What Happened

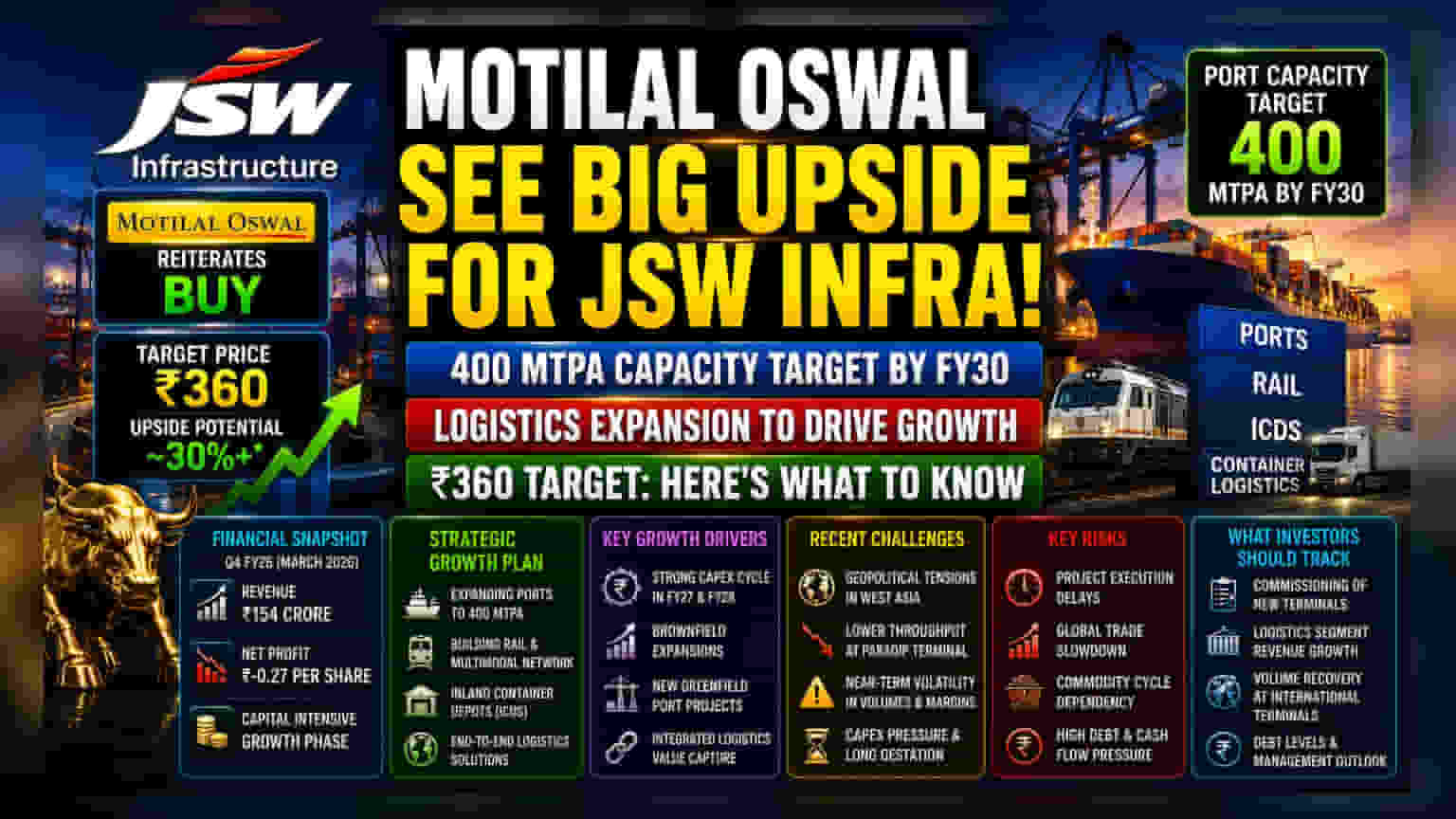

Analysts at Motilal Oswal Financial Services have reiterated a positive stance on JSW Infrastructure, projecting a significant upside based on the company’s long-term growth roadmap. The brokerage anticipates that the company’s ongoing expansion projects, focused on reaching a port capacity of 400 million tonnes per annum (MTPA) by FY30, will serve as a key driver for future performance. The target price for the stock has been set at ₹360, reflecting confidence in the firm's strategic pivot toward integrated logistics and multimodal connectivity.

The Strategic Growth Plan

JSW Infrastructure is currently in the midst of an aggressive capital expenditure cycle. The company’s vision is to evolve from a port operator into a comprehensive logistics player. This involves expanding into rail, inland container depots (ICDs), and container logistics to provide end-to-end service for its clients. By integrating these services, the management aims to reduce reliance on simple port operations and capture more value across the entire supply chain. A central part of this strategy is the significant investment in infrastructure, with substantial capex earmarked for FY27 and FY28 to support both brownfield expansions at existing sites and new greenfield port developments.

Operational Reality and Recent Performance

While the long-term growth thesis remains a focal point for analysts, the immediate operational performance has faced pressure. In the quarter ended March 2026, the company reported a loss of ₹-0.27 per share, with revenue reaching ₹154 crore. This performance highlights the capital-intensive nature of the business and the impact of recent macroeconomic hurdles. Specifically, the company’s operations have been influenced by geopolitical tensions in West Asia and lower throughput at key terminals like Paradip. These issues have created a period of near-term volatility for both cargo volumes and overall profitability.

Market Sentiment and Technical View

Investors are currently balancing the long-term growth story against recent market signals. The stock has faced technical pressure, with some market indicators suggesting a cautious outlook. The combination of high spending on new projects and the time required for these investments to generate steady returns has led to some market hesitancy. Unlike its larger competitor, Adani Ports, which often trades with a different risk-reward profile, JSW Infrastructure is still in a high-growth, high-investment phase, which typically makes it more sensitive to short-term operational misses or project delays.

Risks and Challenges

Investors should be aware of several risks inherent in the current growth phase. High capital expenditure, while necessary for expansion, places pressure on cash flow and requires disciplined execution. Any delay in the commissioning of new projects or a slowdown in global trade can directly impact the company’s ability to meet its revenue and margin targets. Furthermore, the company’s reliance on specific commodities like coal and iron ore makes it vulnerable to cyclical downturns in industrial demand. Geopolitical risks, as seen with terminal disruptions in the Middle East, remain an ongoing factor that can cause sudden, unpredictable impacts on performance.

What Investors Should Track

Moving forward, the key monitorables will be the actual execution of the 400 MTPA capacity target and the profitability of the new logistics segment. Investors may track the commissioning timelines for new terminals and any updates on the logistics division’s revenue contribution. Additionally, management commentary regarding debt levels and the recovery of volumes in international terminals will be crucial to assessing the company’s progress toward its medium-term financial goals.