Blinkit's Quick Commerce Surpasses Food Delivery in User Growth

Eternal Limited, formerly Zomato Limited, reported a strong fiscal fourth quarter for 2026. Net profit surged 346% year-on-year to ₹174 crore, fueled by a 196.5% revenue increase to ₹17,292 crore. A key development was Blinkit's quick commerce (QC) segment surpassing its own Food Delivery (FD) business in Monthly Transacting Users (MTU) for the first time in Q4 FY26.

Blinkit achieved positive adjusted EBITDA of ₹37 crore in Q4 FY26, cementing its position as the quick commerce market leader with an estimated 45-50% share. This gives Blinkit a significant lead over rivals Swiggy Instamart (23-27%) and Zepto (21%). The company plans to expand beyond top cities and increase demand density to maintain its growth.

Profitability Grows Despite Economic Slowdown

Eternal's operational efficiency drove a 575% year-on-year increase in consolidated adjusted EBITDA to ₹486 crore, with margins growing to 2.8%. Blinkit's established markets show potential for 5-6% steady-state margins, while Food Delivery improved its adjusted EBITDA margin to 5.5% of Net Order Value (NOV). This financial improvement occurs as India's broader e-commerce sector faces economic challenges. Post-COVID private consumption growth has slowed to about 8% due to high inflation and stagnant wages, causing e-retail growth to decrease to 10-12% in 2024, down from over 20% previously.

Despite these sector-wide pressures, Eternal's management plans for QC to grow at a 60% annual rate over the medium term. They aim for consolidated adjusted EBITDA to reach $1 billion by FY29E, showing confidence in navigating inflation and meeting consumer demand for speed and convenience.

High Valuation and Fierce Competition

Eternal's market valuation presents a mixed picture. As of late April 2026, its market capitalization was around ₹2.34-2.45 trillion. However, its Price-to-Earnings (P/E) ratio is extremely high, at approximately 1,000 times earnings – far above typical market levels. While some valuation models suggest the stock could be 'Significantly Undervalued', the high P/E ratio remains a concern for investors.

The quick commerce market is very competitive, with rivals like Swiggy Instamart and Zepto fiercely contesting Blinkit's leading position through aggressive pricing and rapid expansion. Average order values in QC are between ₹500-625. Sustained profitability will depend on managing operational costs and achieving sufficient scale.

Analyst Views Mixed on Eternal's Future

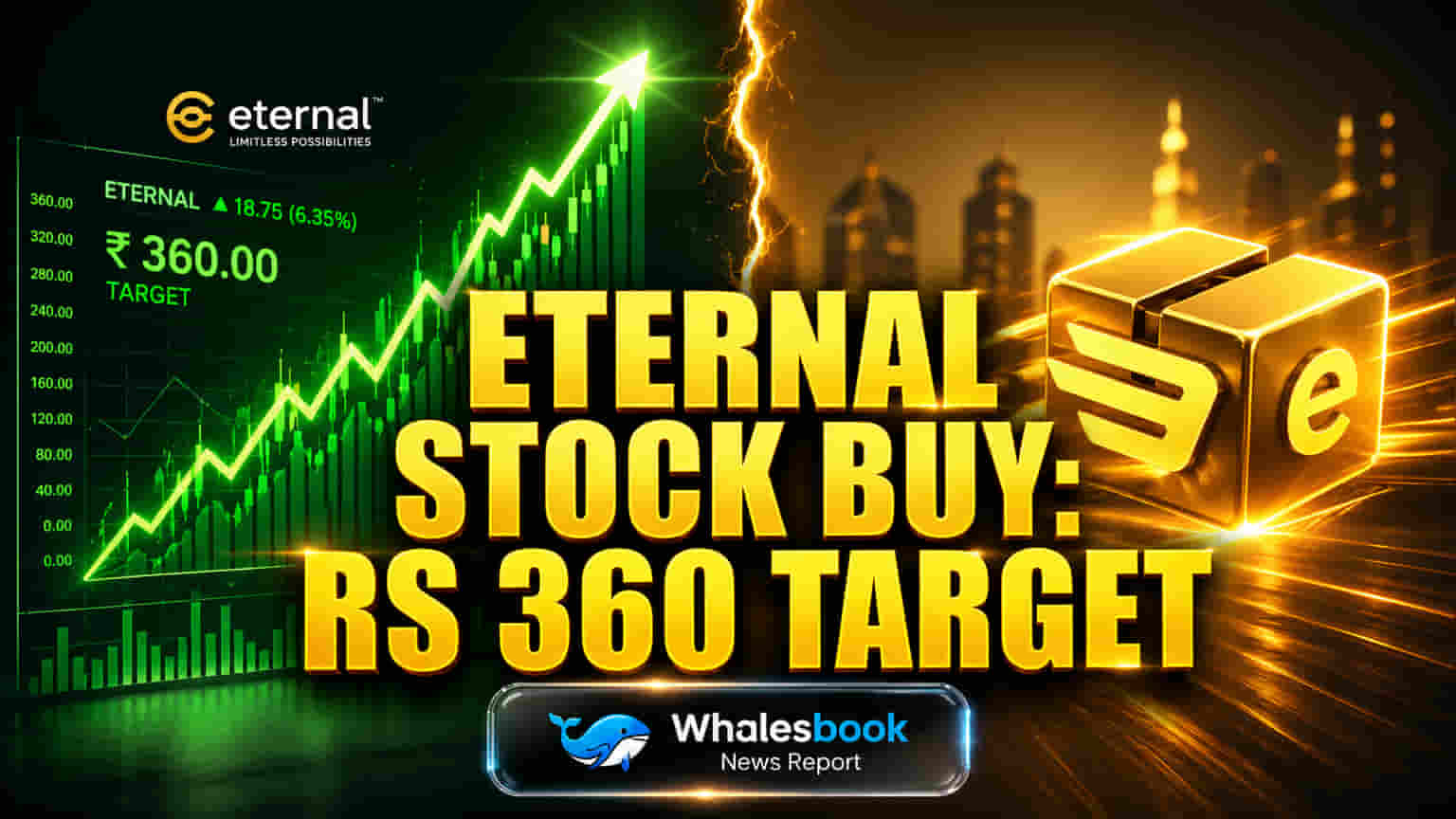

Most analysts remain positive on Eternal, reiterating 'Buy' ratings and projecting 30-40% potential upside with average target prices around ₹359-360. However, some analysts disagree. Macquarie, for example, holds an 'Underperform' rating and a ₹200 target price, citing concerns about slowing growth and intense competition. Bernstein also notes potential near-term volatility. Key risks for the company include quick commerce profitability falling short of expectations and the challenges of rapid scaling in a competitive market.

Long-Term Goals and Growth Strategy

Eternal's strategy centers on expanding its product range, growing its geographical reach, and deepening its presence in tier-2 and tier-3 cities. The company expects to reach $10 billion in annual net order value within two years and aims for $1 billion in adjusted EBITDA by FY29. While AI is viewed as a future tool for operational efficiency, management sees no immediate threat to its core businesses from AI, believing consumer habits are too established. The stock has delivered significant long-term gains but also experienced volatility, including an 11-month low in March 2026. Investors will monitor Eternal's ability to convert user growth into sustained profit at its current valuation while navigating market dynamics and competition.