Brokerage firm Dolat Capital has initiated coverage on R Systems International, highlighting the company’s potential in AI and platform modernization. While the report projects significant growth, it also flags dependencies on the North American market and execution risks related to acquisitions as key factors for investors to watch.

What Happened

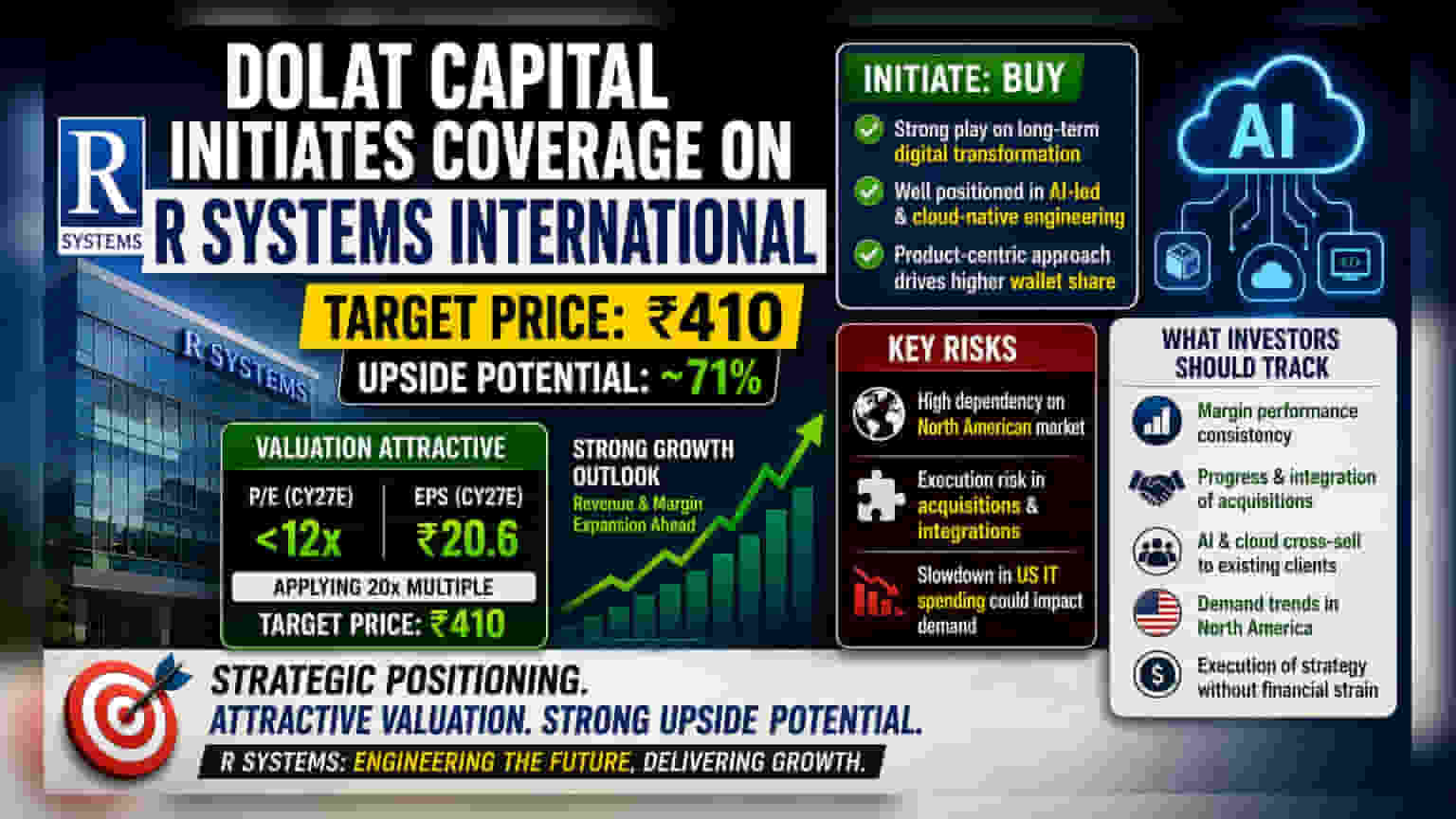

Dolat Capital has officially initiated research coverage on R Systems International Ltd., a provider of product engineering and digital services. In its initial report, the brokerage assigned a positive rating, estimating a target price of Rs 410 per share. The report suggests that the company is well-placed to benefit from long-term digital transformation trends, with the brokerage projecting a potential upside of approximately 71% from current trading levels.

The Growth Thesis

The brokerage points to a few strategic areas where R Systems is expected to perform. First, the report highlights the growing demand for AI-led development among mid-market companies. As businesses move away from basic software maintenance toward AI and cloud-native platforms, specialized engineering firms often see increased demand for their services.

R Systems has focused its business on product-centric engineering, which the brokerage views as a competitive advantage. This approach allows the company to move deeper into client operations, potentially increasing the amount of work it handles for each customer. The report suggests that if the company effectively captures this "wallet share," it could support revenue and margin expansion in the coming years.

Valuation and Earnings Perspective

Dolat Capital’s optimistic view is tied to its valuation assessment. The brokerage noted that recent market corrections have brought the stock to a price-to-earnings (P/E) multiple of less than 12 times its estimated earnings for calendar year 2027.

By forecasting an earnings per share (EPS) of Rs 20.6 for 2027 and applying a multiple of 20 times, the brokerage arrived at its target price. For investors, this perspective suggests that the current stock price may be attractive if the company manages to hit these future earnings targets. However, meeting such targets depends heavily on the company's ability to maintain its profit margins and scale operations without significant cost overruns.

Business Risks to Consider

While the brokerage remains positive, its report also outlines specific risks that investors should take into account. A primary concern is the company's heavy reliance on the North American market. In the IT services sector, this is a common exposure, but it leaves companies vulnerable to any slowdown in US corporate IT spending or changes in macroeconomic conditions.

Additionally, the report mentions execution risks regarding acquisitions. Like many firms in the IT space, R Systems has engaged in inorganic growth (purchasing other companies). Integrating new businesses is inherently risky; it requires merging different work cultures, sales teams, and operational structures. If the integration of these acquired entities is delayed or more expensive than planned, it can put pressure on the company's overall financial health and distract management from core business operations.

What Investors Should Track

Moving forward, the primary monitorables for investors should be the consistency of margin performance and the progress of recent acquisitions. Investors may track whether the company can successfully cross-sell its AI and cloud services to its existing client base. Furthermore, any updates on demand trends in the North American market will be crucial, as this remains the largest revenue driver for the company. The ability of the management to execute its stated strategy without incurring high debt or operational delays will determine if the brokerage’s growth thesis plays out as expected.