drop nearly 45% from recent highs. This decline provides the company with more flexibility to adjust product pricing to drive volume. Marico management has indicated a target of 150-200 basis points for EBITDA margin expansion in FY27.

The company is also looking to scale its foods and digital-first brands while aiming to reach a revenue milestone of ₹15,000 crore in FY27, with a longer-term goal of ₹20,000 crore by FY30. While these targets reflect the company's growth ambition, investors should track whether competitive intensity in the fast-moving consumer goods sector allows for such sustained margin expansion.

Investor Monitorables

The future performance of these stocks will depend on several factors beyond brokerage projections. For the jewellery players, raw gold prices, consumer demand, and the success of new store openings are critical. For Marico, the sustainability of lower copra costs and the ability to grow its newer food portfolios will be key to meeting its stated revenue goals. These companies operate in highly competitive sectors where changing consumer preferences and economic conditions can quickly impact profitability.